Choosing the Best Philadelphia Credit Restoration Company: 2026 Buying Guide

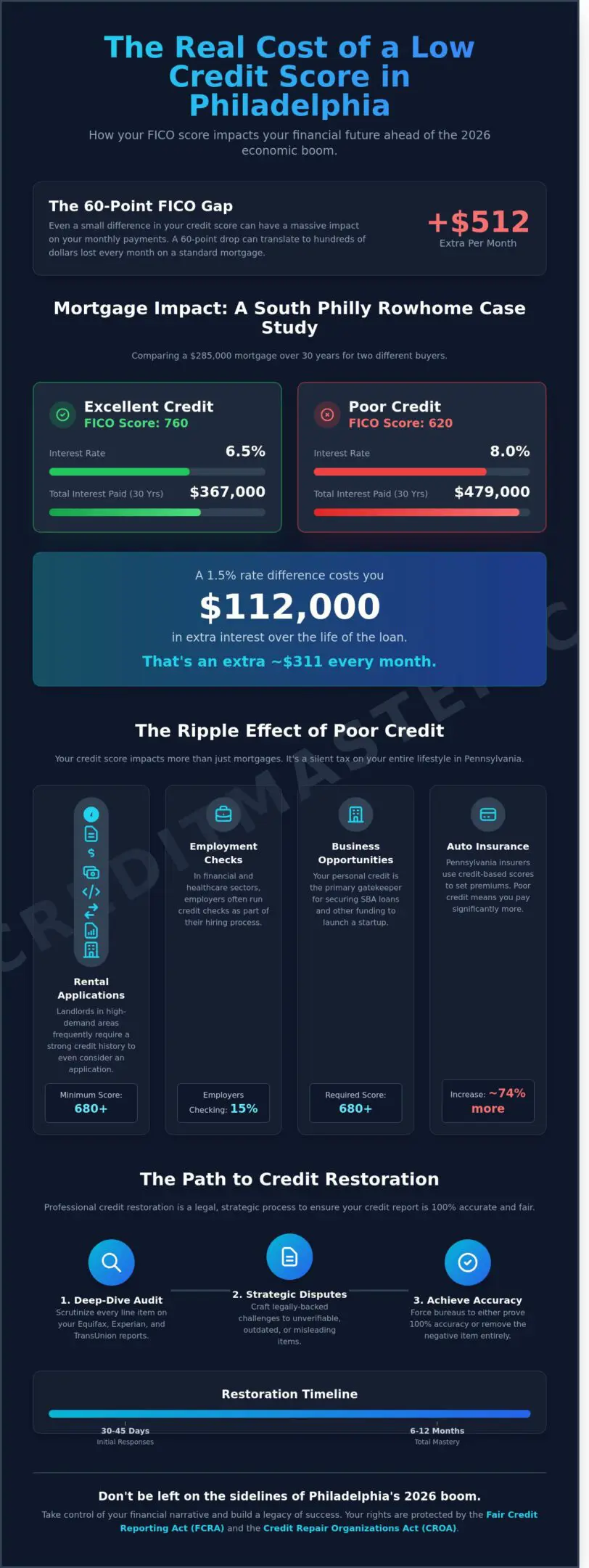

What if the only thing standing between you and a 3.5% interest rate on a Fairmount brownstone is a handful of fixable errors? In 2026, a 60-point FICO gap can mean paying an extra $512 every month on a standard mortgage. Finding a legitimate Philadelphia credit restoration company shouldn’t feel like a gamble. You deserve a partner who understands the clinical reality of credit reporting while offering the expert reassurance you need to move forward.

It’s frustrating to feel defined by past financial mistakes or confused by the complex legality of credit repair fees. We understand that the pressure of high interest rates creates a constant state of anxiety. This guide promises to provide a clear path to a 700+ FICO score by teaching you how to vet CROA-compliant experts who prioritize your financial literacy. You’ll learn the specific steps to dispute derogatory items effectively and lower your monthly debt payments for good. We’ll examine the five critical criteria for choosing a mentor who stands between you and impersonal credit bureaus so you can finally take back control.

Key Takeaways

- Secure lower mortgage rates in the 2026 Delaware Valley market by mastering how local lenders evaluate your credit risk profile.

- Navigate the complexities of the Fair Credit Reporting Act (FCRA) to strategically remove inaccurate data and rebuild your financial credibility.

- Protect your savings by identifying illegal “upfront fee” traps and predatory promises often used by unqualified firms.

- Partner with a compliant Philadelphia credit restoration company that prioritizes your success through a transparent, post-performance fee structure.

- Shift from financial worry to decisive action by learning the difference between temporary fixes and permanent financial literacy.

