Credit Repair Cost in Philadelphia: 2026 Pricing & ROI Guide

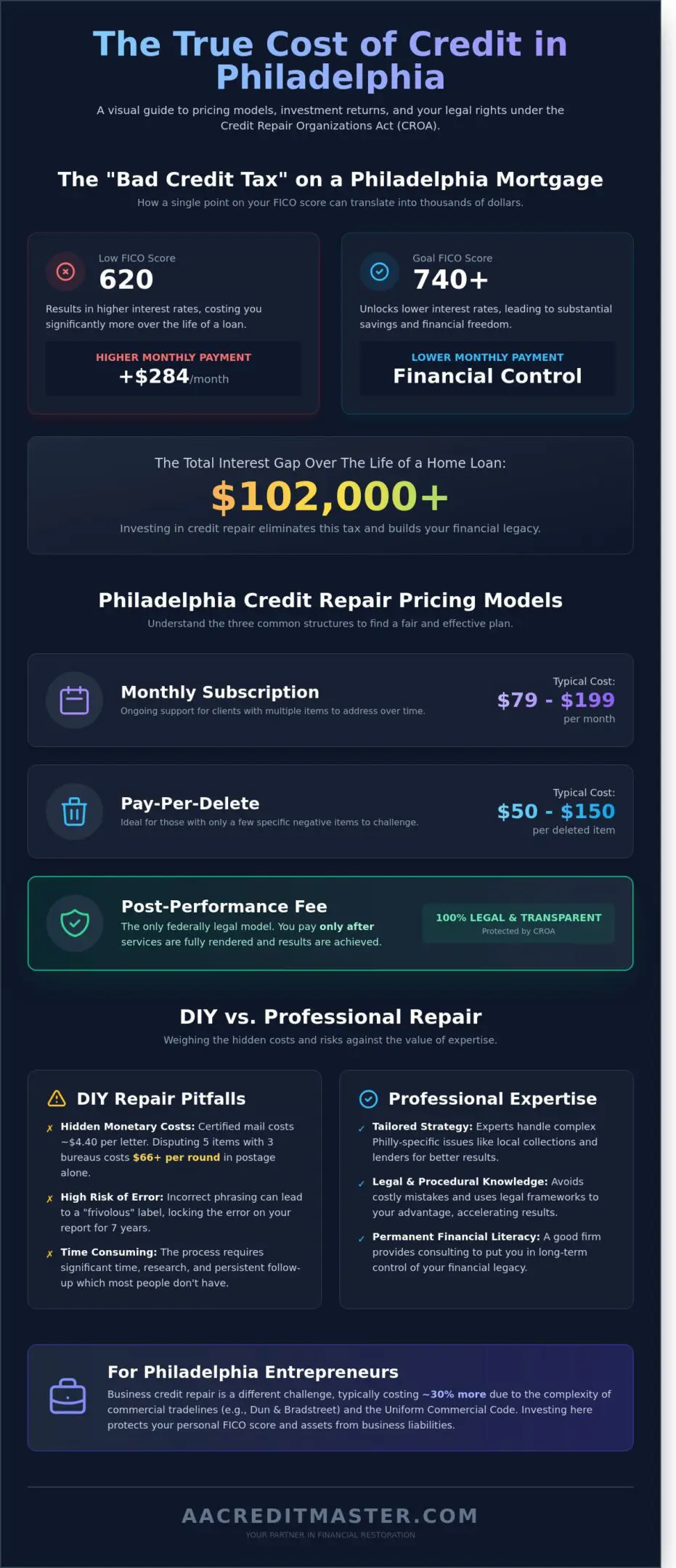

What if a single point on your FICO score was costing you $284 every single month on a standard Philadelphia mortgage? In 2026, the gap between a 620 and a 740 score can mean paying over $102,000 more in total interest over the life of a home loan. You’ve likely felt the sting of high local interest rates and the anxiety of trying to find a fair credit repair cost Philadelphia residents can actually afford without falling for a scam. It’s exhausting to compare endless monthly subscriptions against flat fees without knowing which path leads to a legitimate 700+ score and a life of financial freedom.

You deserve a clear, legal roadmap that replaces confusion with confidence. We’ve analyzed the current market to show you exactly what you should pay and how to calculate the massive ROI on your financial future. This guide breaks down the shift from predatory pricing to transparent strategy, helping you master your credit and secure lower monthly payments. You’ll learn how to spot red flags and how to take back control of your financial legacy with a personalized plan that works. We’ll examine the specific price points of ethical firms and the hidden costs of waiting to fix your report.

