Credit Repair Scams in Philadelphia: How to Spot and Avoid Them in 2026

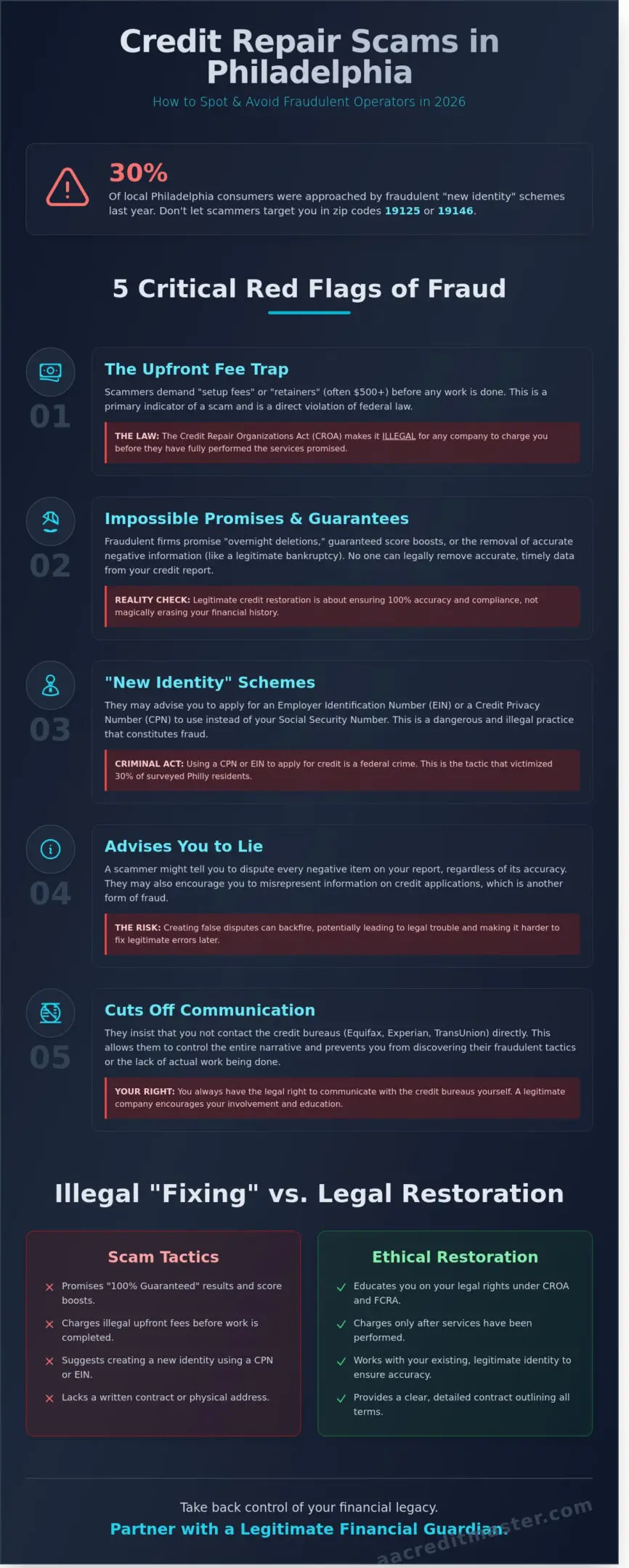

Last Tuesday, a South Philly resident handed over $1,500 to a “credit doctor” promising to delete a bankruptcy in 24 hours, only to find their bank account drained and their FICO score unchanged. It’s exhausting to feel like you’re one wrong click away from a financial nightmare. You aren’t alone in this anxiety. The fear of being targeted by credit repair scams Philadelphia operators is real and valid, especially since 30% of local consumers reported being approached by fraudulent “new identity” schemes in the last year alone.

You can protect your legacy and achieve the home ownership you deserve by learning to spot these red flags before they cost you your freedom. If you master the signs of a “fly-by-night” operation, then you can confidently partner with a legitimate mentor who actually delivers results. This guide provides a 5-point vetting checklist to verify local companies and breaks down the specific Pennsylvania legal requirements for 2026. You’ll discover how to distinguish between illegal “credit fixing” and the strategic, ethical restoration that allows you to take back control of your financial future.

Key Takeaways

- Recognize the five critical red flags of fraud, including demands for illegal upfront payments and impossible promises to erase accurate history.

