How to Read My Experian Report: A Philadelphia Resident’s Guide to Credit Accuracy

What if the only thing standing between you and a lower interest rate on a Philadelphia home loan is a single line of technical jargon you haven’t decoded yet? It’s natural to feel a spike of anxiety when looking at a dense wall of numbers and codes that seem designed to confuse you. You’ve likely felt the weight of financial uncertainty, but learning how to read my Experian report Philadelphia residents use to secure their goals is the first step toward reclaiming your personal autonomy. You deserve a report that accurately reflects your hard work rather than one filled with hidden reporting errors.

This guide will help you master every section of your credit layout so you can spot inaccuracies before they affect your life milestones. We’ll provide a clear roadmap for credit restoration and explain how to leverage your rights, including the fact that Philadelphia law generally prevents most local employers from using your credit history in hiring decisions. You’re about to transform your confusion into a strategic advantage. We will break down the technical terminology and show you exactly how to audit your own data to ensure your financial narrative remains under your control.

Key Takeaways

- Master the structural layout of your credit file to navigate complex data with the confidence of a professional auditor.

- Learn exactly how to read my Experian report Philadelphia residents use to identify common regional errors like merged files and duplicate collection entries.

- Spot the red flags that signal reporting inaccuracies, protecting your ability to secure competitive interest rates in the local housing market.

- Leverage your rights under the Fair Credit Reporting Act (FCRA) to document errors and launch a methodical path toward restoration.

- Discover how the personalized mentorship at Allen & Allen, Inc. helps you conquer financial management as a permanent capability rather than a temporary fix.

Decoding the Experian Report Layout for Philadelphians

Unlock lower monthly payments by auditing your financial data today. Your Experian credit report is a detailed record of your financial reliability, acting as a living resume that lenders review before deciding your future. Securing better interest rates in the competitive Philadelphia real estate market depends entirely on maintaining a clean report. Whether you’re looking at a rowhouse in Fishtown or a condo in Center City, your credit score and the underlying data dictate your fiscal terms. Learning how to read my Experian report Philadelphia residents use to unlock these terms is the first step toward mastering your finances in Philadelphia.

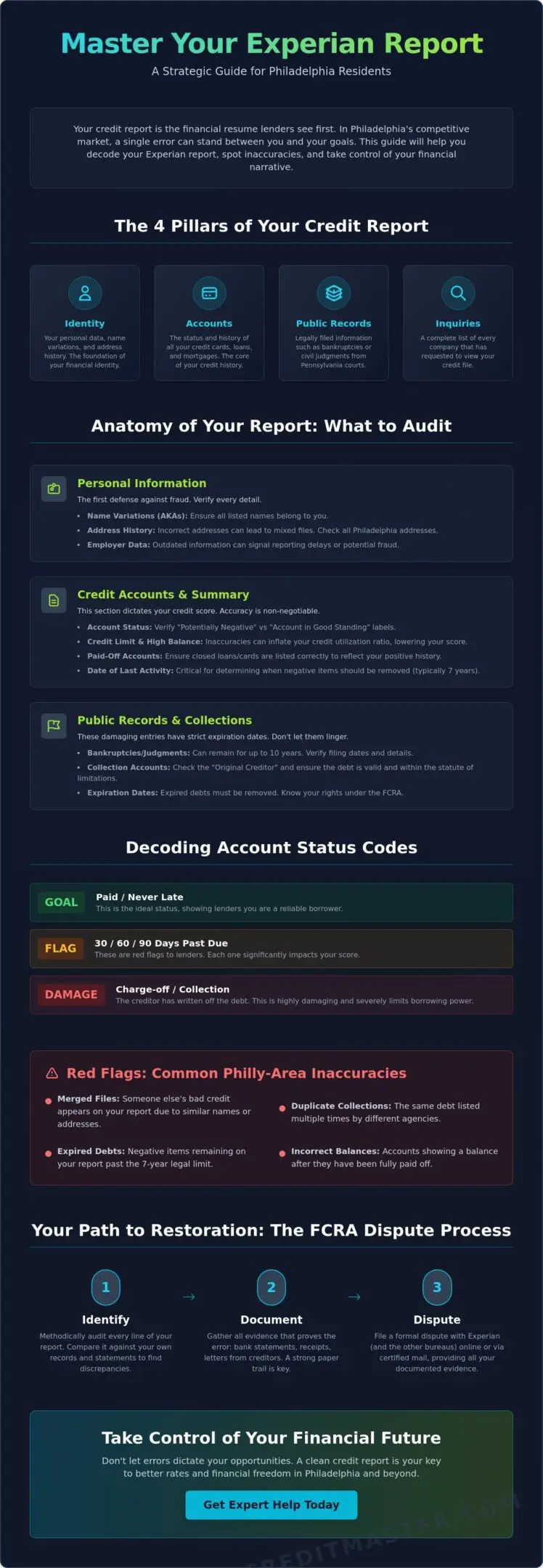

Your report is not a static grade; it’s a narrative of your reliability. Every document rests on four primary pillars:

- Identity: Your personal data and address history.

