How to Get Approved for a Mortgage in Philadelphia: The 2026 Homebuyer’s Guide

Your FICO score isn’t a life sentence; it’s a dynamic tool that determines whether you pay $2,200 or $1,750 for the same rowhome in Brewerytown. You’ve likely felt the sting of a past rejection or felt overwhelmed by the 14 different documents required to get approved for a mortgage Philadelphia banks offer. It’s exhausting to feel like you’re fighting a system designed to keep you in a rental cycle. We understand that stress, but we also know that financial restoration is within your reach right now.

You can secure a loan lenders will fight to fund by mastering your credit profile and utilizing the city’s unique 2026 incentive programs. If you clean up your reporting errors today, then you’ll unlock the lower interest rates that save the average Philly buyer $45,000 over the life of their loan. This guide provides a clear roadmap to mortgage-readiness, from qualifying for the Philly First Home grant to boosting your score by 60 points in record time. It’s time to take back control and secure the legacy your family deserves.

Key Takeaways

- Secure a lower monthly payment by mastering the 2026 interest rate environment and the specific credit tiers required for maximum affordability.

- Gain clarity on the “Mortgage Pull” process to ensure your actual lender-ready FICO score meets the elite 740+ benchmark.

- Follow a precise, step-by-step roadmap to get approved for a mortgage Philadelphia lenders will fund, including a deep audit of local tax records and documentation.

- Access significant savings through the Philly First Home Grant and PHFA programs by learning how to meet current 2026 eligibility criteria.

- Take back control of your financial future with a personalized credit strategy that transforms you from an applicant into a confident homeowner.

