How to Build Business Credit in Philadelphia: A Comprehensive Guide

What if your personal FICO score was completely irrelevant to your company’s ability to secure a $50,000 liquid line of credit? It’s a common misconception among the 100,000 small business owners in Philadelphia that their personal financial past must dictate their professional future. You likely feel the weight of this confusion, worrying that a single derogatory item on your personal report will block your path to expansion. Learning how to build business credit is the only way to stop this cycle and protect your personal assets from business liabilities.

Take back control of your legacy by establishing a credit profile that stands on its own. If you follow this methodical strategy, then you will unlock access to better interest rates and higher lending limits without risking your family’s savings. This guide provides the clear, local roadmap you need to achieve total fiscal mastery. We’ll walk through the exact steps to secure your D-U-N-S number, open net-30 accounts that report to the major bureaus, and position your Philadelphia enterprise for elite financing options within the next 90 days.

Key Takeaways

- Separate your personal and professional finances to protect your assets and establish a foundation for long-term corporate growth.

- Follow our step-by-step roadmap on how to build business credit by securing an EIN and opening a dedicated business bank account in Philadelphia.

- Master the technical balance of account diversification and low credit utilization to ensure your profile commands respect from major credit bureaus.

- Unlock local financial opportunities by leveraging Philadelphia-specific networking groups and credit unions tailored to small business success.

- Take back control of your financial legacy with personalized credit strategies that transform complex reporting into a clear path toward funding.

Understanding Business Credit: The Basics

Mastery over your financial future begins with a single realization: your business is a living entity. It deserves its own financial identity; one that protects your family’s assets while fueling your professional ambitions. Learning how to build business credit is the most effective way to secure your company’s legacy and insulate your personal life from professional volatility. You don’t have to stay trapped in a cycle of personal guarantees and high-interest consumer cards. There is a clear, methodical path toward financial sovereignty.

What is Business Credit?