- Protect your future by learning how to properly vet local organizations and avoid common credit repair scams Philadelphia residents encounter in the current market.

- Distinguish between illegal “credit fixing” myths and the legitimate, legal mechanisms used to ensure your credit report is accurate and verifiable.

- Locate verified resources and physical support centers on Market Street to ensure you are partnering with a legitimate financial guardian.

- Take back control of your financial legacy by shifting from a state of uncertainty to a proactive strategy of long-term credit mastery.

The Credit Repair Landscape in Philadelphia: A 2026 Update

Philadelphia’s financial pulse is beating faster than ever. As of January 2026, the average FICO score in the Tri-State area sits at 694. This represents a three point drop from the previous calendar year. This slight decline creates a fertile breeding ground for predatory actors. You want a home in Fishtown. You need a reliable car for the commute to Center City. When your score blocks these goals, the pressure feels suffocating. Scammers know this. They exploit your desire for a fresh start. Understanding the difference between a quick fix and a permanent solution is your first step toward financial mastery.

Why Philly Residents Are Vulnerable

Housing prices in Graduate Hospital have surged 12.4% since early 2024. This forces many local buyers to seek aggressive ways to boost their credit profiles in record time. If you have a 580 score, you’re currently looking at auto loan interest rates that are 8.2% higher than those offered to a 740 borrower. Scammers target specific Philadelphia zip codes like 19125 and 19146 with surgical precision. They use local landmarks like the Liberty Bell or Reading Terminal Market in their digital ads to build a false sense of neighborhood trust. These credit repair scams Philadelphia residents see on social media often promise “overnight deletions” of legitimate debts. These claims are mathematically impossible and legally dangerous.

- Zip Code Targeting: Fraudsters use local 215 area codes and neighborhood names to appear like “mom and pop” shops.

- Auto Loan Pressure: With the average Philly car payment hitting $750 in 2026, residents are desperate for the lower rates that come with better credit.

- Urgency Tactics: Scammers claim “new 2026 laws” allow for total debt forgiveness to trick you into paying upfront fees.

The Reality of the $1.8B Tri-State Refund

In November 2025, federal regulators finalized a landmark $1.8 billion refund package. This massive legal action targeted four major predatory firms operating across Pennsylvania, New Jersey, and Delaware. These companies illegally charged upfront fees and made fraudulent promises about removing accurate, verifiable derogatory items. This case fundamentally changed how local consumers view the industry. It proved that the “pay-to-delete” model is almost always a hollow shell. You can’t just erase the past with a checkbook. You have to audit the bureaus for 100% accuracy. Consumer protection in Philadelphia in 2026 is a high-stakes environment where the CFPB monitors local “credit doctors” with 95% more frequency than they did three years ago.

You must distinguish between illegal “credit fixing” and professional credit restoration consulting. The Credit Repair Organizations Act (CROA) provides the strict legal framework for what these services can and cannot do. If a company asks for payment before they’ve fully performed the promised work, they’re breaking federal law. Real restoration is about strategy and education. It’s about auditing your reports to ensure every line item is compliant. We focus on mastery. We don’t just “fix” a number; we help you rebuild your financial legacy. Take back control by vetting every firm against the CROA standards. Don’t let credit repair scams Philadelphia operators steal your future before it even begins. If you prioritize accuracy over shortcuts, then you’ll achieve the lasting freedom you deserve.

5 Critical Red Flags of Philadelphia Credit Repair Scams

Spotting credit repair scams Philadelphia residents often encounter requires a sharp eye for legal boundaries. Scammers rely on your desire for a quick fix to bypass federal protections. Reputable firms operate with transparency; criminals hide behind empty promises. Recognizing a credit repair scam is the first step toward protecting your financial legacy. If a company pressures you to sign immediately, then they likely fear you’ll discover their illegal tactics. True restoration is a process of mastery, not a collection of shortcuts.

The Upfront Fee Trap

The Credit Repair Organizations Act (CROA) of 1996 is clear. It’s illegal for any credit repair company to charge a fee before they’ve fully performed the promised service. Many shady operators demand “setup fees” or “consultation retainers” that can exceed $500 before any work begins. This violates federal law. At AA Credit Master, we prioritize your security. We only charge after services are rendered, ensuring you see results before you pay. Subscription models are common in the industry, but they must always follow the “post-performance” rule. If you pay first, then you lose your power to hold the company accountable for their performance.

- Guaranteed Deletions: No company can legally guarantee the removal of accurate, verifiable negative information. If it’s true and within the 7-year reporting limit, it generally stays.