- Accounts: The status of your credit cards, loans, and mortgages.

- Public Records: Legal filings like bankruptcies.

- Inquiries: A list of who has viewed your credit file.

Mastering these sections allows you to spot errors that could be dragging down your potential. You can’t fix what you don’t understand, so approach this layout with the precision of a professional auditor.

The Header and Personal Information Section

Your name variations and previous Philadelphia addresses matter more than you think. Inaccurate address history often leads to “mixed files” where someone else’s bad habits end up on your report. Check for “Also Known As” (AKA) entries that don’t belong to you. These are often the first signs of identity theft. Similarly, incorrect employer data signals outdated reporting or potential fraud. Cleaning this section establishes a solid foundation for your financial identity and prevents confusion during loan applications.

The Summary of Accounts

This section acts as the table of contents for your financial health. It provides an immediate overview of your total debt load and credit utilization ratios. Pay close attention to the “Potentially Negative” versus “Account in Good Standing” labels. A single account mislabeled as “negative” can trigger higher insurance premiums or loan denials. Understanding how to read my Experian report Philadelphia involves verifying that every “good” account is actually working in your favor. If a paid-off loan is missing or listed incorrectly, you’re losing valuable history that proves your stability.

Section-by-Section Breakdown: What to Look For

Mastering the details in your Credit Account section turns a confusing document into a powerful financial tool. This area is the meat of your report, listing every credit card, mortgage, and auto loan tied to your name. You must verify that the “High Balance” and “Credit Limit” fields are accurate. Inaccuracies here can artificially inflate your utilization ratio, which directly suppresses your score. If you find discrepancies, the CFPB offers detailed guidance on how to read credit reports to ensure every field aligns with your actual bank statements.

The Public Records section requires your immediate attention because it documents legal actions from Pennsylvania courts. Bankruptcies or civil judgments filed in Philly can remain on your report for up to ten years, severely limiting your borrowing power. Similarly, the Collections section lists debts sold to third-party agencies. You must verify the “Original Creditor” and the “Date of Last Activity.” This date is vital. It dictates when the item must legally fall off your report, usually after seven years. Knowing how to read my Experian report Philadelphia residents often find that expired debts are still lingering, dragging down their financial potential.

Understanding Account Status Codes

Deciphering status codes is a skill that protects your future. A “Paid/Never Late” status is the goal, but “30/60/90 Days Past Due” indicators act as red flags to lenders. If you see a “Charge-off” status, it means the creditor has written the debt off as a loss. This status is particularly damaging if you’re trying to secure a Philadelphia business line of credit. Always identify the “Date of First Delinquency.” This specific date determines the entire reporting timeline and ensures your accounts don’t haunt you longer than the law allows.

Inquiries and Their Impact

Your inquiry section distinguishes between “Hard” and “Soft” pulls. Hard inquiries occur when you apply for credit. Too many of these, such as multiple hits from Philly auto dealers in a short window, can temporarily lower your score. Verify that every hard inquiry listed was actually authorized by you. In contrast, soft inquiries don’t affect your score at all. These occur during background checks or when you work with a credit score specialist at Allen & Allen, Inc. to review your file. Monitoring these entries ensures no unauthorized person is attempting to open accounts in your name, keeping your financial identity secure.

Spotting Red Flags and Common Inaccuracies in Philly

Your credit score might be suffering because of someone else’s financial mistakes. In a densely populated city like Philadelphia, “merged files” are a frequent and frustrating reality. This occurs when the credit bureau combines your data with that of another person who has a similar name or Social Security number. If you share a common surname, knowing how to read my Experian report Philadelphia residents rely on is vital to ensure your file isn’t cluttered with a stranger’s late payments or high debt levels. You shouldn’t have to pay the price for a clerical error in a database.