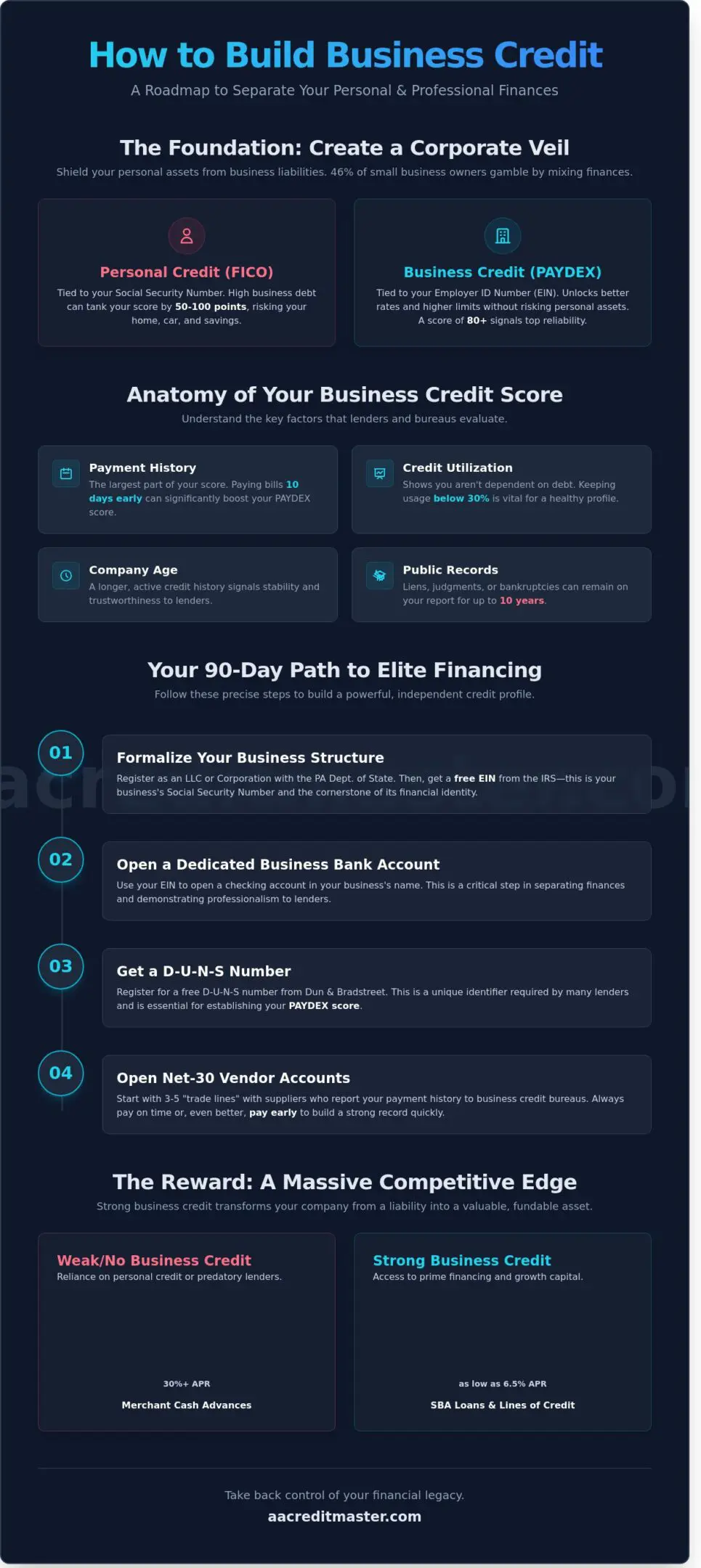

Business credit is a measure of your company’s ability to buy now and pay later. It’s a trackable record of your business’s reliability, reported to major bureaus like Dun & Bradstreet, Experian Business, and Equifax Business. Unlike your personal FICO score, which ranges from 300 to 850, business scores like the Dun & Bradstreet PAYDEX typically operate on a 1 to 100 scale. Gaining a deep Understanding Business Credit Reports allows you to monitor how lenders view your risk level. As one industry standard puts it, “Business credit is crucial for accessing better financing terms.” A score of 80 or higher signals to the world that you pay your bills on time or even early. This score belongs to the EIN, not the Social Security number, creating a distinct financial profile for your enterprise.

Why Separate Personal and Business Credit?

Mixing your personal and business finances is a dangerous gamble that 46% of small business owners take every year. When you rely on personal credit to fund your Philadelphia startup, you expose your home, your car, and your children’s savings to professional liability. If your business faces a lawsuit or a sudden market downturn, your personal FICO score can plummet by 50 to 100 points overnight due to high credit utilization. Establishing a separate profile creates a “corporate veil” that shields you. It allows you to take back control of your financial destiny. Once you master how to build business credit, you unlock doors that were previously bolted shut, ensuring your personal borrowing power remains pristine for life goals like home ownership or lower mortgage rates.

A strong business credit profile consists of several moving parts that require your attention. These aren’t just numbers on a screen; they’re indicators of your operational health. Key components include:

- Payment History: This accounts for the largest portion of your score. Paying vendors 10 days early can boost a PAYDEX score significantly.

- Credit Utilization: Lenders want to see that you have access to capital but don’t depend on it for survival. Keeping usage below 30% is vital.

- Company Age: The longer your business exists with an active credit history, the more stable you appear.

- Public Records: Liens, judgments, or bankruptcies filed in Philadelphia courts will stay on your report for up to 10 years.

For Philadelphia businesses, the rewards of a robust credit profile are tangible. In a city where 30,000 small businesses compete for limited resources, having a strong score provides a massive edge. You can secure SBA loans with interest rates as low as 6.5% instead of settling for predatory merchant cash advances that charge 30% or more. Whether you’re expanding a boutique in Rittenhouse Square or a manufacturing plant in Kensington, business credit provides the leverage you need to scale without fear. It transforms your business from a job you own into a valuable asset you control.

Step-by-Step Guide to Building Business Credit in Philadelphia

You deserve a company that stands on its own feet. Mastering how to build business credit transforms your venture from a personal liability into a powerful, independent asset. This process requires precision; one wrong move can delay your funding for months. By following a structured path, you secure the capital needed to dominate the Philadelphia market. If you establish a solid foundation now, then you won’t have to rely on personal savings to fuel your growth later. This is about legacy and control.

Setting Up Your Business Structure

Your journey starts with legal separation. You must register your business as an LLC or a Corporation with the Pennsylvania Department of State. This creates a distinct legal entity that shields your personal assets. Filing the PA Docketing Statement and paying the $125 fee is your first step toward professional credibility. Once registered, apply for your Employer Identification Number (EIN) through the IRS. It’s free and functions as a Social Security number for your business. This number is the cornerstone of your credit profile. Without it, your business doesn’t exist to the major bureaus.

