How to Fix Credit After Divorce in Philadelphia: A Step-by-Step Guide to Financial Independence

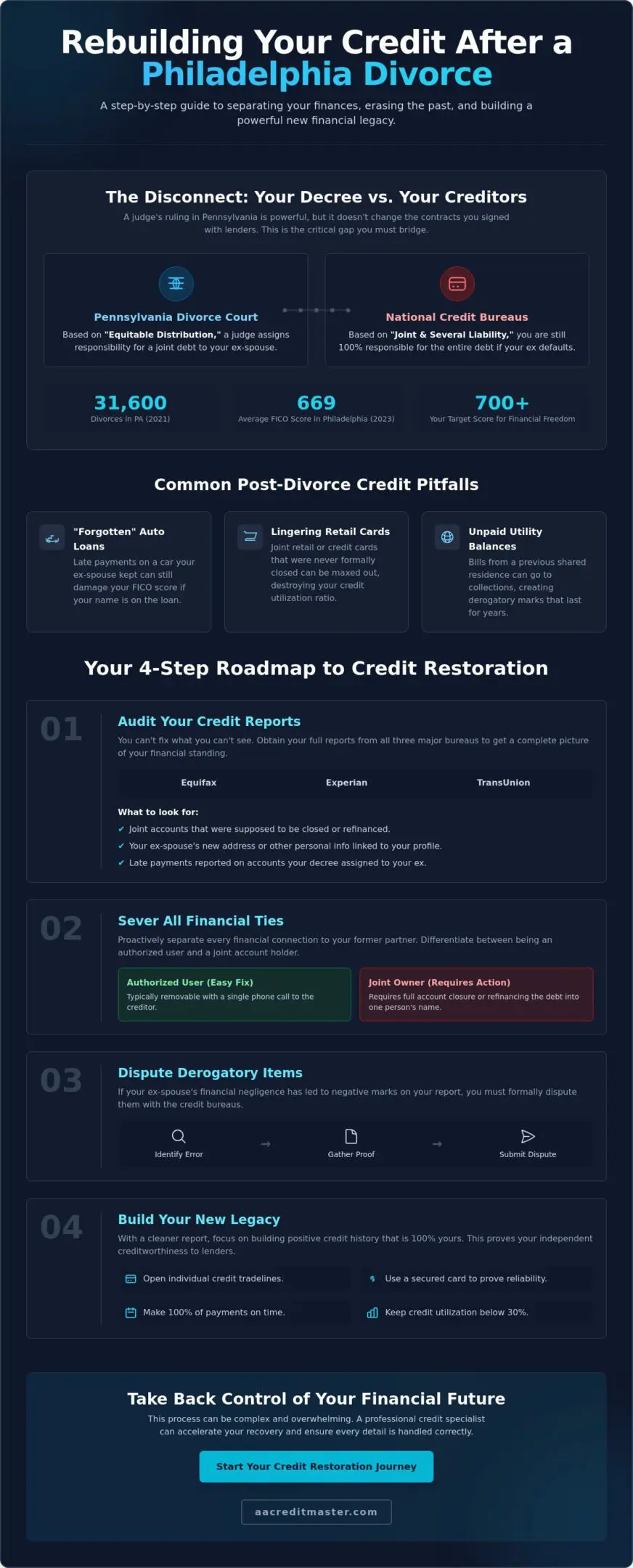

Your Philadelphia divorce decree might state that your ex-spouse is responsible for the joint credit card debt; however, to a credit bureau, that document is essentially invisible. It’s a harsh reality that Pennsylvania’s equitable distribution laws don’t bind national creditors or protect your FICO score from an ex-partner’s financial negligence. With 31,600 divorces recorded in Pennsylvania in 2021 alone, thousands of residents face this exact struggle. You deserve to stop feeling anxious about loan denials and start building a legacy that belongs solely to you. Learning how to fix credit after divorce Philadelphia is the first step toward true independence.