Why Your Credit Score is the Key to Philadelphia’s 2026 Economy

2026 is the year Philadelphia takes the global stage. Between the FIFA World Cup matches at Lincoln Financial Field and the 250th anniversary of the United States, our local economy is bracing for a massive capital surge. If you want to benefit from this growth, your financial profile must be flawless. Local lenders across the Delaware Valley are currently tightening their risk assessments. They view your FICO score as a badge of reliability. Partnering with a Philadelphia credit restoration company ensures you aren’t left on the sidelines while the city prospers. Mastery begins with understanding your credit score and its role as your financial passport.

The Real Cost of Low Credit in Philly

A low score is a silent tax on your lifestyle. Consider a $285,000 mortgage for a typical South Philly rowhome. A buyer with a 760 score might secure a 6.5% rate. A buyer with a 620 score could face 8% or higher. Over 30 years, that 1.5% gap costs you $112,000 in extra interest payments. In Pennsylvania, credit health also dictates your auto insurance costs. Drivers with poor credit pay roughly 74% more for premiums than those with stellar history. Even in high-demand rental markets like Northern Liberties, landlords now frequently require scores above 680 to even consider an application. If you don’t act, you’re paying a premium just to exist in the city.

- Mortgage Gap: A 150-point difference can cost $311 per month in extra interest.

- Insurance Impact: Pennsylvania insurers use credit-based insurance scores to set rates.

- Employment: 15% of local financial and healthcare employers now run credit checks on new hires.

Unlocking Business Opportunities in the City of Brotherly Love

Philadelphia is a hub for innovation, but growth requires capital. If you’re eyeing an SBA 7(a) loan to launch a startup, your personal credit is the primary gatekeeper. Most local banks require a minimum personal score of 680 for business funding. Restoring your credit is about more than just numbers; it’s about building a legacy. High scores allow you to leverage other people’s money to build your own wealth. A Philadelphia credit restoration company helps you transition from financial worry to total mastery. Take back control of your narrative before the 2026 boom begins. You deserve to own a piece of this city’s future.

How Professional Credit Restoration Works in Pennsylvania

Credit restoration is your legal right to a report that reflects the absolute truth of your financial history. It is a strategic, deep-dive audit of your credit files to identify and challenge inaccuracies. When you partner with a top-tier Philadelphia credit restoration company, you move beyond surface-level fixes. You engage in a process designed to hold creditors and bureaus accountable for the data they report about your life. This journey requires patience and precision. While initial responses from bureaus typically arrive within 30 to 45 days, achieving total mastery over your profile often takes 6 to 12 months of consistent effort.

The law is your most powerful tool in this fight. We navigate the complexities of the Fair Credit Reporting Act (FCRA) to ensure your rights remain protected. Our work is also governed by the Credit Repair Organizations Act, a federal statute passed in 1996 to ensure transparency and honesty in the industry. If you understand the rules of the system, then you can use them to your advantage. We prioritize mastery over simple repair because we want you to graduate with the financial literacy needed to maintain a high score for a lifetime. You are not just fixing a number; you are securing your legacy.

The Anatomy of a Credit Dispute

A successful dispute begins with identifying derogatory items that are unverifiable, outdated, or misleading. We scrutinize every line item on your reports from Equifax, Experian, and TransUnion. Generic dispute letters often fail because credit bureaus use sophisticated “e-OSCAR” automated systems to flag and dismiss boilerplate language. Professional consulting succeeds by craftly specific, legally-backed challenges that require a human being at the bureau to perform a manual investigation. This meticulous approach forces the bureaus to either prove the debt is 100 percent accurate or remove it entirely.

Beyond Deletions: Rebuilding Your Profile

Credit restoration is the legal right to an accurate report. Removing a negative item is only half of the equation. To achieve a score that opens doors, you must also focus on your credit mix and positive history. If you add two or three strategic tradelines, then your score can gain the “weight” it needs to impress local lenders. For Philadelphia residents aiming for homeownership, managing your debt-to-income ratio is essential. Most lenders in the Delaware Valley look for a ratio below 43 percent for conventional mortgage approval. You can take back control of your financial narrative by balancing aggressive disputes with smart profile building. This dual strategy ensures you aren’t just erasing the past, but actively constructing a prosperous future.

Legal Aid vs. DIY vs. Philadelphia Credit Restoration Companies

You have three primary paths to fix your credit in the Delaware Valley. Each serves a different financial state. Choosing the wrong one can cost you years of progress and thousands in interest. You must align your strategy with your ultimate goal, whether that is surviving a collection lawsuit or qualifying for a 3.5% down payment on a home.

When Free Legal Aid is the Right Choice

Community Legal Services (CLS) provides a vital safety net for Philadelphia residents. If your household income is below 200% of the federal poverty line, roughly $30,120 for an individual in 2024, they offer expert defense against predatory creditors. They excel at stopping illegal garnishments and defending you in Municipal Court. However, legal aid is reactive. Their primary mission is protection, not proactive score optimization. If you want to master your FICO score to secure a legacy for your family, legal aid lacks the specific tools for aggressive credit building. You should transition to a private Philadelphia credit restoration company once your immediate legal threats are neutralized.