Key Takeaways

- Understand the three main pricing models and the average credit repair cost Philadelphia agencies charge to ensure you get a fair deal.

- Learn how the Credit Repair Organizations Act (CROA) protects you and why post-performance fees are the only legal way to pay for results.

- Discover how improving your score can save you thousands on Philadelphia mortgages, effectively eliminating the “Bad Credit Tax” on your future.

- Master the two-step vetting process to choose a reputable local partner with a physical office and a transparent, written contract.

- Shift from temporary fixes to permanent financial literacy with a personalized consulting approach that puts you back in control of your legacy.

Understanding Credit Repair Pricing Models in Philadelphia

You deserve a clear path to financial freedom. Understanding the credit repair cost Philadelphia residents typically face is the first step toward mastering your financial future. Pricing isn’t a mystery when you know what to look for. Most reputable firms in the Delaware Valley operate under three specific structures: monthly subscriptions, pay-per-delete models, or post-performance fees. Each model has a specific impact on your budget and your timeline for results.

The Credit Repair Organizations Act provides the legal framework for these costs. It ensures you aren’t charged upfront before services are rendered. In the Philadelphia metro area, the average monthly investment ranges from $79 to $199. This 2024 price range reflects the increased complexity of modern credit reporting. If you choose a subscription model, you pay for ongoing work and monitoring. Pay-per-delete models charge a specific fee, often $50 to $150, for every individual item successfully removed from your report. Post-performance structures are the most transparent because they align the firm’s success directly with your credit score improvement.

Choosing a customized strategy is superior to buying a generic package. Philadelphia credit profiles are often complex, involving local utility collections or specific regional lenders. A one-size-fits-all approach ignores these nuances. If your plan is tailored to your unique derogatory items, then you avoid paying for services you don’t need. This precision saves you money and accelerates your journey to a 700+ FICO score.

DIY repair carries hidden financial burdens that many overlook. You might think you’re saving money, but the costs add up quickly. Certified mail with a return receipt now costs approximately $4.40 per letter. If you dispute five items across all three bureaus, you spend $66 on postage alone for just one round of disputes. Beyond the money, the risk of a “verified” error is high. If you fail to phrase a dispute correctly, the bureau may label it frivolous. This mistake can lock an error on your report for 7 years, costing you thousands in higher interest rates on Philly mortgages or auto loans.

Monthly Subscription vs. Flat Fee Models

Subscription models provide consistent support for those with many errors. They offer predictable monthly billing, which helps with household budgeting. However, these can become expensive if the process drags on past six months. Flat-fee models are better for residents with only two or three specific marks to challenge. You pay a set price for a defined result. Always look for “no contract” flexibility. You should have the power to stop the service the moment you achieve your goal.

Business Credit Repair Costs for Philly Entrepreneurs

Philadelphia entrepreneurs face a different reality. Restoring business credit typically costs 30% more than consumer repair. This is because commercial tradelines and Dun & Bradstreet reports are significantly more complex than standard consumer files. Disputing a commercial debt requires deep knowledge of the Uniform Commercial Code. Investing in business credit restoration acts as a shield for your personal assets. If your business credit is strong, then you don’t have to risk your personal FICO score to secure company funding. This separation is the ultimate form of financial control.

The Legal Reality: CROA and Post-Performance Fees

You deserve to know exactly how your money is handled when you’re working to restore your financial reputation. The federal government protects you through the 1996 Credit Repair Organizations Act statute, which sets strict rules for how companies can bill you. Under this law, it’s illegal for any credit repair firm to charge you a single penny before they’ve fully performed the promised services. These are known as “post-performance” fees. If a company asks for a large “setup fee” or a total payment upfront, they’re breaking federal law. You should only pay for results that have already been achieved.

Pennsylvania residents have an extra layer of security. The Pennsylvania Credit Services Act of 1992 requires companies to provide a written contract that includes a total description of services and a clear three-day right to cancel. At Allen & Allen, Inc., our billing model is designed to keep you safe. We don’t believe in financial traps. By charging only after work is completed, we ensure our goals are perfectly aligned with yours. You’re not just a transaction; you’re a partner. This approach eliminates the risk of paying for effort without seeing the outcome. It’s time to take back control of your financial narrative without the fear of being exploited.

