Philadelphia Credit Repair Scams: How to Spot Frauds and Find Legit Help in 2026

Your hard-earned savings are on the line. In Philadelphia’s complex credit repair landscape, the fear of losing your limited funds to a slick-talking fraudster is more than just a worry-it’s a paralyzing reality for many. This anxiety over identity theft and broken promises keeps you from achieving the financial freedom and legacy you deserve. But your vulnerability ends today, because knowledge is your ultimate protection.

To secure your future, you must first master the strategies for avoiding common pitfalls, mitigating financial risk, and identifying fraudulent schemes. The most critical piece of this financial education is understanding how to spot legitimate services, particularly those that operate on a post-performance fee model—a clear signal of a trustworthy partner. This guide is your definitive blueprint for 2026. We will equip you to spot every red flag, wield your powerful legal protections under the Credit Repair Organizations Act, and confidently choose a specialist who only gets paid after they deliver proven results.

Prepare to take back control. It’s time to stop feeling exposed and start rebuilding your credit with the absolute certainty that your money and your future are safe.

Key Takeaways

- Master the ultimate legitimacy test for any credit repair service. This is your primary shield against the industry’s Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle.-a legal company will never charge a fee until after the work is done.

- Navigate the complex landscape by learning to spot the red flags of predatory companies. This is the central theme of Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle., which uses the “post-performance fee” model as your shield.

- Discover the specific federal law that protects you-the Credit Repair Organizations Act (CROA). Understanding this law is a key component of navigating Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle., as it gives you the power to cancel any agreement without penalty.

- Arm yourself with a simple checklist to vet any local credit repair company. This tool puts the principles of Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle. into practice, ensuring you find a legitimate Philadelphia-based partner and successfully avoid the very problems outlined in our guide to Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle.