We understand the resentment of watching your score drop below the 2023 Philadelphia average of 669 because of a former partner’s choices. You shouldn’t have to carry that burden while trying to start a new chapter. We promise to show you the exact process for separating your financial identity and restoring your credit score to 700 or higher. This guide provides a methodical roadmap to help you dispute derogatory items, manage joint accounts, and master the art of individual financial restoration so you can take back control for good.

Key Takeaways

- Learn why a Philadelphia divorce decree doesn’t legally bind your creditors and how to shield your FICO score from shared liability.

- Master how to fix credit after divorce Philadelphia by identifying critical discrepancies between your legal settlement and your active credit tradelines.

- Take back control of your financial identity by systematically closing joint accounts and disputing derogatory items that hinder your progress.

- Establish a new financial legacy through strategic individual tradelines and secured cards designed to prove your independent creditworthiness.

- Discover how a personalized consulting strategy can navigate the complex overlap of Pennsylvania equitable distribution and credit bureau rules.

Why Divorce Impacts Your Philadelphia Credit Profile

A Philadelphia divorce decree is a powerful legal document, but it lacks the authority to rewrite your contracts with lenders. Many residents mistakenly believe that if a judge assigns a debt to their ex-spouse, they are personally shielded from the fallout. This is a dangerous misconception. Creditors were not parties to your divorce case. They still view you as legally responsible for any joint accounts you signed for during the marriage. If you want to master how to fix credit after divorce Philadelphia, you must first accept that your financial reputation is still tied to your former partner until you take proactive steps to sever those links.

Pennsylvania operates under the principle of equitable distribution. This means a court divides marital property and debt based on what is fair, not necessarily a 50/50 split. While this process is designed for justice, it creates a massive gap in credit security. If your ex-spouse is ordered to pay off a joint Visa card but fails to do so, the bank will report the late payment on both of your credit reports. Understanding what a credit score is helps clarify why this happens. Your score is a reflection of your individual contract with the lender, and that contract remains active regardless of your marital status.

The Disconnect Between Law and Lenders

A judge in a Philadelphia courtroom cannot override federal credit reporting guidelines. Banks rely on “joint and several liability,” which means they can pursue either person for the full amount of a debt. If your name is on the note, you are on the hook. You must distinguish between being a primary joint account holder and an authorized user. Authorized users can often be removed with a simple phone call, but joint owners require a full account closure or a formal refinance to achieve total separation. If you don’t act, your ex-spouse’s financial choices will continue to dictate your borrowing power.

Common Post-Divorce Credit Pitfalls in Philly

Financial negligence often lingers long after the moving trucks have left. We frequently see clients struggling with derogatory items from “forgotten” bills that impact their ability to move forward. These often include:

- Late payments on an auto loan for a car your ex-spouse kept, which still appears on your report.

- Maxed-out retail cards from local Philadelphia shops that were never officially closed.

- Unpaid utility balances from a previous shared residence in Manayunk or Center City that went to collections.

Spousal credit sabotage is a real threat. Even if it isn’t malicious, simple forgetfulness can tank your FICO score. Taking back control requires a clinical audit of every tradeline to ensure your ex-spouse’s future mistakes don’t become your financial prison. You deserve a clean slate, and that starts with identifying every shared liability that still exists today.

Step 1: Auditing Your Post-Divorce Credit Report for Errors

Requesting your comprehensive reports from Equifax, Experian, and TransUnion is your first move toward freedom. You must see exactly what the creditors see before you can challenge it. As you learn how to fix credit after divorce Philadelphia, you will discover that inaccuracies are frequent. Philadelphia residents often find that their ex-spouse’s new address or name variations are still linked to their own profile. This creates a data bridge that can drag your score down if your former partner misses a payment on a new, unrelated account. If you spot these links, you must act to sever them immediately.

