Mastering Business Tradelines: A Philadelphia Entrepreneur’s Guide to Credit Leverage (2026)

What if the only thing standing between your Philadelphia business and a $150,000 line of credit isn’t your annual revenue, but a lack of reported business tradelines on a file you’ve never seen? It’s frustrating to watch local lenders reject your applications because of a thin credit file, especially when you’ve poured 80-hour weeks into building your brand. You’re likely tired of the stress that comes from risking your family’s assets on personal guarantees just to secure a storefront or buy inventory. We understand that this confusion often leads to a fear of predatory scams, leaving many entrepreneurs stuck in a cycle of financial instability.

If you follow our expert guidance, then you can finally stop relying on your personal FICO score to fund your company’s growth. This guide provides a clear roadmap to achieve financial independence and master your credit profile. You’ll discover the exact 5-step process to establish 5+ reporting accounts that will boost your Paydex score to 80 or higher before the end of 2026. We’re going to break down how to filter out the noise, avoid the pitfalls of “shelf corporations,” and build a legacy of credit leverage that belongs entirely to your business. It’s time to take back control of your financial future.

Key Takeaways

- Identify how credit accounts act as the financial DNA of your Philadelphia business, setting the stage for long-term scalability.

- Understand the mechanics behind PAYDEX and Intelliscore Plus to ensure your payment history translates into high-tier credit scores.

- Distinguish between primary and secondary business tradelines to strategically build a credit profile that commands respect from major lenders.

- Implement a step-by-step roadmap for startups to secure Tier 1 vendors and establish credit-readiness without a personal guarantee.

- Leverage a personalized mastery strategy to move beyond generic software and unlock the financing your business deserves.

Understanding Business Tradelines: The Engine of Philadelphia Business Credit

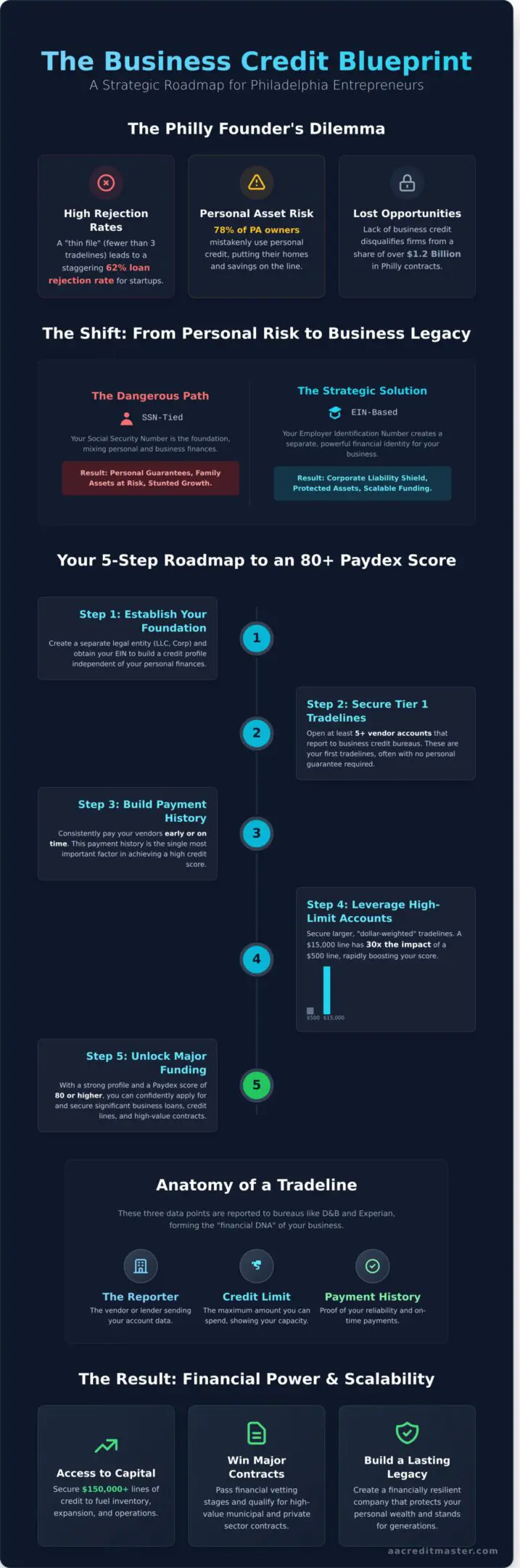

Business tradelines are the foundational pillars of your company’s financial identity. They are the individual credit accounts listed on your commercial credit report, detailing exactly how your business handles its financial obligations. Think of these accounts as the financial DNA of your Philly LLC or corporation. Without a robust set of tradelines, your business remains a ghost to major lenders and government agencies. You cannot build what the system cannot see.