The Landscape of Credit Repair Scams in Philadelphia

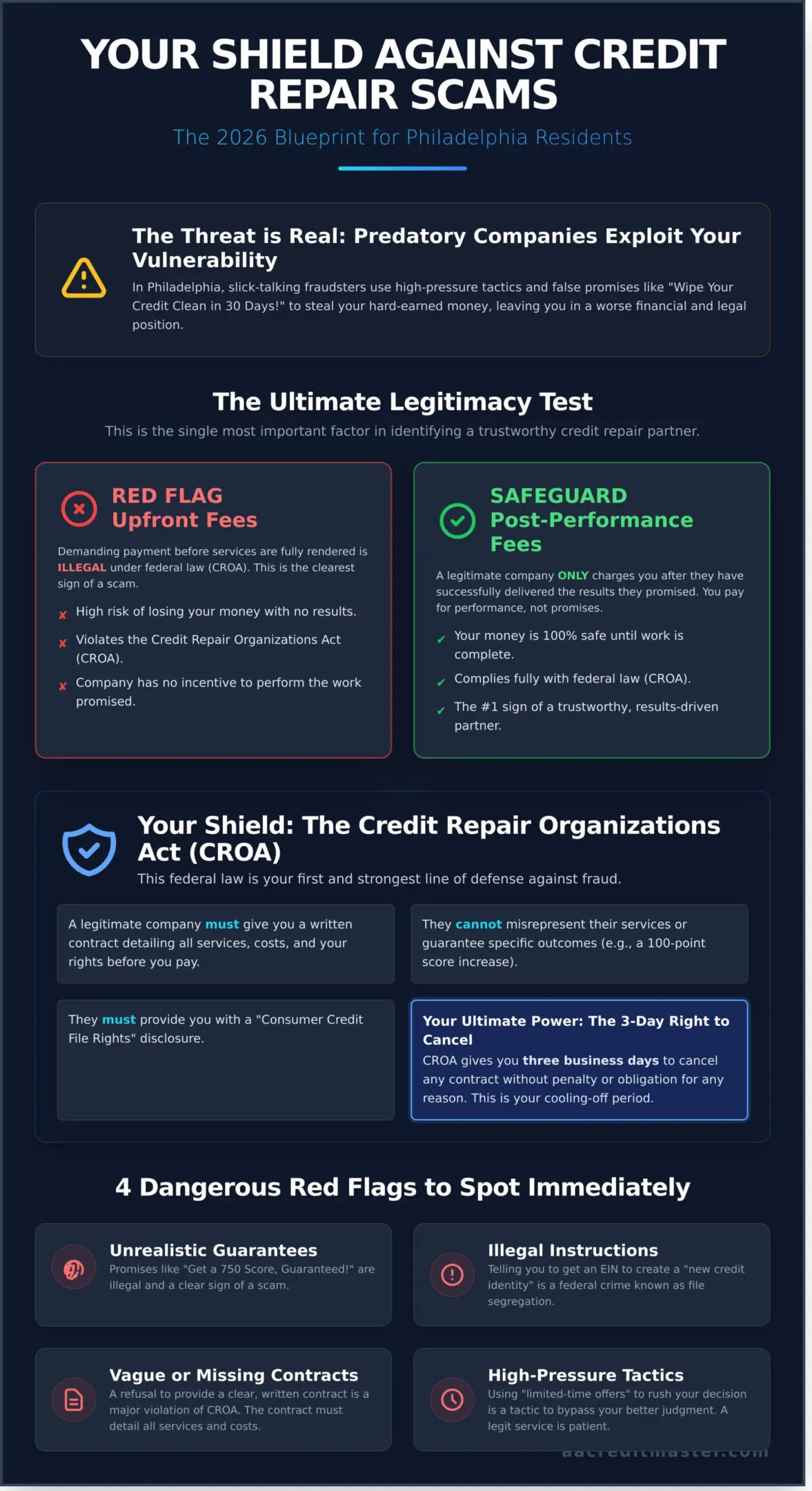

Financial stress is a heavy burden. In neighborhoods across Philadelphia, from Kensington to West Philly, predatory companies exploit this vulnerability with promises that feel like a lifeline. You’ve seen them on billboards and social media feeds: “Wipe Your Credit Clean in 30 Days!” or “Get a 750 Score, Guaranteed!” These claims prey on the desire for a quick fix, but this mindset is the single greatest risk to your financial recovery.

Achieving lasting financial control requires you to first understand the threats. Mastering the world of pain, risk & scams is your first line of defense. It starts by recognizing the difference between legitimate credit education-a process of strategic disputing and rebuilding-and illegal tactics like “file segregation,” which is a federal crime.

The Anatomy of a Credit Repair Scam

Scammers rely on a predictable playbook designed to create panic and bypass your better judgment. They use high-pressure tactics and “limited-time offers” to force an impulsive decision. Their most dangerous red flags include:

- Illegal Demands: They may instruct you to create a “new” credit identity by applying for an Employer Identification Number (EIN) to use instead of your Social Security Number. This is illegal and can lead to serious legal consequences.

- Vague Contracts: A fraudulent company will offer a contract with unclear terms and no specific timeline for services. Federal law, specifically the Credit Repair Organizations Act (CROA), mandates that all credit repair agreements be in writing and detail your rights, the services to be performed, and the total cost.

- Upfront Fees for Removal: A legitimate company will not charge you until after they have performed the services promised. Demanding hundreds of dollars in “setup fees” before any work is done is a major violation and a clear sign of a scam.

The Cost of Falling for a Fraud

The price of a scam is far more than just the money you lose. While the direct financial loss of hundreds or even thousands in bogus fees is devastating, the long-term damage is worse. You not only face potential legal repercussions for participating in illegal schemes but you also delay your journey to true financial literacy by months or even years. Every moment spent with a fraudulent company is a moment you’re not learning to build a powerful financial legacy. Taking back control means focusing on understanding your rights (CROA) and identifying legit services that empower you, not exploit you.