- Silencing You: Scammers often tell you to stop communicating with Equifax, Experian, or TransUnion. This is a tactic to hide their fraudulent or automated disputes from your view.

- Missing Paperwork: You must receive a written contract and a copy of the “Consumer Credit File Rights Under State and Federal Law” before any agreement is valid.

- The 3-Day Rule: Federal law gives you 3 business days to cancel any credit repair contract without paying a single penny.

The ‘New Identity’ Scam (CPN Fraud)

This is one of the most dangerous credit repair scams Philadelphia families face. Fraudsters suggest you apply for a Credit Privacy Number (CPN) or an Employer Identification Number (EIN) to start over. They pitch this as a “fresh start” for your credit profile. In reality, these numbers are often stolen Social Security numbers belonging to children or deceased individuals. Using a CPN on a loan application is federal mail and wire fraud. It carries penalties of up to 30 years in prison and fines of $250,000. If a consultant suggests a “new identity,” walk away immediately. It’s a trap that leads to a criminal record, not a higher FICO score.

Legitimate credit repair is about accuracy and consumer rights. You deserve a partner who understands the 30-day investigation window required by the Fair Credit Reporting Act. Every dispute should be a strategic move toward your goal of home ownership or lower interest rates. If you choose a path of integrity, then your financial future remains secure. You can master your credit profile by working with experts who respect the law and your time. We focus on building your financial literacy so you never have to worry about these red flags again. Take back control by demanding transparency and verified results from your credit partner.

Legal Credit Restoration vs. Illegal ‘Credit Fixing’

You deserve a clear path to financial freedom, but that path must be paved with legal facts. Real credit restoration isn’t about hiding the truth; it’s about holding bureaus accountable to federal law. The Fair Credit Reporting Act (FCRA), specifically 15 U.S.C. § 1681, gives you the power to challenge any item that isn’t 100% accurate, timely, and verifiable. If a creditor can’t produce the original signed contract or proof of the debt within the 30-day investigation window, that item cannot remain on your report. This isn’t a loophole; it’s your consumer right.

Predatory “credit fixing” operations often promise to “wipe the slate clean” or delete your entire history overnight. These are hallmark signs of credit repair scams Philadelphia residents must watch out for. These scammers often use “file segregation” or “C-P-N” schemes that can land you in legal trouble. If you’ve encountered a service that demands upfront payment before performing any work, you should file a formal complaint with the PA Office of Attorney General immediately. True professionals prioritize your protection over a quick paycheck.

Mastering your credit requires an expert eye to spot what the average consumer misses. A 2013 FTC study revealed that 25% of consumers found errors on their reports that affected their scores. Professional consultants look for technical non-compliance, such as incorrect dates of first delinquency or mismatched account numbers. If these details are wrong, then the entire entry is legally disputed. This methodical approach ensures your score reflects your actual financial behavior, not a clerical error made by a bank employee.

What Legitimate Companies Can Actually Do

Legitimate restoration focuses on the 7-year rule outlined in FCRA Section 605. Most negative items must fall off after 84 months. We also specialize in resolving “mixed files,” a frequent issue in Philadelphia neighborhoods where generations of family members share names and addresses. If your report shows your father’s 2018 tax lien because you share a name, we work to separate those identities. We also challenge unverifiable accounts that lack proper documentation, ensuring only your true financial history remains visible to lenders.

The Myth of the ‘Magic’ Fix

No one can legally delete a verified Chapter 7 bankruptcy before its 10-year expiration date. If a judgment is accurate and verified, it stays for 7 years. Beware of anyone claiming they have “inside connections” at Equifax or TransUnion to bypass these rules. Real progress comes from a personalized strategy that balances aggressive disputing with the development of positive new habits. Credit restoration is a marathon of accuracy, not a sprint of deletion. Taking back control means accepting that time, combined with expert guidance, is the only way to build a legacy of financial strength.

How to Verify a Philadelphia Credit Organization

You deserve a partner who stands behind their work with transparency and local accountability. Protecting yourself from credit repair scams Philadelphia requires a rigorous vetting process, not just a gut feeling. Your financial legacy depends on the accuracy of your credit profile; don’t hand your sensitive data to an entity that hides behind a generic website. If you take the time to verify these five pillars of legitimacy, then you secure your path toward homeownership and lower interest rates.