The Philadelphia Mortgage Landscape in 2026

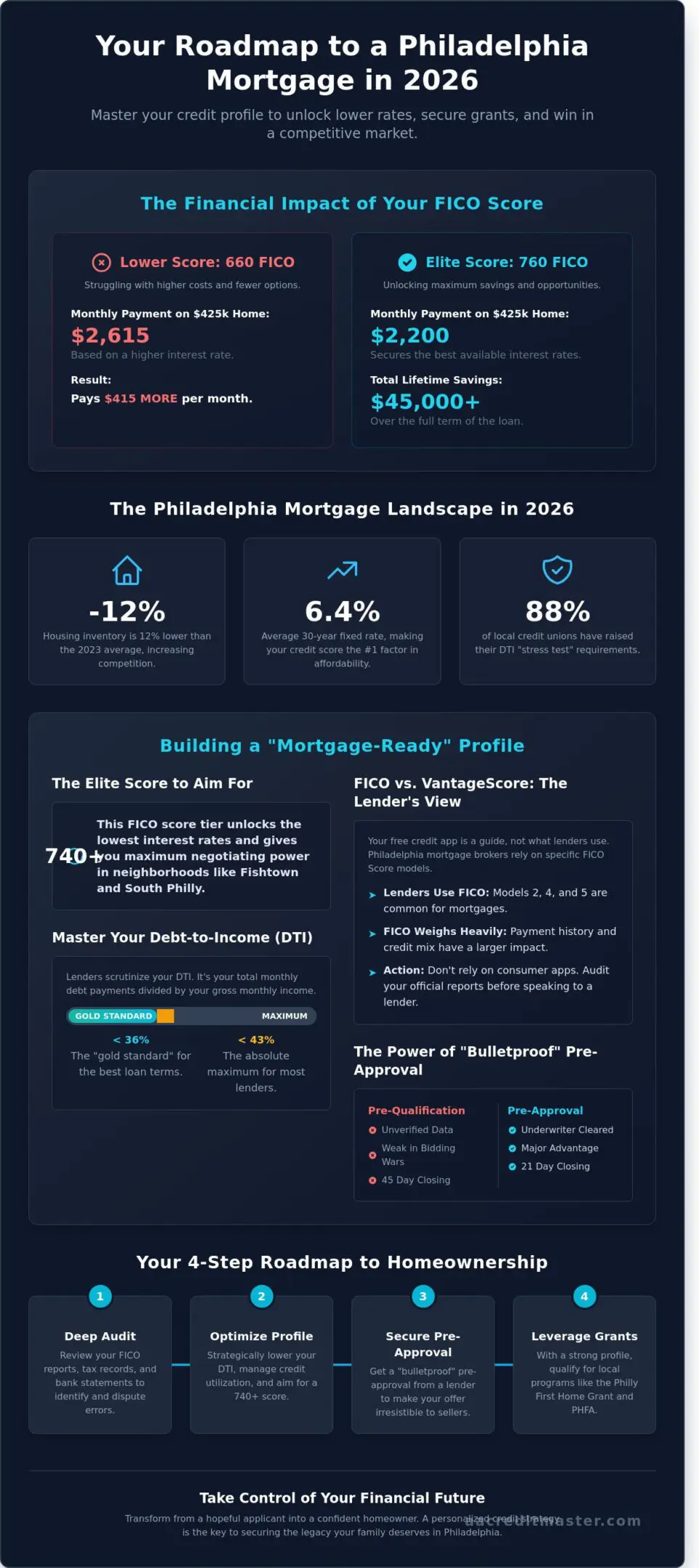

To get approved for a mortgage Philadelphia lenders now require a level of financial transparency that did not exist three years ago. Getting approved in 2026 is no longer about a simple handshake or a basic income check. It is a rigorous verification process where an underwriter scrutinizes your tax returns, bank statements, and debt obligations. This “bulletproof” approval serves as your financial passport in a city where inventory remains 12% lower than the 2023 average. You are not just asking for a loan; you are proving you are a low-risk asset in a high-stakes environment.

The 2026 economy has redefined affordability. With the average 30-year fixed rate sitting at 6.4% as of January 2026, your credit tier is the single most important factor in your monthly budget. If your FICO score sits at 760, you could save $415 per month on a $425,000 rowhouse in South Philly compared to someone with a 660 score. Understanding what is a mortgage loan? is the first step, but mastering your credit profile is what actually secures the keys. You must view your credit as a tool to be managed, not a static number that defines you.

Distinguishing between a pre-qualification and a pre-approval is vital for your success. A pre-qualification is a surface-level estimate based on unverified data. In a competitive market, it is essentially worthless. A bulletproof pre-approval means a lender has already cleared your files through their underwriting system. This status allows you to close in 21 days rather than 45, giving you a massive advantage over other buyers.

Why Philly Lenders Are More Selective Now

Philadelphia-area underwriting has shifted significantly since the 2025 federal banking updates. Currently, 88% of local credit unions have raised their internal “stress test” requirements for debt-to-income ratios. National banks often use automated algorithms that can be unforgiving to minor errors on your report. Local lenders are more nuanced but demand higher FICO scores to offset local property tax volatility. Your credit score is the gatekeeper to your future legacy. If you want to get approved for a mortgage Philadelphia agents respect, you must address derogatory items before you start your home search. Take back control of your narrative by ensuring your report is accurate and optimized.

Neighborhood Market Realities

In high-demand pockets like Fishtown or Chestnut Hill, financial credibility is your only leverage. Properties in these zip codes often receive 5 or more offers within the first 48 hours of listing. Sellers prioritize buyers who can guarantee funding without hiccups. In high-tax neighborhoods, a high credit score is the only way to keep your total monthly payment sustainable. If your interest rate is 1% lower because of your credit mastery, then your purchasing power increases by approximately $40,000. Just having “good enough” credit is a recipe for losing out to more prepared buyers. Aim for excellence to ensure your offer is the one that gets signed.

Building a “Mortgage-Ready” Credit Profile

You want to own a piece of Philadelphia. Your credit profile is the key that unlocks that door. By 2026, lenders have tightened their standards to ensure long-term stability. A score of 620 might get you in the game for an FHA loan, but it won’t secure the best terms. To grab the lowest interest rates in neighborhoods like Fishtown or South Philly, you should aim for a 740 or higher. This 120-point gap can save you over $350 a month on a standard $400,000 mortgage. That’s money back in your pocket for home improvements or savings.