The reality of joint debt after a divorce is that collectors can still pursue you for any account where your signature remains. Your divorce decree does not automatically update the credit bureaus’ records. Your strategy for how to fix credit after divorce Philadelphia relies on a clinical audit of your active tradelines. If you feel overwhelmed by the volume of data on your reports, seeking a professional credit specialist can help you cut through the noise and identify the most damaging errors.

Identifying Divorce-Specific Inaccuracies

Look for accounts that were supposed to be assumed by your ex-spouse. Sometimes, a lender agrees to remove one person from a loan, but the paperwork never reaches the credit bureaus. You also need to verify that your name was removed as an authorized user on your ex’s individual cards. Even if you don’t have the physical card, their high balances can still spike your credit utilization ratio. Detecting unauthorized accounts opened during the separation period is also vital, as these represent a form of credit sabotage that must be disputed.

Organizing Your Documentation for Disputes

You need a Mastery Folder to house your final divorce decree and property settlement agreement. These documents are your evidence. If the court ordered you to satisfy a specific debt, keep the proof of payment handy. Having these papers organized ensures you are ready to dispute any derogatory items that shouldn’t be there. You are building a case for your financial independence. A tailored consulting strategy can help you organize this evidence effectively to ensure your disputes are legally sound and persuasive to the bureaus.

Strategy: Separating Financial Identities and Disputing Inaccuracies

Closing every joint account is the only way to guarantee your ex-spouse’s future spending won’t haunt your credit report. If you leave a shared retail card or bank account open, you remain 100% liable for the balance, regardless of what your divorce decree says. You must systematically contact each creditor to request a formal account closure. This proactive step prevents new derogatory items from appearing on your profile. Mastering how to fix credit after divorce Philadelphia requires this level of clinical detachment from your past financial life.

Disputing inaccuracies is your next priority. You have a legal right to a credit report that is accurate, timely, and verifiable. If a lender cannot prove a debt is yours or if they report the same late payment twice, it must be removed. Your path to independence depends on knowing how to fix credit after divorce Philadelphia by challenging every unverifiable mark. We use “Expert Reassurance” letters to communicate with bureaus, ensuring they understand the specific separation of liability. This isn’t about hiding debt; it’s about forcing creditors to adhere to the high standards of federal reporting laws.

The Art of the Effective Dispute

Writing a dispute letter that bureaus can’t ignore requires precision. You must avoid generic templates that look like automated spam. Instead, cite the Credit Repair Organizations Act (CROA) to remind bureaus of your consumer rights. Simply stating “I’m divorced” isn’t enough to win a dispute because banks care about contracts, not marital status. To succeed, your dispute should include:

- The specific account number and the exact error being reported.

- A clear explanation of why the data is inaccurate or unverifiable.

- Supporting evidence, such as a letter from a creditor confirming an account was closed.

- A formal request for the item’s immediate deletion or correction.

Handling Stubborn Joint Debts

Refinancing is the ultimate solution for large joint liabilities like mortgages or auto loans. If your ex-spouse keeps the house, they must refinance the loan into their individual name to remove yours from the debt. If they refuse to comply with the court’s financial terms, your credit score could suffer for years. In these complex cases, you may need a credit score specialist Philadelphia to intervene. A specialist can help you build a personalized strategy to mitigate the damage and protect your individual borrowing power while you resolve the dispute through the proper channels. Take back control by ensuring your name is no longer tied to assets you don’t own.

Building Your Individual Financial Legacy in Philadelphia

Restoring your financial reputation is about more than just erasing the past; it is about constructing a future that belongs to you alone. Once you have cleared the wreckage of joint accounts, you must prove your independent creditworthiness to lenders. This is a critical phase in learning how to fix credit after divorce Philadelphia. You are no longer half of a financial unit. You are now the sole architect of your FICO score. Establishing new, individual tradelines allows you to demonstrate that you can manage debt responsibly on your own terms. This process transforms your credit from a source of anxiety into a tool for empowerment.