Your Shield: The Credit Repair Organizations Act (CROA) Explained

Feeling powerless against credit reporting agencies is a heavy burden. But you are not alone, and you are not without protection. The Credit Repair Organizations Act (CROA) is the federal law that acts as your shield, defining exactly how credit repair companies must operate to protect you from fraud.

This law is your first line of defense against predatory practices. It grants you specific, non-negotiable rights designed to eliminate the pain, risk, and scams that plague the industry. Before you sign anything, a legitimate firm must provide a “Consumer Credit File Rights Under State and Federal Law” disclosure. They cannot misrepresent their services or guarantee specific outcomes, like a 100-point score increase. Most importantly, CROA makes it illegal for companies to demand payment before they have fully delivered the promised results-a critical detail that exposes upfront-fee scams.

CROA empowers you with fundamental protections:

- The Three-Day Right to Cancel: You have three business days to cancel any contract without penalty or obligation. This is your cooling-off period to reconsider without pressure.

- No False Promises: A company cannot lie about what it can achieve. Vague promises or guarantees to remove legitimate derogatory items are massive red flags. The Consumer Financial Protection Bureau offers a clear guide on how to spot a credit repair scam based on these illegal claims.

- Truthful Disclosures: You must be informed, in writing, of your rights before signing a contract.

Pennsylvania-Specific Protections for Consumers

Here in Philadelphia, your protection is reinforced by state and local agencies. If you encounter a fraudulent credit repair service, you can file a complaint with the Pennsylvania Bureau of Consumer Protection. For more severe cases of financial fraud, the Philadelphia District Attorney’s Office has the power to prosecute criminal organizations, ensuring that those who prey on consumers face serious consequences.

Why a Contract is Non-Negotiable

A verbal promise is worthless. A legitimate credit restoration service will always provide a detailed written contract. This document is your proof of the services agreed upon. Look for a personalized strategy tailored to your specific credit issues, not a generic “boilerplate” template. Your agreement must clearly state all fees, a detailed description of the services, and a written estimate of how long the process will take. This contract is your tool to take back control and ensure accountability.

Upfront Fees vs. Post-Performance: The Ultimate Legitimacy Test

In the complex world of credit restoration, one simple rule cuts through the noise and protects you from fraud. This is the golden rule: You should never pay a credit repair company a single dollar until they have fully performed the services they promised. This isn’t just good advice-it’s the law. Understanding the **pain, risk, and scams** tied to this industry begins with this single, non-negotiable standard.

Your financial security is protected by federal law. The Credit Repair Organizations Act (CROA) explicitly forbids credit repair companies from requesting or receiving payment until the promised results are achieved. Any company that ignores this is not just unethical; they are breaking the law and exposing you to risk.

Scam Model: The Upfront Fee Trap

Scammers demand money before starting work because their business model isn’t built on results-it’s built on volume. They use a “churn and burn” strategy, collecting fees from as many Philadelphians as possible with no intention of delivering real, lasting change. They disguise these illegal fees as “consultation costs,” “document processing fees,” or “first-work fees.” If a consultant asks for your credit card on the first call, that is your signal to end the conversation immediately.

Legitimate Model: Post-Performance Billing

A legitimate company operates on a foundation of confidence and transparency. They trust their ability to achieve results, so they are willing to work first and bill you only after their success. This “pay-after” model aligns their goals directly with yours. They don’t get paid unless you see progress.

So, what does “performance” mean? It means a verified result, such as:

- The successful removal of a negative, inaccurate, or unverifiable item from your credit report.

- Confirmation from the credit bureau that a dispute has been resolved in your favor.

This transparent model ensures you know exactly what you are paying for-actual, tangible improvements to your credit profile. The pricing is customized to the specific derogatory items on your report, not a generic monthly subscription. This is the ultimate proof of a company’s mastery and commitment to helping you take back control.

How to Verify a Philadelphia Credit Service: A 5-Step Checklist

Financial uncertainty is stressful enough without worrying about who to trust. This checklist empowers you to cut through the noise and identify a legitimate partner in Philadelphia. Take back control by asking the right questions from the very first conversation.