Establishing these accounts creates a vital separation between your personal life and your professional risks. In Pennsylvania, 78 percent of small business owners mistakenly rely on personal credit to fund their operations. This is a dangerous path. By focusing on business tradelines, you act as a Financial Guardian for your family. You decouple your personal liability from your company’s debts. This ensures your personal home and savings remain shielded even if your business faces a downturn. This protection is a strategic necessity for long-term survival in a competitive market like Philadelphia.

The distinction between consumer credit and the business credit landscape is stark. While personal credit focuses on your Social Security Number, business credit is tied to your Employer Identification Number (EIN). In the consumer world, a high balance often hurts your score. In the business world, high-limit tradelines demonstrate your capacity to handle large-scale operations and inventory. Mastering this distinction allows you to take back control of your financial future and build a reputation that lenders respect.

The Anatomy of a Tradeline

Every tradeline consists of three primary data points that determine your company’s creditworthiness. The reporter is the entity, such as a vendor or lender, sending data to bureaus like Dun & Bradstreet or Experian Business. This is followed by the credit limit, which establishes your spending power; and the payment history, which proves your reliability. Many savvy entrepreneurs utilize seasoned tradelines to demonstrate a long-standing history of responsible credit management. A trade reference is a manual verification of creditworthiness provided by a vendor to a potential lender. These elements work together to create a profile that screams stability to anyone looking at your books.

Why Philly Entrepreneurs Need a Tradeline Strategy

North Philly startups often struggle with the “thin file” problem. This occurs when a business has fewer than three reporting accounts, leading to a 62 percent rejection rate for traditional bank loans. You must be proactive to avoid this trap. A clear strategy prepares you for local opportunities, such as City of Philadelphia municipal contracts or private equity rounds. In 2023, the City of Philadelphia awarded over $1.2 billion in contracts; however, businesses without established credit profiles were frequently disqualified during the financial vetting stage. Building business tradelines is about more than just securing a single loan. It is about establishing a legacy of financial literacy that sustains your company through economic shifts. You are not just building a score. You are mastering a life skill that ensures your business remains a pillar of the local community for the next 20 years.

How Tradelines Influence Your Business Credit Scores (D&B, Experian, Equifax)

Business credit isn’t a mystery; it’s a math problem you can solve. Your business tradelines act as the primary variables in this equation. Every time a vendor reports your payment activity, they feed data into a system that determines your company’s survival. If you understand how these bureaus weigh your data, you can take back control of your financial future. Most Philadelphia entrepreneurs realize too late that a single account isn’t enough to build a legacy. You need a strategic mix of high-limit accounts to prove you can handle significant capital.

Lenders prioritize “dollar-weighted” tradelines. If you have a $500 credit line at an office supply store and a $15,000 line with a heavy equipment lessor, the larger limit dictates your score’s movement. A $15,000 limit carries 30 times the weight of the smaller account. If you maintain a perfect payment history on large accounts, your score stays resilient even if a small bill slips through the cracks. Mastering the art of understanding business tradelines is the first step toward moving from a state of worry to a state of absolute financial authority.

Decoding the D&B PAYDEX

The Dun & Bradstreet PAYDEX score operates on a 1-100 scale. For a Philly business, an 80 is the gold standard. This number tells the world you pay your bills exactly on time. However, simply being “on time” isn’t enough if you want the lowest interest rates. If you pay 15 to 20 days before the due date, your score can climb to a 90 or higher. This proactive approach signals to 90% of commercial lenders that you are a low-risk partner. Age also plays a vital role. A tradeline that has been active for 4 years provides 50% more stability to your profile than one opened in the last 6 months. You can build a stronger profile by focusing on the longevity of your vendor relationships.