Monitoring your credit utilization ratio strictly during the first 12 months post-divorce is essential for a rapid recovery. Your utilization, which is the amount of credit you use compared to your limits, accounts for 30% of your score. Keeping these balances below 10% will signal to bureaus that you are a low-risk individual. If you maintain this discipline, you will see your score climb steadily. You deserve a clean slate, and building individual history is the most effective way to achieve it.

Establishing New Credit Lines

Choosing the right local institutions can accelerate your recovery. Philadelphia Federal Credit Union (PFCU) provides excellent tools for this transition, such as credit-builder loans ranging from $250 to $1,000. These loans act as a forced savings plan while reporting positive payment history to the bureaus. Secured credit cards also serve as a vital foundation for your new identity. As of May 2026, the average interest rate for new credit card offers sits at 22.12%. Look for cards with lower annual fees or those that transition to unsecured lines after a period of perfect payment history. Avoid predatory lenders who target the recently divorced with sky-high fees and subprime terms.

Long-Term Credit Education

Maintaining a 700+ score while managing a single-income household requires a shift in mindset. You must understand the impact of new inquiries as you rebuild your life. Every application for a car loan or a new apartment in neighborhoods like Brewerytown or Old City can cause a temporary dip in your numbers. True restoration isn’t a one-time event; it is a permanent life skill. You can learn more about credit education Philadelphia to ensure you never fall back into the traps of the past. Mastery over your finances is the ultimate solution to instability.

If you want to move from a state of worry to a state of action, you need a plan that accounts for your unique Philadelphia lifestyle. You have the power to achieve mastery over your numbers and take back control of your legacy. Consult with a credit score specialist today to design your personalized path to financial freedom.

Navigating Post-Divorce Credit Restoration with AA Credit Master

Achieving financial independence requires more than just a list of steps; it requires a partner who understands the high stakes of a post-divorce economy. Allen & Allen, Inc. serves as your Financial Guardian in this journey. We offer the expert reassurance you need to move from a place of anxiety to a position of strength. Our Philadelphia based consultants specialize in the nuances of local credit reporting, ensuring that your path forward is clear and professional. You don’t have to face the credit bureaus alone. We provide the tools and strategy to help you take back control of your financial reputation.

Compliance is the cornerstone of our relationship with every client. We operate in full accordance with the Credit Repair Organizations Act (CROA). This federal law ensures consumer protection by requiring that fees for credit restoration services are only collected after the service has been fully performed. This performance based model aligns our success with yours. Learning how to fix credit after divorce Philadelphia becomes a manageable, transparent process when you have a seasoned mentor by your side. We prioritize your long term stability over quick, temporary fixes.

Our Personalized Consulting Process

Success begins with a deep dive review of your post-divorce credit reports from all three major bureaus. We don’t use generic software that ignores the human element of your story. Instead, a dedicated consultant identifies the specific derogatory items and joint liabilities that are holding you back. We then develop a customized roadmap designed to meet your specific life goals. If you want to qualify for a mortgage on a new home in Philadelphia, we focus on the exact metrics lenders in our region look for. This human centered approach ensures that every dispute and every new tradeline serves your ultimate vision of freedom.

Join the Ranks of Philly Credit Masters

Philadelphia residents trust Allen & Allen, Inc. because we treat credit management as a vital life skill. We move you beyond the “quick fix” mentality and into a state of financial mastery. This transition is essential for anyone rebuilding their life after a significant transition. You are not just a number; you are a person building a new legacy for your family. By mastering how to fix credit after divorce Philadelphia, you ensure that your future is never again limited by a former partner’s financial choices. You have the power to achieve a 700+ FICO score and maintain it through any life change.

Your journey toward a clean, individual credit report starts with a single, decisive action. Stop letting the past dictate your borrowing power and start investing in your independent future. We are ready to stand between you and the impersonal credit institutions that ignore your divorce decree. Schedule your post-performance credit consultation today and begin the process of mastering your financial destiny.