Step 1: Demand a Local Address. A legitimate business has roots in the community. Insist on a physical Philadelphia office address, not just a P.O. Box. A local presence means accountability and a team you can meet face-to-face.

Step 2: Check Their BBB Rating. Verify their standing with the Better Business Bureau (BBB). While no system is perfect, a poor rating or a pattern of unresolved consumer complaints is a clear warning sign to stay away.

Step 3: Ask the “CROA Question.” This is critical. Ask, “How do you bill for your services?” To navigate the world of credit repair **pain, risk, and scams**, you must understand your rights. The Credit Repair Organizations Act (CROA) makes it illegal for a company to charge you before they perform the promised services. A compliant company will use a “post-performance fee” model. If they demand money upfront, walk away immediately.

Step 4: Listen for Reassurance, Not Pressure. A true expert offers calm reassurance and a clear strategy. A scammer creates false urgency and uses high-pressure sales tactics. You should feel educated and empowered after a consultation, not cornered or confused.

Step 5: Look for Local Proof. Ask to see testimonials or case studies from other Philadelphia residents. Real results from your neighbors carry far more weight than generic, anonymous reviews found online.

Local Verification Resources

Confirm the company is registered to do business on the Pennsylvania Department of State website. Scan local Philly community forums for unbiased feedback. Also, note their language: a “Credit Score Specialist” focuses on strategic, long-term improvement, while a “Credit Fixer” often implies temporary, unsustainable gimmicks.

Red Flags in the First Consultation

Scammers often reveal themselves early. Watch for these illegal and unethical tactics during your initial call:

- Promises of guaranteed results. No one can legally guarantee a specific score increase or the removal of an accurate derogatory item.

- Telling you not to contact the bureaus. They want to control all communication. You always have the right to speak directly with Equifax, Experian, and TransUnion.

- Failing to explain your rights. A reputable service will always inform you that you can dispute inaccuracies on your own for free. They provide expertise and efficiency, not a secret you can’t access.

Choosing the right guide is the first step toward financial mastery. At AACreditMaster, we believe in transparent, compliant results built on a foundation of trust.

Master Your Credit with AA Credit Master in Philadelphia

You now understand the landscape of credit repair-the red flags, the illegal promises, and your rights. Navigating the world of credit repair means being aware of the pain, risk, and scams that plague the industry. That’s why choosing a local partner who operates with complete transparency isn’t just a preference; it’s a necessity. At Allen & Allen, Inc., we are more than a service; we are Philadelphia’s Financial Guardian, committed to protecting families from predatory practices.

Our foundation is built on the law. We strictly adhere to the Credit Repair Organizations Act (CROA), which is why we operate on a 100% post-performance fee structure. You only pay for the results we achieve. We don’t ask for a dollar until we’ve successfully removed a negative item from your report. This model eliminates your risk and proves our confidence in our ability to help you.

But true financial health goes beyond just removing negative marks. We empower you with the credit education and long-term financial literacy needed to build a lasting legacy. This isn’t about a temporary fix; it’s about giving you permanent control. At our 1515 Market Street office, you’ll work with real people who understand the challenges Philadelphians face.

The Allen & Allen, Inc. Process

Your path to freedom begins with a meticulous, line-by-line audit of your credit reports. We identify every inaccurate, outdated, or unverifiable derogatory item that is legally disputable. From there, we develop a personalized strategy with resources tailored to the Philadelphia economic landscape. We don’t just send letters; we equip you with the knowledge to take back control of your financial future and build a powerful credit profile.

Take the First Step Toward Mastery

In your initial consultation at our Philly office, we’ll review your credit summary and outline a clear, actionable plan. There’s no pressure and no upfront fees-just honest, expert guidance. Waiting only allows creditors to strengthen their position while your score suffers. Don’t let another day pass where your credit history dictates your life’s possibilities. Take action now.

Schedule your professional credit consultation today and begin your journey to financial mastery.