Duplicate reporting is another red flag that can artificially suppress your score. This happens when an original creditor sells your debt to a collection agency, and both entities continue to report the balance. Lenders see this as two separate debts, which doubles the damage to your credit profile. You must also watch for outdated information. Under federal law, most negative accounts must “age off” your report after seven years. If you find these lingering ghosts, you should dispute errors on your credit report to force their removal. Finally, check your credit limits. If a lender under-reports your limit, your utilization rate appears much higher than it actually is, making you look like a high-risk borrower to local banks.

The Danger of “Zombie” Debts

Zombie debts are old accounts that have been sold to new collectors who then re-report them with “new” dates. This illegal tactic makes an old debt look recent, extending its stay on your report. In Pennsylvania, the statute of limitations for most consumer debt is four years, meaning collectors lose their right to sue you after that period. However, they can still report it for seven years. These complex errors often require expert credit repair services in Philadelphia provided by Allen & Allen, Inc. to resolve effectively. We help you identify these re-aging tactics and hold bureaus accountable for their reporting accuracy.

Inaccurate Balance Reporting

Timing is everything when you’re applying for a mortgage or a car loan. Check the “Balance Date” on every account to ensure it reflects your most recent payments. If you’ve paid off a credit card but the report shows a high balance from three months ago, your debt-to-income ratio will look inflated. This single discrepancy can block a mortgage approval in the Philly market. You must also verify that any account marked as “Closed” does not show an active balance. A closed account with a balance suggests you still owe money, which can confuse automated underwriting systems and lead to an instant denial.

The Path to Restoration: Disputing Experian Errors

Take back control of your financial story by leveraging the Fair Credit Reporting Act (FCRA). This federal law serves as your primary shield for accuracy, ensuring that every piece of data on your report is verifiable and timely. Once you have identified inaccuracies while learning how to read my Experian report Philadelphia residents often find, you must act with precision. You aren’t just correcting a number; you’re restoring your reputation in the eyes of local lenders. Secure the accuracy you deserve by following a methodical, evidence-based approach to every dispute you file.

Avoid the “click-to-dispute” buttons found on many bureau websites. While these tools appear convenient, they often limit your ability to provide detailed evidence and may even waive your right to future legal recourse. Instead, draft a formal dispute letter and send it via certified mail. This creates a physical paper trail that forces the bureau to take your claim seriously. Once they receive your package, the law requires them to complete an investigation within a 30-day window. Tracking this timeline is essential, as a failure to respond within the legal limit can result in the automatic removal of the disputed item.

Why Documentation is Everything

Proof is the only currency credit bureaus accept. To remove an inaccurate account, you must provide concrete evidence such as bank statements, canceled checks, or letters from the original creditor confirming a balance of zero. Organize your Philadelphia financial records by account number and date to ensure your package is undeniable. Under the Fair Credit Reporting Act, bureaus must respond to your documented dispute within 30 days or remove the unverified information from your file. Providing clear, organized documentation significantly increases your chances of a permanent correction on the first attempt.

Navigating Complex Disputes

Expect some resistance when a creditor “verifies” inaccurate information as correct. This common hurdle occurs when the bureau’s automated system performs a surface-level check rather than a deep audit. In Philadelphia, you’re also protected by the Credit Repair Organizations Act (CROA), which regulates how professional services must operate on your behalf. If a bureau refuses to correct a documented error, escalate your complaint to the Consumer Financial Protection Bureau (CFPB). Seeking foundational credit education in Philadelphia before you begin ensures you understand the nuances of these laws. If you’re feeling overwhelmed by the technical requirements, consult with a credit specialist to build a personalized strategy for your restoration journey.

Partnering with a Philadelphia Credit Score Specialist

Partnering with a specialist provides a level of expert reassurance that automated software simply cannot match. While large credit bureaus push their own subscription monitoring tools, those systems often fail to address the nuances of your unique financial story. We act as your seasoned mentor, offering a clear path forward that prioritizes your long-term stability over temporary fixes. AA Credit Master stands as a powerful ally between you and large, impersonal institutions to ensure your voice is heard and your rights are respected. Our post-performance fee structure reflects our commitment to your success, as we prioritize results before payment.

Learning how to read my Experian report Philadelphia residents often discover is only the first step in a larger journey of skill acquisition. Once you’ve identified the technical errors and “zombie” debts, you need a proactive strategy to remove them permanently. We don’t just offer a service; we provide foundational knowledge that transforms financial management into a capability you can conquer. This human-led approach ensures that your specific challenges are met with personalized solutions rather than generic, automated templates that often lead to “verified” errors and further frustration.