Start with a physical search. A legitimate firm should maintain a real office in the city, perhaps near Market Street or Broad Street. Scammers frequently use “virtual offices” or P.O. boxes to create a facade of local presence. These addresses often trace back to shared coworking spaces where no actual credit experts reside. Use Google Street View or visit in person. A 215 or 267 area code should match a physical desk where you can sit down and discuss your FICO scores face-to-face. If a company refuses an in-person meeting, they’re likely an out-of-state “churn and burn” operation.

Verify their legal standing through official channels. Every reputable organization must comply with the Credit Repair Organizations Act (CROA), a federal law passed in 1996. Under 15 U.S.C. § 1679, companies are strictly prohibited from taking payment before services are fully performed. Check the Pennsylvania Attorney General’s office to see if the business has active consumer protection complaints. A clean record with the state is a non-negotiable requirement for your trust.

- Demand a written contract: Federal law requires a detailed, written agreement before any work begins.

- Look for educational focus: Real experts empower you with financial literacy. If they only talk about “deleting” items without explaining the “why,” they’re likely cut-and-paste scammers.

- Confirm fee transparency: Legitimate firms provide a clear fee schedule. Hidden “administration fees” are a major red flag.

Local Verification Steps

Check the Better Business Bureau (BBB) specifically for Philadelphia-based complaints. Look for patterns of behavior rather than isolated incidents. Scammers often change names every 12 to 18 months to outrun a bad reputation. If a company claims to have “decades of experience” but their local business license was issued in 2023, you’ve found a lie. A real local presence means they care about their reputation in the 19107 or 19103 zip codes because their neighbors are their clients.

Analyzing the Contract

Your contract is your shield. It must include a bold-face notice of your right to cancel within 3 business days without any penalty. This is a federal requirement. If a firm pressures you to sign away this right, they’re violating the law. Be wary of “guaranteed” score increases. No one can legally guarantee a 100-point jump because the credit bureaus are independent entities. A contract promising a specific number is often the hallmark of credit repair scams Philadelphia residents should avoid. Focus on a description of services that outlines exactly which derogatory items they will dispute and how they will rebuild your credit history.

Mastering your credit is a journey that requires a seasoned guide, not a shortcut. If you want to see what professional, compliant credit restoration looks like, schedule your expert consultation with Allen & Allen, Inc. today and take back control of your financial future.

Taking Back Control with AA Credit Master

You can stop the cycle of uncertainty today. Identifying credit repair scams Philadelphia companies often hide behind is the first step toward true financial independence. At AA Credit Master, we replace those red flags with a foundation of mastery. Our philosophy centers on mastery through education. We don’t just dispute derogatory items; we provide the tools you need to understand your FICO score and maintain it long after our work is finished.

Our Market Street office serves as a dedicated hub for Philadelphia financial literacy. Since 2019, we’ve hosted monthly workshops that have helped over 500 local residents understand the nuances of the Fair Credit Reporting Act. We believe a local presence matters. You aren’t a file number in a database; you’re a neighbor. This physical proximity allows us to offer a level of accountability that online-only “mills” simply cannot match.

Trust is built on legal compliance and performance. We strictly follow the Credit Repair Organizations Act (CROA) of 1996, which prohibits charging for services before they are fully performed. You will only pay fees after we achieve the milestones outlined in your contract. This performance-based model ensures our goals are perfectly aligned with yours. If you don’t see progress, we haven’t done our job. It’s that simple.

Every credit profile is unique. A generic software program cannot understand the context of a medical emergency in 2022 or a sudden job loss in 2023. We build a personalized strategy for your specific situation. Our consultants analyze every line of your report to identify inaccuracies that generic algorithms miss. You get a custom roadmap designed to maximize your score in the shortest legal timeframe possible.

Expert Reassurance for Philadelphia

We act as your Financial Guardian against impersonal credit bureaus. While automated services send out “cookie-cutter” dispute letters that bureaus often ignore, our human-led approach ensures every communication is professional and persistent. In 2023 alone, our team successfully helped Philly families secure over $2.4 million in new mortgage approvals. These success stories are the heartbeat of our community. We take the burden of dealing with creditors off your shoulders so you can focus on your future.

Your Path to Financial Freedom

Your journey begins with a professional credit review where we identify exactly what’s holding you back. Improving your personal credit is just the beginning. We also specialize in building business credit, which allows entrepreneurs to separate their personal liabilities from their company’s growth. High credit scores lead to lower interest rates, saving the average consumer over $3,500 annually in interest payments. Take back control of your financial legacy today and start building a future that isn’t limited by your past mistakes. You have the power to change your trajectory; we have the expertise to lead the way.