Take Back Control: Your Final Verdict on Philadelphia Credit Repair

Navigating the credit repair landscape in Philadelphia doesn’t have to be a minefield. You now hold the power to distinguish genuine partners from predatory frauds. Your greatest shield is knowledge: understanding your rights under the Credit Repair Organizations Act (CROA) and knowing that legitimate help never demands money upfront. Your ability to identify the Pain, Risk & Scams: Keywords about avoiding scams, understanding rights (CROA), and identifying legit services. Highlight the “post-performance fee” angle. is the first step to reclaiming your financial power.

At AA Credit Master, we earn your trust before we earn your business. We operate on a 100% post-performance billing model, in strict adherence to CROA. From our office in the heart of Philadelphia at 1515 Market Street, our focus is on expert consulting for long-term financial literacy, not just temporary fixes. It’s time to stop worrying and start rebuilding.

Frequently Asked Questions

Is it legal for a credit repair company to charge money before they start working?

No, it is illegal. The Credit Repair Organizations Act (CROA) explicitly forbids companies from requesting or receiving payment until they have fully delivered the promised services. This “post-performance fee” model protects you. If a company demands money upfront for credit repair, consider it a major red flag. A legitimate partner invests in your success first and is compensated only after the work is done, ensuring you avoid credit repair scams.

How can I tell if a credit repair company in Philadelphia is legitimate?

A legitimate company empowers you with knowledge and transparency. They will provide a detailed, written contract before you sign anything, clearly explaining your rights and the services offered. They never guarantee score increases or the removal of accurate items. Look for a physical Philadelphia-area address, positive local reviews, and professionals who focus on a personalized strategy for your financial situation. They should be your guide, not a source of false promises.

What should I do if I have already paid a scammer for credit repair?

Take back control immediately. First, stop all payments and contact your bank or credit card company to dispute the charges. Then, report the fraudulent company to the Federal Trade Commission (FTC), the Consumer Financial Protection Bureau (CFPB), and the Pennsylvania Attorney General’s office. Filing these reports helps protect others and holds these predatory organizations accountable. You have the power to fight back against fraud.

Can a credit repair company guarantee that my score will go up?

Absolutely not. Any company that guarantees a specific FICO score increase or promises to remove all derogatory items is breaking the law. It is impossible to predict the outcome of disputes with credit bureaus like Experian, Equifax, and TransUnion. An honest, professional service will only promise to work diligently and strategically on your behalf, using their expertise to challenge questionable items and advocate for your financial future.

What is the Credit Repair Organizations Act (CROA) and how does it protect me?

The CROA is your shield. It is a federal law created to protect you from deceptive and unfair credit repair practices. It grants you three key rights: the right to a written contract, the right to cancel within three business days, and the right to not be charged until services are complete. Understanding your rights under CROA is the first step in mastering your credit and avoiding the pain, risk, & scams of predatory companies.

How long does legitimate credit restoration usually take in Philadelphia?

Credit restoration is a marathon, not a sprint. While some clients see initial results within 45-60 days, a comprehensive strategy typically takes 3 to 6 months to achieve significant, lasting improvement. The exact timeline depends on the number and type of negative items on your reports. A trustworthy expert will set realistic expectations and provide a clear, step-by-step plan for rebuilding your financial legacy over time.

Are there free resources in Philadelphia for credit education?

Yes, building your financial literacy is a powerful first step. Philadelphia offers excellent non-profit resources. Organizations like Clarifi provide free or low-cost credit counseling and financial workshops to help residents understand their credit reports and create a budget. The Urban League of Philadelphia also offers programs focused on financial empowerment. These resources can provide a strong foundation for your credit journey.

Can I remove accurate but negative information from my credit report?

Legally, accurate and timely negative information cannot be removed. However, “accurate” is a high standard. We often find that derogatory items contain small errors in dates, amounts, or reporting procedures that make them disputable. A professional credit analyst meticulously examines every detail of these items to find legal grounds for a challenge, ensuring the credit bureaus are held 100% accountable for the information they report.