Tailored Philadelphia Credit Consulting

A one-size-fits-all repair kit rarely works for the specific lending landscape of the Delaware Valley. Our local team understands the criteria used by Philadelphia banks and credit unions, allowing us to tailor your strategy to the local market. We maintain a strict commitment to the Credit Repair Organizations Act (CROA) to ensure your total protection throughout the consulting process. You deserve a professional who has navigated these complex systems many times and knows exactly where the pitfalls lie. This local expertise gives you a distinct advantage when you’re ready to apply for a mortgage or a business line of credit.

Your Future Beyond the Score

Frame your credit profile as a skill to be mastered for life rather than just a static number for a loan. Mastering your financial narrative leads to personal autonomy and the ability to build generational wealth for your family. You’re creating a permanent solution that will provide you with better fiscal terms for decades to come. Once you’ve secured your personal accuracy, you can take the next step toward building business credit in Philadelphia to fuel your entrepreneurial goals. Reclaim your financial narrative today with AA Credit Master and turn your worry into a state of decisive action.

Reclaim Your Financial Future in Philadelphia

Mastering the technical structure of your credit file is the foundation for your long-term restoration. You’ve learned how to identify the subtle red flags, from merged files to inaccurate balance reporting, that often go unnoticed by automated tools. Understanding how to read my Experian report Philadelphia residents rely on allows you to move from a state of worry to a state of decisive action. You now possess the strategic knowledge to audit your own data and hold large institutions accountable for every entry on your report.

Don’t let a single reporting error block your next major life milestone. As a dedicated member of the Philadelphia business community, we offer a personalized mentor-led strategy that prioritizes your autonomy. Our CROA-compliant post-performance fees ensure that we are invested in your success from the very beginning. Let a Philadelphia Credit Specialist Audit Your Experian Report Today. You deserve a clear path forward and a financial narrative that reflects your true reliability. Your better future starts with a single, expert-guided step.

Frequently Asked Questions

How do I get a truly free copy of my Experian report in Philadelphia?

Obtain your free weekly credit report through AnnualCreditReport.com, which is the only government-authorized source. Philadelphia residents also have the option to register directly with Experian for a free report at any time. This permanent extension of free weekly access allows you to monitor your file with the frequency required to maintain total accuracy and peace of mind.

Can I remove a legitimate late payment from my Experian report?

Accurate late payments generally remain on your report for seven years, but you can contact the creditor to request a goodwill adjustment. If the payment is incorrectly listed as late, you have the legal right to have it removed through a formal dispute. Learning how to read my Experian report Philadelphia residents find involves distinguishing between these permanent marks and removable reporting errors that drag down your score.

How long does it take for Experian to update my report after a dispute?

Experian must investigate and resolve your dispute within 30 days under the Fair Credit Reporting Act. This window can extend to 45 days if you submit additional evidence during the active investigation. Once the bureau verifies the error, they typically update your file within a few business days, though it may take a full billing cycle for all lenders to see the updated data.

What is the difference between an Experian credit report and a FICO score?

Your credit report is a detailed record of your financial history, while a FICO score is a three-digit number calculated from that data. Think of the report as your financial resume and the score as the grade a lender assigns based on that resume. Most reports from AnnualCreditReport.com don’t include a score, but Experian provides a free FICO Score with their direct membership.

Does checking my own Experian report lower my credit score?

Checking your own credit report is considered a soft inquiry and will never lower your credit score. You can review your file as often as you like to ensure its accuracy without fear of damaging your borrowing power. This proactive monitoring is a vital skill for anyone looking to build long-term financial stability and personal autonomy.

What should I do if my Philadelphia address is misspelled on my report?

Correct a misspelled Philadelphia address by filing a formal dispute with Experian immediately. While it seems like a minor clerical error, inaccurate address data can lead to merged files with individuals who have similar names. Keeping your personal information precise ensures that your financial narrative remains tied only to your own actions and protects you from identity confusion.

Is there a limit to how many errors I can dispute at once?

You can dispute as many errors as you find on your report at one time without any legal restriction. It’s often more effective to submit all identified inaccuracies in one comprehensive package to provide a clear picture of the necessary corrections. Be sure to include specific documentation for every item to ensure the bureau has the evidence required for a successful removal.

Can AA Credit Master help me read my report if I am confused by the codes?

AA Credit Master is a consulting company and credit score specialist dedicated to providing the education you need to decode complex reporting codes. We act as your mentor, helping you translate technical jargon into a clear roadmap for restoration. Understanding how to read my Experian report Philadelphia residents use is a capability we help you conquer so you can navigate the financial landscape with total confidence.