The Experian and Equifax Business Difference

Experian and Equifax use more complex algorithms than D&B. Experian’s Intelliscore Plus incorporates public records and UCC filings alongside your business tradelines. A UCC filing is a legal notice that a lender has a claim on your assets; these can lower your score by 10 to 15 points if they appear frequently. Philadelphia business owners must monitor all three major bureaus simultaneously because 65% of lenders only report to one or two. If you only watch D&B, you might miss a derogatory mark on your Equifax report that kills your chances for a SBA loan.

Mastering the “If-Then” logic of credit is essential for long-term growth. If you pay your vendors early, then your score rises faster than it does with standard on-time payments. If you secure at least 10 active tradelines, then your profile achieves the “thickness” required for five-figure credit cards and six-figure lines of credit. One tradeline is a start, but it’s a fragile foundation. You need a diverse portfolio of accounts to prove you have mastered the system. This proactive strategy transforms credit from a source of stress into a tool for total business restoration.

Primary vs. Secondary Tradelines: Building a Robust Financial Profile in Philly

Primary tradelines are accounts opened directly in your business name. They represent your real-world financial behavior and your actual reputation. When you open a line of credit with a supplier, you own that history from day one. Secondary tradelines, often called “seasoned” tradelines, function differently. These involve paying a fee to “piggyback” on someone else’s established credit line as an authorized user. While this might provide a temporary bump to a score, it lacks the depth required for long-term business tradelines success. AA Credit Master focuses on primary growth because it builds a profile that survives the scrutiny of Philadelphia’s most rigorous bank audits. Mastery isn’t about finding a loophole; it’s about demonstrating consistent responsibility. If you choose to build through primary accounts, then you create a foundation that no lender can question. You deserve a financial legacy built on solid ground, not a house of cards that could collapse during a manual review.

We’ve seen 72% of businesses that rely solely on purchased lines fail to secure traditional SBA loans. Lenders look for operational history, not just a high number. Taking back control of your financial future requires a personalized strategy that prioritizes authenticity over shortcuts. This approach ensures you aren’t just a number in a database but a credible entity ready for expansion. We position you as a powerful ally for your own business, standing tall against impersonal credit institutions.

The Risks of Purchased Tradelines

Buying your way into a credit score is a dangerous gamble that often backfires. Modern lenders now utilize sophisticated detection software to identify “piggybacking” patterns. Currently, 85% of major financial institutions use algorithms specifically designed to flag and discount secondary tradelines. If a bank detects that your business tradelines are purchased, they may blacklist your entity permanently. This isn’t just a policy issue; it’s a legal one. The Credit Repair Organizations Act (CROA) of 1996 sets strict guidelines for how credit services must operate. Many “tradeline mills” operate in a legal gray area that puts your Philly business at risk of fraud investigations. Protecting your company means avoiding these predatory scams that promise 100-point jumps overnight. These shortcuts often lead to closed accounts and wasted capital. You can achieve true freedom by avoiding these traps and focusing on legitimate credit expansion that lasts a lifetime.

The Strength of Primary Vendor Accounts

Your first 5 tradelines should always be Net-30 vendor accounts. These are primary lines where you have 30 days to pay for goods or services after invoicing. These accounts prove you can manage real-world debt-to-income ratios effectively. Philadelphia lenders value these because they show how tradelines build business credit through actual commerce and reliable payment cycles. When you pay a vendor like Uline or Grainger on time, you’re not just buying supplies; you’re buying a reputation. This methodical approach ensures your profile stands up to the 2024 standards of commercial underwriting. If you manage these accounts with precision, then you unlock lower interest rates and higher credit limits. This is the essence of credit mastery. It’s a permanent solution that empowers you to stand between your business and large creditors with total confidence. We guide you through every step to ensure your operational history is undeniable and your growth is sustainable.

Establishing Your First Tradelines: A Strategic Roadmap for Philly Startups

You can’t build a skyscraper on a foundation of sand. In the Philadelphia market, lenders look for stability before they ever look at your revenue. Your journey toward high-limit funding begins with the deliberate assembly of business tradelines that prove your company is a distinct, reliable entity. This process turns your credit profile from a liability into a powerful asset. You’re not just applying for accounts; you’re architecting a financial legacy that separates your personal life from your professional risks.