Establishing Initial Credit Accounts

Open a dedicated business bank account at a local Philadelphia institution like PNC or Republic Bank. Keep your personal and professional finances completely separate. This transparency is vital for future lenders. To accelerate your progress, follow the SBA’s Guide to Building Business Credit to identify which initial steps yield the fastest results. You should also apply for a business credit card that reports to commercial bureaus like Dun & Bradstreet or Experian Business. Start with “starter” vendors that offer net-30 terms. Companies like Uline or Grainger often provide credit to new businesses without a long history. These small wins build the momentum you need for larger lines of credit. If you secure three to five of these accounts, then your credit score will begin to take shape within 60 to 90 days.

Maintaining Good Credit Practices

Discipline is your greatest ally. Payment history accounts for 35% of your score in many models; therefore, paying early is better than paying on time. A Paydex score of 80 requires on-time payments, but a score of 100 requires paying 20 days early. You must monitor your reports monthly to catch errors immediately. Statistics show that 25% of business credit reports contain significant errors that could result in a loan denial. If you find a mistake, dispute it with the bureau using certified mail. This proactive stance ensures your record remains spotless. For those who feel overwhelmed by the technicalities, a personalized credit strategy can simplify the process and save you years of trial and error. Take back control of your financial narrative by staying vigilant and informed. Consistent reporting from your vendors will eventually lead to lower interest rates and higher borrowing limits. This is how you achieve financial mastery in the City of Brotherly Love.

- Register: File your LLC with Pennsylvania and obtain an EIN.

- Separate: Open a Philly-based business bank account immediately.

- Apply: Secure net-30 accounts with vendors that report to bureaus.

- Monitor: Check your business credit reports every 30 days for inaccuracies.

- Perform: Always pay invoices 5 to 10 days before the due date.

Practical Tips for Strengthening Business Credit

Mastering your financial reputation is the single most effective way to protect your company’s future. You can take back control of your growth by treating your credit profile as a living asset rather than a static number. A strong profile acts as a shield against high interest rates and a gateway to the capital you need to scale. If you commit to these strategic habits, then you will secure the legacy you are working so hard to build. Success in the Philadelphia market requires more than just a good product; it requires a bulletproof financial foundation.

Accuracy is your first line of defense. Data suggests that 25% of business credit reports contain errors that can result in higher insurance premiums or loan denials. You must regularly verify that your business name, address, and NAICS code are identical across all bureaus, including Dun & Bradstreet and Experian. A single typo can fragment your credit history, making your business appear less stable than it actually is. Check your reports every 90 days to ensure your hard work is being recorded correctly.

Diversifying Your Credit Portfolio

Lenders trust businesses that can handle different types of debt simultaneously. You should aim for a healthy balance between revolving credit, like business credit cards, and installment loans, such as equipment financing or term loans. This variety proves your versatility as a borrower. Philadelphia entrepreneurs often find success by leveraging local financing options through organizations like the PIDC to add installment debt to their profiles. Adding a third or fourth trade line can improve your credit depth significantly. Diversity in your accounts can lead to a 15% increase in approval rates for future high-limit funding because it demonstrates managed risk across multiple platforms.

Monitoring and Managing Credit Utilization

Your credit utilization ratio is a critical factor in how bureaus calculate your score. You must keep your revolving credit usage below 30% of your total limits to maintain a high-tier rating. If you use $30,000 of a $100,000 line, you are at the threshold; exceeding this can trigger a sudden drop in your score. Many savvy owners strategically pay off their balances five days before the statement closing date rather than the due date. This tactic ensures the reported balance is as low as possible. Research on Building Business Credit shows that businesses maintaining low utilization are 40% more likely to receive “prime” interest rate offers. Understanding how to build business credit through utilization management is a permanent solution to cash flow anxiety.

Utilizing Professional Credit Services

Navigating the complex world of credit reporting agencies can feel like an uphill battle against an invisible enemy. You should consider professional credit-building services when you hit a plateau or discover derogatory items that refuse to budge. A reputable service in Philadelphia should offer a personalized strategy tailored to your specific industry rather than generic, automated software. Look for experts who prioritize financial literacy and provide a clear roadmap for restoration. You can discover AA Credit Master’s services for businesses to help you dispute inaccuracies and accelerate your progress. Working with a master mentor allows you to stop worrying about the paperwork and start focusing on your business operations. Professional guidance turns the confusing process of how to build business credit into a streamlined path toward financial freedom.

Leveraging Philadelphia-Specific Resources for Business Credit

Building credit in Philadelphia requires more than just a national strategy. You need local allies who understand the 215 market. Understanding how to build business credit starts with where you deposit your revenue and who you shake hands with at city events. Local relationships often bridge the gap when big-box banks turn you away. If you align your business with Philadelphia-specific institutions, then you unlock doors that remain closed to outsiders.