FICO vs. VantageScore: The Mortgage Reality

Your free credit app is a guide, not the absolute truth. Most consumer apps use VantageScore 3.0, but Philadelphia mortgage brokers rely on specific FICO versions. These models weigh your payment history and “credit mix” much more heavily. If you have derogatory items like a 30-day late payment from 2024, it will negatively impact your mortgage pull more than your free app suggests. You must identify these errors early. Take back control by checking your official reports through mortgage resources provided by the CFPB to understand your consumer rights before you speak to a lender.

The Mastery of Debt Management

To get approved for a mortgage Philadelphia lenders look closely at your Debt-to-Income (DTI) ratio. In a city where property taxes and insurance costs are shifting, keeping your total DTI below 36% is the gold standard for approval. If your monthly debts, including your future mortgage, exceed 43% of your gross income, your borrowing power drops significantly. Focus on the “Credit Utilization” rule. Keep your credit card balances below 10% of their total limits for at least 60 days before your application. This simple move often boosts scores by 25 to 45 points almost overnight. You can begin mastering your finances in Philadelphia today to ensure your profile is bulletproof before the big pull.

Lenders also want to see a healthy mix of accounts. Having a combination of revolving credit and installment loans proves you can handle different types of financial responsibility. Mastery isn’t about luck; it’s about a personalized strategy that looks at your specific accounts. If you feel overwhelmed by the numbers, a custom credit consultation can provide the professional clarity you need to move forward with total confidence.

Step-by-Step: How to Get Approved for a Mortgage in Philadelphia

To get approved for a mortgage Philadelphia buyers must follow a precise, localized roadmap. The city’s unique tax codes and utility structures create hidden hurdles that can derail an application if you aren’t prepared. Success isn’t about luck; it’s about mastering your financial profile before the lender ever sees it.

Auditing and Cleaning Your Record

Philly residents often find “ghost” collections from Philadelphia Gas Works (PGW) or the Water Department on their reports. These $150 or $200 errors can drop a FICO score by 60 points overnight. You should start this audit process at least 180 days before you plan to tour homes in neighborhoods like Chestnut Hill or Passyunk. This six month window allows the three major bureaus to verify your disputes and update your files properly. You can use expert credit repair services in Philadelphia to expedite this and ensure your record reflects your true financial standing. Don’t let an old rent dispute from a 2022 lease agreement stand between you and your new front door.

The Documentation Deep Dive

Lenders in 2026 require the “Big Four”: 30 days of paystubs, two years of W2s or 1099s, 60 days of bank statements, and a valid government ID. If you’re one of the 15% of Philly workers in the gig economy or running a small business in Fishtown, you must provide your Philadelphia Net Profits Tax (NPT) returns. Missing these local tax records is a primary reason for mid-process rejection. Total transparency with your loan officer prevents surprises. If you have a large deposit from a side hustle, document the source immediately. Take back control of your paperwork early to avoid the stress of a last minute document scramble.

- Step 1: Audit your credit for Philly-specific utility inaccuracies.

- Step 2: Gather 2026 documentation, including NPT and Wage Tax records.

- Step 3: Secure a local lender who understands Pennsylvania Housing Finance Agency (PHFA) products.

- Step 4: Execute a credit restoration strategy to peak your score above the 720 threshold.

- Step 5: Finalize your pre-approval letter to compete in the Philly housing market.

Partnering with a local lender is vital because they understand PA-specific loan products that national “big box” banks often overlook. Once your documentation is set, execute a final credit restoration strategy to peak your score. This moves you from a “maybe” to a “preferred buyer” in the eyes of the underwriter. Finally, secure your pre-approval letter. In a market where 45% of homes receive multiple offers within 48 hours, having this letter in hand is your only way to get approved for a mortgage Philadelphia sellers will actually respect. Mastery of these steps transforms you from a dreamer into a homeowner.