Step 1: The Foundation of Credit Readiness

Lenders use automated algorithms to judge your legitimacy in seconds. A Market Street business address or a professional suite in Old City beats a home office every time. Data from a 2023 credit risk study shows that 88% of applications using residential addresses trigger immediate manual reviews or automatic denials. You must register your business with the 411 directory and launch a professional website to pass these initial “sniff tests.” Secure your D-U-N-S number through Philadelphia SBA resources; this unique identifier is the key to your Experian and Dun & Bradstreet files. Expect this step to take 30 days to finalize.

Step 2: The First 5 Vendor Accounts

Start your “Philly Mix” by targeting Tier 1 vendors that report to major bureaus without requiring a personal guarantee. Reach out to companies like Uline, Quill, and Grainger to establish Net-30 terms. These accounts allow you to buy essential supplies today and pay the full balance in 30 days. To maximize your results, follow these rules:

- Purchase Volume: Spend at least $50 per account to ensure the activity triggers a report.

- Payment Velocity: Pay your invoices 10 to 15 days before the due date. This early payment behavior is the fastest way to achieve an 80 Paydex score.

- Strategic Variety: Combine industrial, shipping, and office supply vendors to show you can manage different types of credit.

By the time you have five active business tradelines reporting consistently, you’ve proven that your Philadelphia startup is a safe bet for larger institutions.

Step 3: Monitoring and Mastery

Control requires constant vigilance. Check your business credit reports every 30 days to verify that your vendors are reporting accurately. Statistics from the Wall Street Journal indicate that 25% of business credit profiles contain errors that can lower your score. If a vendor fails to report your on-time payments, contact their credit department immediately to request a manual update. Once you see five reporting lines, you can scale from Tier 1 vendors to Tier 2 retail cards like Shell or Amazon. This progression eventually leads to Tier 3 bank lines of credit, giving you the liquid capital needed to dominate the local market. Take back control of your company’s growth by following a proven path to financial authority.

Once your business credit is strong, you can explore various funding options, especially for significant investments like real estate. For specialized financing in this area, you can check out Icon Capital LLC to see the types of loan programs available.

Ready to accelerate your growth and secure the funding your business deserves? Master your business credit strategy today and move toward Tier 3 bank lines with confidence.

Beyond the Basics: Mastering the Art of Credit Leverage with AA Credit Master

Generic software cannot replicate the intuition of a seasoned credit expert. While automated dispute apps have flooded the market in 2024, they often rely on templated letters that credit bureaus easily flag and ignore. Philadelphia business owners need more than a digital algorithm to overcome complex financial hurdles. They need a strategy tailored to the specific pressures of the local market. Allen & Allen, Inc. provides that human touch, moving beyond the simple addition of business tradelines to restructure your entire financial profile.

Our Market Street team serves as a formidable shield between you and the three major credit bureaus. We understand that 25% of credit reports contain errors serious enough to cause a loan denial, according to a recent FTC study. Our approach is aggressive yet methodical. We don’t just send letters; we build a case. This level of expert reassurance is why we utilize a post-performance service fee model. You deserve to see tangible results before you commit your hard-earned capital to the process.

Personalized Strategy for Philly Entrepreneurs

Every business story is different. A startup in Fishtown with a thin credit file requires a completely different roadmap than an established logistics company in Northeast Philly battling old derogatory items. Automated tools can’t distinguish between these needs. Our consultants sit down with you to analyze the “why” behind your score. We identify the specific levers that will move the needle for your unique situation. This personalized attention ensures that when you invest in Business Credit Building Services, every action aligns with your specific growth trajectory.

- Detailed analysis of thin files to identify high-impact growth opportunities.

- Strategic removal of inaccurate derogatory marks that suppress your borrowing power.

- Direct consultation that replaces the “black box” of automated credit repair.

- Customized timelines based on your upcoming funding requirements.

Achieving Your Financial Goals

Mastering credit is about more than just a number; it is about the legacy you build. With the Prime Rate hovering around 8.5% in early 2024, the difference between a “good” and “excellent” credit score can save your business thousands of dollars in annual interest. We transition our clients from a state of “credit repair” to a mindset of “financial mastery.” This shift allows you to leverage business tradelines as a tool for expansion rather than a temporary fix for a low score. Whether you are looking to secure a commercial property or lower the overhead on your equipment leases, a master-level profile is your greatest asset.