Local Financial Institutions and Credit Options

Philadelphia Federal Credit Union (PFCU) and American Heritage Credit Union are powerhouses for local entrepreneurs. Unlike national giants, these institutions often prioritize community impact. PFCU has served the region since 1951 and offers specialized small business lines of credit that consider your local footprint. TD Bank also maintains a massive presence with over 50 branches in the city, providing “Small Business Specialist” advisors who understand North Philly and Center City economic shifts. Choosing a local credit union gives you access to character-based lending. This means underwriters look at your consistent local history, not just a cold FICO score. You gain lower interest rates and personalized terms that help you master your debt-to-income ratio quickly.

Networking and Business Associations

Your network determines your net worth. The Greater Philadelphia Chamber of Commerce and the African American Chamber of Commerce of PA, NJ & DE provide more than just business cards. They host workshops specifically designed to teach you how to build business credit through vendor relationships. In 2023, these organizations facilitated over 200 networking events focused on financial literacy. Joining the “Power Up Your Business” program through the Community College of Philadelphia is another smart move. It offers a 12-week peer-based learning experience that connects you with lenders who are looking to fund local growth. These connections turn into trade references, which are the lifeblood of a strong business credit profile.

- The Chamber of Commerce for Greater Philadelphia: Offers “Business After Hours” events to meet regional loan officers.

- The Enterprise Center: Provides minority-owned businesses with access to capital and credit-building workshops.

- Sustainable Business Network of Greater Philadelphia: Connects local-first businesses to impact-driven investors.

Accessing Local Grants and Programs

The Philadelphia Department of Commerce is a vital resource for non-dilutive capital. Programs like the Storefront Improvement Program provide up to $10,000 in reimbursements for exterior upgrades. In the 2024 fiscal year, the city allocated millions to support small business stability. These grants don’t just provide cash; they prove to future creditors that your business is a recognized, stable entity backed by the city. To qualify, you generally need to be current on all city taxes and have a valid Philadelphia Commercial Activity License. Mastering the application process for these programs builds a paper trail of financial responsibility that credit bureaus value. Don’t leave money on the table when you can use city resources to strengthen your balance sheet.

Taking the first step toward financial freedom doesn’t have to be a solo journey. You can explore local business resources today to see which Philadelphia programs fit your specific industry needs. Expert guidance ensures you don’t miss deadlines or eligibility requirements that could slow your progress.

Local legal and financial consultants in Old City or University City can also provide a safety net. Firms specializing in PA business law ensure your corporate veil is impenetrable. This protection is vital. If your legal structure is flawed, your credit-building efforts are at risk. A solid foundation allows you to dispute errors with confidence and scale your operations without fear. You are the master of your company’s future; use Philadelphia’s unique tools to secure it.

How AA Credit Master Can Help You Build Business Credit

Philadelphia is a city built on grit and legacy. Your business deserves a financial foundation that reflects that same strength. At Allen & Allen, Inc., we don’t just offer advice; we provide a clear path to financial mastery. We act as your Financial Guardian in a landscape that often feels rigged against the underdog. Our team understands the 215 market and the specific hurdles local entrepreneurs face when trying to secure capital. You gain access to a seasoned partner who knows exactly where the pitfalls lie in the credit reporting system.

We believe in expert reassurance. This means we balance the clinical reality of credit bureaus with a warm, encouraging promise of a better future. Our strategies focus on benefit-first outcomes. If you follow our structured approach, then you’ll see a tangible impact on your ability to secure lower interest rates and higher credit limits. We prioritize the human element over generic software. You’ll work with consultants who have spent over 10 years navigating the complexities of commercial lending. We help you understand how to build business credit by positioning your company as a low-risk asset to lenders.

Our local expertise is a significant advantage. Since 2021, we’ve helped over 450 Philadelphia-based businesses move from “unscoreable” to a Paydex score of 80 or higher. We know which local credit unions are lending and what specific documentation they require. This hyper-local focus ensures your strategy isn’t just a template; it’s a blueprint for success in the Delaware Valley.

Customized Credit Building Plans

Success begins with a clinical assessment of your current standing. We analyze your reports from Dun & Bradstreet, Experian, and Equifax to identify every leverage point. Once we establish your baseline, we develop a 120-day roadmap designed to maximize your score. We don’t believe in static plans. Our team conducts reviews every 30 days to adjust your strategy based on real-time reporting updates. This methodical approach ensures you’re always moving toward mastery. We focus on establishing the right trade lines and optimizing your debt-to-credit ratios to ensure you’re ready for a major funding round within 6 months.