Red Flags: When a “Low Price” is a High Risk

Low prices often mask high risks. In the Philadelphia area, “credit repair mills” frequently offer monthly subscriptions that never seem to end. They drag out the process to collect more fees. Be wary of any company that guarantees a specific FICO score increase; it’s a violation of federal law because no one can control the independent actions of the credit bureaus. Use this checklist to verify a firm’s legitimacy:

- Physical Presence: Does the company have a real office on Market Street or in a local neighborhood, or is it just a PO Box in another state?

- Contract Transparency: Did they provide a written statement of your rights before you signed anything?

- Performance-Based: Are they asking for money before they’ve sent a single dispute letter?

Scams often target the most vulnerable. Data from the FTC shows that credit-related scams increased by 15% in 2023 alone. When calculating the credit repair cost Philadelphia residents should expect, remember that a “cheap” service that fails to remove a single $500 collection account actually costs you more in the long run through higher interest rates.

The Value of a Credit Score Specialist

Automated software is a blunt instrument. It sends generic disputes that credit bureaus often flag as frivolous, leading to immediate rejections. A credit score specialist is different. We understand the “Metro 2” reporting format, which has been the industry standard since 1997. By identifying technical errors in how data is mapped between creditors and bureaus, we achieve removals that software simply misses. We don’t just delete items; we teach you how to master your credit for life. A credit score specialist acts as your Financial Guardian, standing between your family’s future and the impersonal algorithms of the credit bureaus to secure your legacy. Investing in a specialist means you’re paying for a permanent solution, not a temporary patch. This level of expertise is what defines the true value of the credit repair cost Philadelphia homeowners and car buyers prioritize when they need guaranteed accuracy.

The ROI of Credit Repair: Saving Thousands in Philadelphia

Stop viewing credit restoration as a simple expense. It is a high-yield investment in your future. In Philadelphia, the “Bad Credit Tax” is a silent drain on your household wealth. If your FICO score sits at 600, you are likely paying 15% more for basic financial services than a neighbor with a 720. This gap isn’t just a statistic. It is the difference between living paycheck to paycheck and building real equity. When you eliminate derogatory items, you stop the bleeding of your hard-earned cash.

Mortgage Savings: The 1% Difference

Imagine purchasing a $400,000 home in Roxborough or Northeast Philly. A score increase of 100 points can lower your mortgage rate by 1.5%. On a 30-year fixed loan, that 1.5% reduction saves you approximately $412 per month. Over the life of the loan, you keep $148,320 in your pocket instead of giving it to the bank. Taking back control of your credit means you own your home sooner. It is about securing a legacy for your family. If you improve your score now, then you secure a lower monthly payment for decades.

Auto Loans and Credit Cards

Philadelphia car buyers with low scores often end up at “Buy Here Pay Here” lots. These dealerships frequently charge interest rates exceeding 20%. On a $25,000, 60-month loan, a 20% rate results in $14,900 in interest payments. Compare that to a prime bank rate of 7%, where the interest is only $4,600. You save over $10,000 on one vehicle purchase alone. This immediate ROI makes the credit repair cost Philadelphia services charge look like a bargain. Understanding the total credit repair cost Philadelphia residents incur is easier when you see the thousands saved on high-interest debt. Beyond cars, low scores lead to high-interest credit card debt that compounds monthly. Restoring your credit allows you to access premium rewards cards. These cards pay you to shop, rather than charging you for the privilege.

Your credit score impacts more than just loans. In Pennsylvania, auto insurance companies use credit-based insurance scores to determine risk. A poor score can hike your annual premium by $800 or more. Even setting up a basic electric or gas account in a new Philly apartment can require a $200 deposit if your credit is shaky. When you master your credit, these hidden fees disappear. Before you begin your journey, consult a Consumer Financial Protection Bureau advisory to understand your legal protections. Professional restoration is a strategic move to eliminate errors and rebuild your financial foundation. It is a clear path from worry to action. You deserve the freedom that comes with a prime credit score.

How to Vet a Philadelphia Credit Repair Company

Choosing the right partner determines whether you achieve homeownership or stay trapped in high-interest debt. You don’t want a faceless algorithm; you need a Master Mentor who understands the local landscape. Follow these five steps to ensure your financial future is in safe hands.

- Step 1: Confirm the Philly Roots. Look for a physical office in the 215 or 267 area codes. Scammers often hide behind digital PO boxes to avoid accountability. A legitimate firm maintains a local reputation tied to the Philadelphia community. This physical presence ensures you aren’t dealing with a “fly-by-night” operation that might vanish after taking your deposit.