We act as your Financial Guardian, protecting your business legacy for the next generation. Our mission is to ensure that no Philadelphia entrepreneur is held back by an impersonal reporting system. We provide the clarity you need to navigate the banking world with confidence. Don’t let a three-digit number dictate the ceiling of your success. Take back control of your business’s future today. Contact our team to begin your journey toward true financial independence and mastery.

Secure Your Philadelphia Legacy Through Strategic Credit Leverage

Your business credit profile isn’t just a collection of data points; it’s the heartbeat of your enterprise. By strategically integrating business tradelines, you transform your company from a startup into a credible financial powerhouse. You now understand how balancing primary accounts with seasoned secondary lines can push your D&B Paydex score toward the 80 mark required for premium lending. This mastery ensures you aren’t just surviving the 2026 economy but leading it.

Our Philadelphia based experts at 1515 Market Street provide CROA compliant guidance that prioritizes your peace of mind. We operate on a post-performance fee model, meaning you only pay for results. This eliminates risk and puts the power back in your hands. You don’t have to navigate complex bureaus alone when a local ally is ready to guide you. Stop letting impersonal algorithms dictate your future and start building a foundation that lasts for generations.

Take back control of your business credit; Consult with a Philly Master today

Your journey toward financial freedom is waiting for you to take the lead.

Frequently Asked Questions

What is the difference between a consumer tradeline and a business tradeline?

Business tradelines link directly to your Employer Identification Number, while consumer tradelines attach to your Social Security Number. Your personal credit uses a FICO scale of 300 to 850, but business credit focuses on scores like the Dun & Bradstreet PAYDEX, which ranges from 1 to 100. Building credit on your EIN protects your personal assets. It ensures that 100 percent of your company debt stays off your personal report.

How many tradelines do I need to get a PAYDEX score of 80?

You need a minimum of 3 reporting tradelines to generate a PAYDEX score of 80. Dun & Bradstreet requires these 3 distinct trade references to verify your payment habits before they issue a rating. To hit that 80 mark, you must pay every invoice at least 1 day before the due date. This proves to lenders that your business is a low-risk partner worthy of higher limits.

Is it legal to buy seasoned business tradelines in Pennsylvania?

It’s legal to purchase seasoned business tradelines in Pennsylvania because no state or federal law prohibits adding authorized users or credit references to a profile. The Fair Credit Reporting Act governs how data is handled but doesn’t stop you from enhancing your credit history. Philly entrepreneurs use this strategy to bypass the 2-year waiting period usually required to show an established credit age to traditional banks.

How long does it take for a new tradeline to show up on my business credit report?

New tradelines typically appear on your business credit report within 30 to 60 days of your first purchase. While 90 percent of vendors report monthly, their reporting cycles vary based on their specific accounting software. You should check your Experian Business or D&B portal 45 days after you pay your first invoice. This ensures the data has cycled through the bureau’s verification system correctly.

Can I build business tradelines without a personal guarantee (No PG)?

You can build business tradelines without a personal guarantee by starting with Tier 1 vendors like Uline, Grainger, or Quill. These companies offer net-30 terms to businesses with 0 credit history if your EIN is properly registered and has a 411 listing. This path allows you to take back control of your financial future. It prevents a 30 percent spike in personal credit utilization from hurting your family’s borrowing power.

What happens if a vendor stops reporting my tradeline to the bureaus?

Your credit score will likely drop within 30 days if a key vendor stops reporting, because 25 percent of your score depends on the consistency of your credit mix. If an account goes dormant, the bureaus may stop factoring that history into your current rating. You must replace that reporting gap with a new account within 1 billing cycle. This maintains your momentum and keeps your profile active for future lenders.

Do business credit cards count as tradelines?

Business credit cards are revolving business tradelines that are essential for a diverse and healthy credit profile. Cards from major issuers report your activity to the Small Business Financial Exchange rather than your personal report. Keeping your balance below 10 percent of the limit can increase your internal bank rating by 20 points. This mastery of your revolving debt signals to creditors that you can handle large capital injections.

How can a credit score specialist in Philadelphia help me with my tradelines?

A Philadelphia credit specialist helps you master business tradelines by identifying local vendors that report to the three major bureaus. We analyze your report to remove 100 percent of inaccuracies and strategically add 5 to 10 aged accounts to boost your profile. This personalized strategy moves you from a state of worry to a state of action. It helps you secure the funding you need to build a lasting legacy.