The High Cost of DIY Mistakes

The “do-it-yourself” approach often feels like a cost-saving measure. It frequently becomes a expensive trap. Managing complex disputes requires more than just sending a template letter. If you submit an incorrectly phrased dispute, the credit bureaus may flag your file as “frivolous.” This label can effectively lock in negative data for 120 days or longer. Most individuals spend 10 to 15 hours per month tracking certified mail and deciphering bureau responses. Your time has a dollar value. Expert guidance provides a massive return on investment by avoiding these technical pitfalls.

- Technical Precision: Professionals understand the nuances of the Credit Repair Organizations Act (CROA) to ensure every action is compliant and effective.

- Strategic Sequencing: If you dispute items in the wrong order, you might accidentally verify a debt that was about to age off your report.

- Financial Impact: A 60-point score increase can save you $250 per month on a standard auto loan. That is $15,000 over a five-year term.

If you want to take back control, look for a partner that prioritizes personalized strategy over automated software. A reputable Philadelphia credit restoration company will analyze your specific derogatory items and create a roadmap for total financial literacy. This mastery ensures that once your credit is restored, it stays that way forever.

5 Red Flags to Avoid When Hiring a Philly Credit Repair Firm

Protecting your financial legacy starts with identifying predators who profit from your stress. Many residents searching for a Philadelphia credit restoration company fall victim to empty promises that lead to deeper debt. If a firm demands an upfront fee before they complete any work, they are violating the Credit Repair Organizations Act (CROA) of 1996. Federal law is clear; companies must provide results before collecting payment.

Scammers often use high-emotion language to mask illegal practices. Watch for these five warning signs:

- 100% Guaranteed Results: No legitimate expert can guarantee a specific FICO score increase because credit bureaus are independent entities.

- The “New Identity” Scam: If a firm suggests applying for a Credit Privacy Number (CPN), they are encouraging federal wire fraud. This carries a prison sentence of up to 30 years.

- Vague Service Agreements: A contract must include a clear “Mastery” plan. If it lacks specific timelines or educational goals, it is likely a template-based scam.

- Bureau Silence: You have a legal right to contact Equifax, Experian, or TransUnion directly. Any firm that discourages this is trying to hide their methods from you.

- Upfront Costs: Paying for “setup” or “consultation” before service delivery is a major compliance violation.

Understanding the Credit Repair Organizations Act (CROA)

The CROA protects you by requiring a written contract that outlines your rights. You have a legal three-day cooling-off period to cancel any agreement without penalty. Under Pennsylvania consumer protection laws, firms must also maintain a $10,000 bond to operate. If a firm cannot prove they are bonded, they aren’t qualified to handle your restoration. Post-performance billing is the only legal way to charge for these services.

The Importance of Personalized Strategy

Automated software misses the nuances of your financial life. A 2021 study by Consumer Reports found that 34% of Americans had at least one error on their credit reports. Generic dispute letters can’t fix complex derogatory items. You need a human Credit Score Specialist who asks about your goal to buy a home or lower your interest rates. A personalized resource plan for Philadelphia residents ensures your strategy aligns with local lending requirements. If you want to stop the cycle of rejection, you must take back control with a customized mastery plan today.

Master Your Future with AA Credit Master in Philadelphia

Located at 1515 Market Street, AA Credit Master serves as your dedicated financial guardian. We aren’t just another Philadelphia credit restoration company; we’re your partners in rebuilding a stable future. Our team operates on a post-performance fee model. This means our success is tied directly to your results. You pay for progress, not empty promises. This structure ensures we remain aggressive and focused on removing the barriers between you and your financial goals.

We provide tailored solutions for every stage of your journey. If you’re an individual looking to qualify for a mortgage, we clean up your personal profile. If you’re an entrepreneur, we build the business credit you need to scale. We focus on the clinical reality of your credit report while providing the expert reassurance you need to stay the course. You can’t achieve true freedom without mastery over your finances. We give you the tools to take back control.

The AA Credit Master Difference

Our consulting is professional, modern, and entirely non-judgmental. We understand that financial instability is stressful. We don’t dwell on the past; we focus on the solution. Financial literacy is our primary weapon. We treat credit management as a life skill rather than a temporary fix. Our expertise spans both personal FICO restoration and complex business credit landscapes. We help you navigate the system so you don’t have to face impersonal credit institutions alone.