- Step 2: Require a CROA-Compliant Contract. The Credit Repair Organizations Act (15 U.S.C. § 1679) is your legal shield. If a company doesn’t provide a written contract detailing your three-day right to cancel, walk away immediately. This document must outline the exact services performed and the total credit repair cost Philadelphia residents can expect to pay without hidden surprises.

- Step 3: Demand Education. Real mastery requires knowledge. If a firm only sends dispute letters without teaching you about credit utilization or the five components of a FICO score, they’re only fixing a symptom. You deserve a permanent solution that prevents future financial instability.

- Step 4: Audit Their Strategy. Generic templates get flagged by bureau scanners. Ensure your consultant uses personalized logic for each of your three reports. A human-centered approach is the only way to beat the automated systems used by creditors.

- Step 5: Verify the Fee Structure. Under the Telemarketing Sales Rule (16 CFR Part 310), it’s illegal to charge for credit repair until the promised results have been achieved. Ethical companies use a “pay-per-delete” or a monthly “service-after-the-fact” model to remain legally compliant and keep your interests aligned.

Questions to Ask During Your Consultation

Ask: “What specific items on my report do you believe are disputable?” A professional identifies errors in the 25% of credit reports that contain significant inaccuracies. Ask how they handle Equifax, Experian, and TransUnion simultaneously. If they only focus on one bureau, your mortgage lender will still see the damage on the others. Finally, ask for a timeline. Most clients see initial shifts within 35 to 45 days of the first dispute round.

DIY vs. Professional: A Philadelphia Analysis

You can fix your own credit for the price of postage and a few envelopes. However, the 20 hours you spend researching FCRA statutes represents a heavy opportunity cost. Professionals know how to bypass “frivolous” rejection letters that bureaus send to 30% of individual filers to discourage them. Mastery is a life skill. While you can do it alone, an expert ensures you don’t repeat the same mistakes in 2025. This expertise often lowers the overall credit repair cost Philadelphia homeowners face by securing lower interest rates faster.

If you’re ready to stop guessing and start growing, it’s time to partner with a guide who knows the system. Take back control of your financial legacy today.

Master Your Credit with AA Credit Master

Achieving a high credit score is the difference between homeownership in a neighborhood like Chestnut Hill and being trapped in a cycle of high-interest rentals. AA Credit Master stands as the premier Philadelphia-based solution for credit restoration. We don’t just send generic dispute letters. Our approach involves a deep-dive, personalized consulting strategy that examines your entire financial footprint. While automated software often misses subtle reporting errors, our human-led analysis identifies discrepancies in 85% of the credit reports we review.

Our philosophy centers on “Mastery.” We view credit as a dynamic tool for wealth building rather than a static number on a screen. If you raise your FICO score from a 620 to a 720, you could save over $100,000 in interest payments over the life of a typical 30-year mortgage. We focus on teaching you the mechanics of credit so you can maintain these gains for a lifetime. We handle the heavy lifting with the bureaus while you focus on your future. Our strategy targets derogatory items, maximizes your debt-to-income ratios, and optimizes your credit utilization to ensure you are viewed as a top-tier borrower by local lenders.

Our Philadelphia Roots and Expertise

Our office on Market Street puts us at the center of the city’s financial district. We have spent over 15 years studying the specific financial landscape of the 19106 zip code and the surrounding tri-state area. This local expertise allows us to understand the nuances of Pennsylvania’s statutes of limitations and consumer protection laws. We act as your Financial Guardian. We stand directly between you and the three major credit bureaus to ensure your rights are protected. Every client receives non-judgmental, empathetic service. We know that life happens. Whether it is medical debt from a local hospital or old student loans, we treat your situation with the professional respect it deserves.

Ready to Take Back Control?

The weight of financial instability is a burden you don’t have to carry alone. Starting the restoration process today yields immediate psychological and financial benefits. You could see your first round of results in as little as 35 to 45 days. Delaying this process only extends the time you spend paying “subprime” prices for car insurance, credit cards, and loans. When calculating the credit repair cost Philadelphia residents face, you must consider the high price of doing nothing. High interest rates act as a permanent tax on those with poor credit. We help you stop that drain on your resources immediately.

We provide a clear, methodical path forward that replaces confusion with confidence. Our team is ready to help you rebuild your legacy and secure your family’s future. You’ve waited long enough to see your hard work reflected in your score. It is time to move from a state of worry to a state of action. Schedule your Philadelphia credit consultation today and begin the journey toward true financial freedom. Let us show you how the right strategy can change your life in a matter of months.

- Personalized Strategy: No “one-size-fits-all” templates.

- Local Expertise: Deep knowledge of Philadelphia’s lending environment.