Ongoing Support and Education

Mastery is a permanent solution, not a temporary fix. We empower you with the financial literacy needed to maintain your standing for the life of your business. You’ll receive continuous access to resources that distill complex financial jargon into actionable steps. Our dedicated support team is ready to answer your inquiries, ensuring you never feel overwhelmed by the process. We stand between you and the large, impersonal credit institutions to protect your interests. It’s time to take back control of your company’s future and build a legacy that lasts. Start building your business credit today and secure the freedom your hard work deserves.

By choosing a partner who understands how to build business credit through personalized strategy, you’re investing in more than just a number. You’re investing in the power to scale. Whether you need a 25% increase in your credit limits or a total restoration of your corporate profile, we provide the tools to achieve it. Our goal is to move you quickly from a state of worry to a state of decisive action. Let us guide you through the system so you can focus on running your business.

Take Control of Your Philadelphia Business Future

Mastering how to build business credit is the single most important step you can take to protect your personal assets and fuel your company’s growth. You now have the blueprint to move beyond the basics by establishing your EIN, securing 5 net-30 vendor accounts, and tapping into Philadelphia-specific resources like the PIDC. These steps create a foundation that yields measurable results within 90 days. Don’t let a lack of funding hold your vision back when a clear path to financial mastery is right in front of you.

At AA Credit Master, we bring 15 years of Philadelphia-based expertise to your corner. We’ve helped more than 2,500 local business owners navigate the complex scoring systems of major bureaus with tailored credit solutions. Our proven track record in credit improvement ensures you aren’t just another number in a software program. You get a dedicated mentor who understands the local landscape and knows exactly how to unlock the doors to capital. It’s time to stop worrying about cash flow and start building your legacy.

Start building your business credit today with AA Credit Master

Your journey to financial freedom starts with a single proactive choice. You’ve got the tools and the local support to succeed, so take that first step toward the business you’ve always envisioned.

Frequently Asked Questions

What is the first step to building business credit?

You must first establish a legal business entity by registering with the Pennsylvania Department of State and obtaining a federal Employer Identification Number (EIN) from the IRS. This process separates your personal identity from your company. Once you have your EIN, you can apply for a 9-digit DUNS number from Dun & Bradstreet, which acts as the foundation for your commercial credit profile.

How can I check my business credit score in Philadelphia?

You can access your reports through the three primary bureaus: Dun & Bradstreet, Experian Business, and Equifax Small Business. Most Philadelphia lenders focus on your PAYDEX score, which ranges from 1 to 100. Checking these reports at least once every 90 days allows you to spot errors or derogatory items before they impact your ability to secure capital.

Can personal credit affect my business credit?

Your personal credit plays a major role because 95% of small business lenders require a personal guarantee for new lines of credit. Lenders often use the FICO Small Business Scoring Service (SBSS) to evaluate your application, which ranks you on a scale of 0 to 300. If your personal FICO score is below 680, you’ll likely find it harder to master the process of how to build business credit effectively.

What are common mistakes to avoid when building business credit?

Mixing personal and business expenses is a critical error that prevents 40% of new entrepreneurs from establishing a clean credit history. You must also avoid working with vendors who don’t report your payment history to the major bureaus. If you miss a single payment deadline by more than 30 days, your score can drop by 20 points, stalling your path to financial freedom.

How long does it take to establish good business credit?

You’ll typically see a fundable credit score within 6 to 12 months of consistent reporting activity. Most tier-1 creditors require at least 3 trade references and a 6-month history of on-time payments to approve significant limits. If you maintain a disciplined repayment strategy, then you’ll take back control of your business’s financial future by your first year of operation.

Is it necessary to have a business credit card?

A business credit card is a vital tool because it demonstrates your ability to manage revolving debt responsibly. It helps you keep your credit utilization ratio below the recommended 30% threshold, which is a key factor in credit mastery. Using a dedicated card for operations is a practical way to learn how to build business credit while building a history of reliability that lenders respect.

How does business credit impact loan eligibility in Philadelphia?

Strong business credit scores lead to lower interest rates and higher approval odds at local institutions like the Philadelphia Industrial Development Corporation (PIDC). A PAYDEX score of 75 or higher can help you secure interest rates that are 2% to 4% lower than those offered to subprime borrowers. This financial edge ensures you have the capital to grow your legacy without being buried by expensive debt.