Your New Financial Chapter Starts Now

Securing your individual financial legacy is a proactive choice. You’ve learned that a divorce decree doesn’t stop creditors from reporting joint debt, but you now have the tools to sever those ties for good. By auditing your reports for Philadelphia-specific errors and establishing new individual tradelines, you can rebuild a score that reflects your personal responsibility. You deserve a future where your borrowing power is no longer tethered to the past. Mastering how to fix credit after divorce Philadelphia is the first step toward that permanent freedom.

Our team has served as Philadelphia-based experts since we were founded. We offer tailored resources for both individual and business credit to ensure your recovery is comprehensive. We maintain strict CROA compliance, which means we only charge fees after we perform the work. This professional, non-judgmental approach provides the expert reassurance you need to navigate this transition with absolute confidence. Join the 31,600 Pennsylvanians who navigate this process annually by choosing to prioritize your financial health. Take back control of your credit; consult with a Philadelphia Master Mentor today. You have the strength to achieve mastery over your numbers and build a lasting legacy.

Frequently Asked Questions

Does my divorce decree automatically remove my name from joint debts?

No, your divorce decree is a legal agreement between you and your ex spouse, not a contract with your creditors. Banks and lenders were not parties to your divorce case and are not bound by the judge’s order. You must proactively contact each creditor to request a release of liability or refinance the debt into an individual name to stop it from appearing on your report.

Can I sue my ex-spouse for ruining my credit in Philadelphia?

You cannot typically sue for credit damage as a standalone civil claim, but you can file a petition for contempt in Philadelphia Family Court. If your former partner violates the financial terms of your property settlement agreement, a judge can order them to satisfy the debt or reimburse you for losses. Since we don’t provide legal services, you should consult a family law attorney to discuss enforcing your decree.

How long does it take to fix my credit after a divorce?

Initial results from disputing inaccuracies usually appear within 90 to 180 days. However, restoring your score to a 700+ level often requires 12 to 24 months of consistent, individual payment history. The exact timeline depends on the volume of derogatory items and how quickly you can establish new, positive tradelines in your own name.

Should I close all my joint credit cards immediately after separating?

Closing joint accounts is generally the best way to prevent your ex-spouse from accruing new debt that you are legally liable for. While closing an account can temporarily lower your credit age, it’s a necessary step to achieve total financial separation. Ensure you have at least one individual credit card established before you begin shutting down shared lines to maintain your own credit access.

Will my ex-spouse be notified if I dispute a joint account error?

Credit bureaus do not send a formal notification to your ex-spouse when you initiate a dispute. However, if the creditor updates the account status to “disputed” on both reports, your ex might see that marker on their own profile. If the dispute results in the deletion of a negative item, it often benefits both of your scores simultaneously by removing the shared derogatory data.

What is the best way to build credit in my own name if I haven’t worked in years?

Secured credit cards and credit builder loans are the most effective tools for those with employment gaps. Philadelphia Federal Credit Union offers credit builder loans from $250 to $1,000 that allow you to prove your reliability without a high-income requirement. These small, managed lines of credit report directly to the bureaus and form the foundation of your new, independent financial identity.

Can a credit score specialist in Philadelphia help with divorce-related errors?

A credit score specialist provides the expert reassurance and technical knowledge needed to navigate how to fix credit after divorce Philadelphia. We identify name variations and old addresses that link your profile to your ex’s new financial activity. Our consultants create a personalized strategy that goes beyond generic software to address the specific inaccuracies that often follow a Pennsylvania divorce.

What happens if my ex-spouse files for bankruptcy on our joint debts?

You remain 100% liable for the full balance of any joint debt if your ex-spouse files for bankruptcy. The bankruptcy court’s stay protects them, but it doesn’t stop creditors from pursuing you for the $5,900 average credit card debt currently seen in Pennsylvania. You must act quickly to settle or restructure these accounts to prevent a major derogatory event on your individual credit report.