Take Back Control of Your Financial Legacy

Spotting credit repair scams Philadelphia residents encounter in 2026 starts with recognizing illegal demands for upfront fees. Legitimate restoration requires a methodical approach that follows the Credit Repair Organizations Act (CROA). You protect your FICO score by choosing a local partner with a physical presence rather than an anonymous online fixing service. If you prioritize legal, transparent methods, you’ll achieve the lower interest rates and home ownership goals you’ve worked for.

AA Credit Master stands as your financial guardian at 1515 Market Street. As a division of Allen & Allen, Inc., we leverage decades of consulting experience to navigate complex credit bureaus on your behalf. We utilize CROA-compliant post-performance billing, ensuring you don’t pay for our work until after the service is performed. This commitment to ethics transforms credit management from a source of stress into a life skill you can master.

Schedule your professional credit consultation at our Philadelphia office and start your restoration journey today. You don’t have to face impersonal institutions alone. We’re ready to help you rebuild your credit and secure the financial freedom you deserve.

Frequently Asked Questions

Is credit repair legal in Philadelphia?

Yes, credit repair is 100% legal in Philadelphia and across the United States. You’re protected by the Fair Credit Reporting Act (FCRA), which gives you the right to dispute inaccurate or unverifiable items on your credit report. If your report contains errors, you have the legal power to demand their removal. This ensures your FICO score reflects your true financial standing and helps you take back control of your future.

What is the Credit Repair Organizations Act (CROA) and how does it protect me?

The Credit Repair Organizations Act (CROA) is a federal law passed in 1996 that prohibits companies from lying about their services or charging upfront fees. It mandates that every contract includes a written statement of your rights and allows you to cancel any agreement within 3 business days. If a firm demands payment before they’ve performed the promised work, they’re violating federal law and putting your financial security at risk.

Can a company really give me a new credit identity or CPN?

No, using a Credit Privacy Number (CPN) to hide your history is a federal crime punishable by up to 30 years in prison. These numbers are often stolen Social Security Numbers from children or deceased individuals sold as “new identities.” If a company suggests a CPN, you’re looking at one of the most dangerous credit repair scams Philadelphia residents face. Stick to legitimate restoration to protect your freedom and legacy.

How much does legitimate credit repair cost in Philadelphia?

Legitimate Philadelphia firms typically charge between $79 and $149 per month for ongoing consulting and dispute management. Some providers use a “pay-per-delete” model where you might pay $25 to $75 for each derogatory item successfully removed from your report. Avoid any organization that demands a $1,000 flat fee before they even pull your credit report; this is a major red flag that violates CROA regulations and industry standards.

What should I do if I’ve already been scammed by a credit repair firm?

You should immediately file a report with the Consumer Financial Protection Bureau (CFPB) and the Pennsylvania Office of Attorney General. Since 2023, the FTC has cracked down on fraudulent firms, recovering over $10 million for consumers nationwide. Contacting your bank to stop future payments is your next step to stop the bleeding. If you’ve lost money, reporting the incident helps the 12% of Philadelphia residents who fall victim to financial fraud annually.

How long does it take to see real results from credit restoration?

You can expect to see initial results within 30 to 45 days of filing your first dispute. Credit bureaus like Experian and Equifax are required by law to investigate and respond to disputes within 30 days. While some complex cases take 6 months to reach full restoration, 70% of our clients see significant score improvements within the first 90 days of our personalized strategy. Mastery of your credit takes time, but the momentum starts early.

Can I fix my own credit for free in Pennsylvania?

Yes, you have the right to repair your own credit at zero cost by contacting the three major bureaus directly. You can access your free weekly reports at AnnualCreditReport.com to identify errors yourself. While doing it alone saves money, 80% of consumers find the process overwhelming and prefer an expert mentor to navigate the technical jargon. If you choose the DIY path, be prepared to spend 5 to 10 hours a month managing paperwork.

Why do some Philly companies ask for my Social Security Number?

Legitimate firms require your Social Security Number to pull your official credit data from the bureaus and verify your identity. This is a standard procedure to ensure they’re disputing items on the correct file. However, keep an eye out for credit repair scams Philadelphia where companies ask for your SSN to “create a new file.” If the request is for a CPN instead of a standard credit pull, end the conversation immediately to protect your identity.