Your Path Starts Here

Your journey begins with a meticulous review of your current credit reports. Data from the Federal Trade Commission suggests that 25% of consumers have errors on their credit reports that affect their scores. We find these mistakes. Our process is methodical and thorough. We identify derogatory items and dispute inaccuracies on your behalf using proven industry strategies. You can expect a clear, step by step breakdown of how we’ll rebuild your profile.

- Detailed analysis of derogatory items from all three bureaus.

- Customized dispute strategies for maximum impact.

- Ongoing education to ensure your score stays high.

- Direct access to seasoned credit mentors.

Stop letting a three-digit number dictate your life choices. You have the power to change your trajectory starting right now. Master your credit and take back control today.

Master Your Financial Destiny in the 2026 Philadelphia Market

Navigating the 2026 economy requires more than just a passing interest in your FICO score. You’ve discovered that securing a mortgage or a business loan in Pennsylvania often hinges on maintaining a score above 720. Avoiding common red flags like illegal upfront fees is the first step toward protecting your assets. Choosing a reputable Philadelphia credit restoration company ensures your path to recovery follows the strict guidelines of the Credit Repair Organizations Act (CROA).

AA Credit Master stands as your dedicated financial guardian at 1515 Market Street. We specialize in both personal and business credit restoration, utilizing a strictly CROA-compliant post-performance fee structure. This means you don’t pay for promises; you pay for verified results. Our team works directly with credit bureaus to challenge derogatory items that hold you back from your goals. It’s time to stop feeling overwhelmed by complex reports and start seeing tangible progress. We’re here to guide you through every dispute and rebuild every point until you achieve total mastery over your financial life.

Take back control of your financial legacy; consult with AA Credit Master

Your future is waiting, and we can’t wait to help you reach it.

Frequently Asked Questions

Is credit repair legal in Philadelphia?

Yes, credit repair is 100% legal in Philadelphia under the federal Credit Repair Organizations Act of 1996. This law gives you the right to challenge any information on your reports that is inaccurate, unfair, or unverified. Pennsylvania state laws provide additional consumer protections to ensure you aren’t exploited by predatory practices. If a bureau reports false data, you have the legal authority to demand its immediate removal.

How much does a Philadelphia credit restoration company cost?

Investing in a Philadelphia credit restoration company typically involves a monthly service fee ranging from $99 to $149. Most reputable firms also charge a one-time work fee of approximately $195 to perform a deep-dive audit of your three bureau reports. If you improve your score by 50 points, you could save over $200 a month on a standard auto loan. These costs are a small price for long-term financial freedom.

Can I remove accurate but negative information from my credit report?

Legally, accurate and verifiable information must remain on your credit report for 7 years, or 10 years for Chapter 7 bankruptcies. However, if a creditor fails to verify the data within the 30-day legal window, that item must be deleted regardless of its accuracy. We scrutinize every technical detail to find reporting errors that others miss. If the data is perfect, we focus on rebuilding your profile to outweigh those past mistakes.

How long does it take to see results with AA Credit Master?

You will typically see initial progress within 35 to 45 days of starting your personalized restoration plan. While 75% of our clients notice score movement in the first two months, reaching your ultimate goal usually requires 4 to 6 months of consistent effort. If you follow our step-by-step roadmap, you’ll gain the momentum needed to secure a mortgage or a new vehicle. We prioritize human expertise over generic software to accelerate your success.

What is the difference between credit repair and credit restoration?

Credit repair focuses on the narrow task of deleting specific errors, while credit restoration addresses your entire financial health. Repair might fix one late payment from 2022, but restoration builds a path to a 740 FICO score through total profile management. If you want more than a temporary fix, restoration provides the mastery needed to stay in control of your legacy. It is the difference between patching a leak and rebuilding the foundation.

Will checking my own credit report hurt my score?

Checking your own credit report is a soft inquiry and results in 0 points lost from your score. Unlike a hard pull from a lender which can drop your score by 5 to 10 points, self-monitoring is a safe and vital habit. We recommend reviewing your reports every 90 days to catch errors or signs of identity theft early. Take back control of your financial data without any fear of a penalty or a lower rating.

How does business credit differ from personal credit in Pennsylvania?

Business credit is tied to your Federal Tax ID or EIN rather than your Social Security number. While personal scores like FICO range from 300 to 850, business scores like the Dun & Bradstreet Paydex range from 0 to 100. Establishing a strong business profile allows you to secure credit limits that are often 10 times higher than personal accounts. Every Philadelphia credit restoration company client should understand this distinction to protect their personal assets from business liabilities.

What happens if the credit bureaus refuse to remove an error?

If a bureau refuses to correct a verified error, we escalate the dispute to the Consumer Financial Protection Bureau. Under the Fair Credit Reporting Act, bureaus must conduct a reasonable investigation or face significant legal consequences. We provide the specific documentation needed to force a re-investigation within the 60-day federal window. You don’t have to accept a rejection when the law is on your side and your financial future is at stake.