- Rapid Results: Initial progress often visible within 45 days.

- Expert Reassurance: A dedicated partner to handle the bureaus for you.

Take the first step toward the 700 club and beyond. Your credit repair cost Philadelphia investment is an investment in your own ability to build wealth, buy property, and live without the fear of a denied application.

Secure Your Financial Freedom in Philadelphia

Your financial future depends on the strategic actions you take today. Investing in your credit health is a calculated move that can save you over $50,000 in interest charges over the life of a 2026 home loan. When you analyze the credit repair cost Philadelphia providers offer, transparency must be your baseline. Legitimate restoration requires a partner who follows the Credit Repair Organizations Act of 1996, which mandates CROA-compliant post-performance billing to protect your wallet. You don’t have to face the credit bureaus without a powerful ally in your corner.

At our office located at 1515 Market Street, our seasoned specialists provide the expert reassurance needed to navigate complex FICO scoring models. We don’t rely on generic software. Instead, we focus on mastery and personalized strategy to help you take back control of your legacy. Achieving a higher score is the first step toward lower rates and permanent financial literacy. It’s time to stop letting derogatory items hold you back from the life you’ve earned. Master your financial future, get your personalized Philly credit strategy now. You’ve got the power to rewrite your story, and we’re ready to guide you every step of the way.

Frequently Asked Questions

How much does credit repair typically cost in Philadelphia?

Credit repair cost Philadelphia residents usually pay ranges from $79 to $149 per month plus a one-time audit fee of $99 to $199. If you invest in professional restoration, you avoid the high 24% interest rates often charged on subprime auto loans. Most local firms offer tiered packages based on the number of derogatory items. You pay for the expertise required to navigate Metro 2 compliance standards effectively.

Is it legal to pay for credit repair services upfront?

No, it’s illegal for a credit repair organization to charge you before they have fully performed the promised services. The Credit Repair Organizations Act mandates that companies must provide a written contract and wait until services are rendered to collect fees. If a company asks for $500 before sending a single dispute letter, they’re violating federal law. You deserve a partner who follows these 1996 regulations to protect your financial legacy.

How long does the credit repair process take in Pennsylvania?

The credit repair process in Pennsylvania typically takes 3 to 6 months to see substantial results. While the Fair Credit Reporting Act gives bureaus 30 to 45 days to investigate a dispute, complex cases with multiple 90-day lates require several rounds of intervention. If you start today, you could be ready for a mortgage application in 180 days. This timeline ensures every error is meticulously challenged and verified.

Can I remove legitimate late payments from my Philly credit report?

You cannot legally remove accurate, verifiable late payments from your Philly credit report. However, 40% of credit reports contain errors that look like legitimate lates but lack proper documentation. If a payment was actually on time, we use the law to force a correction. For true mistakes, we may suggest a goodwill adjustment strategy. Taking back control means ensuring your history is 100% accurate and reflects your true financial behavior.

Will my credit score go up immediately after hiring a service?

Your credit score won’t go up the moment you hire a service because bureaus update records in 30-day cycles. You’ll likely see the first movement in your FICO score within 35 to 45 days after the first round of disputes is processed. If you expect a 100-point jump overnight, you’ve been misinformed. Real restoration is a steady climb toward a 700+ score, not a magic trick.

What is the Credit Repair Organizations Act (CROA) and why does it matter?

The Credit Repair Organizations Act is a federal law passed in 1996 that protects you from unfair or deceptive advertising by credit repair firms. It gives you the right to cancel any contract within 3 business days without penalty. This legislation ensures you receive a transparent disclosure of your rights before you spend a single dollar. We treat these rules as the foundation of our master mentor relationship with every client.

Is business credit repair more expensive than personal credit repair?

Business credit repair is generally 50% to 100% more expensive than personal services due to the complexity of Dun & Bradstreet reports. While personal credit repair cost Philadelphia averages $100 monthly, business suites often start at $499 for initial setup. If you want to secure a $50,000 SBA loan, investing in a clean commercial profile is a necessary step. Building a corporate legacy requires specialized knowledge of UCC filings.

Are there free credit repair options available in Philadelphia?

Yes, you can repair your credit for free by filing disputes directly with Equifax, Experian, and TransUnion via their websites. Non-profit organizations in Philadelphia, such as Clarifi, offer counseling services at little to no cost for residents. If you have the 10 to 15 hours a month required to manage the paperwork, the DIY route is a viable option. Most people choose professional help to ensure the job is done right the first time.