Leveraging Philadelphia Grants and Assistance Programs

Winning the keys to a new home requires more than just a steady paycheck. You need a strategic advantage. In 2026, the Philly First Home program remains the most powerful tool for local buyers, offering up to $10,000 or 10% of the purchase price toward down payments. This grant directly tackles Philadelphia’s high closing costs, which often reach 7% of the total loan amount. To get approved for a mortgage Philadelphia lenders will actually fund, you must meet the program’s 620 minimum credit floor. If your score falls below this threshold, you lose access to these funds immediately. Rebuilding your credit profile is the first step to securing this “free” money.

Philly First Home and K-FIT Programs

City funding for the 2026 cycle was refreshed on July 1, 2025, but it disappears quickly. The K-FIT program provides a forgivable second mortgage of up to 5% of your home’s price, capped at $8,000. While these programs are labeled for “low-to-moderate income” buyers, they have hidden credit score barriers. Lenders view a 580 score as a high risk, even with city backing. You can use these grants to wipe out closing costs entirely if you position your credit health correctly before applying. A restored credit report turns a denied application into a funded dream.

Pennsylvania State-Level Opportunities

The PHFA Keystone Home Loan offers lower interest rates for first-time buyers. However, state aid is often tiered. A buyer with a 740 FICO score qualifies for a significantly lower interest rate than a buyer at 660, even when using the same PHFA program. National “big box” lenders often ignore these local nuances. They treat you like a data point in a machine. A local credit specialist provides a human element, identifying specific derogatory items that might block state-level approval. If you master your credit score now, then you maximize your savings for the next 30 years.

Combining state-level loans with city grants creates a “stacking” effect. This strategy can reduce your out-of-pocket expenses to nearly zero. You aren’t just buying a house; you’re building a legacy. This mastery over your financial profile ensures that you aren’t just another applicant, but a preferred candidate for every available dollar in the city’s budget.

Don’t let a low score stand between you and $10,000 in grant money. Take back control of your financial future today and secure the assistance you deserve.

Master Your Mortgage Journey with AA Credit Master

Your credit score is the most significant hurdle between you and a new set of keys. At AA Credit Master, we don’t view you as a three-digit number. We see a future homeowner who needs a dedicated Financial Guardian. Our philosophy centers on expert reassurance and a personalized strategy that treats your credit report like the legal document it is. We stand as a powerful shield between you and the three major credit bureaus. These impersonal institutions frequently fail consumers; in fact, a 2024 study showed that 25% of credit reports contain errors that can lower scores by 20 points or more. We force these bureaus to acknowledge your rights and correct the record.

You deserve a partner who is as invested in your success as you are. This is why we operate on a “Post-Performance” promise. Our model ensures that we only win when your credit does. You shouldn’t pay for empty promises or stagnant progress. We align our goals with your specific need to get approved for a mortgage Philadelphia lenders will actually fund. By removing the financial risk of restoration, we empower you to take back control of your financial legacy and move toward your closing date with total confidence.

Our Personalized Restoration Process

Generic software fails because it lacks the nuance of human judgment. Automated dispute tools often trigger “frivolous” flags from bureaus, leading to immediate rejections. Our human consultants provide a tactical advantage that algorithms can’t match. Consider a recent client from West Philadelphia who came to us with a 540 FICO score due to misreported medical debt from 2023. Within 120 days, our manual intervention cleared the derogatory items, boosting their score to 695. They moved from “Rejected” to “Approved” for a competitive 30-year fixed rate. You can begin this same transformation by visiting us at our 1515 Market Street office in the heart of Center City.

Your Next Step Toward Homeownership

The 2026 Philadelphia real estate market waits for no one. With home prices in neighborhoods like South Philly and Port Richmond rising by 5.8% over the last 12 months, delaying your credit restoration is a costly mistake. Every month you wait, the barrier to entry grows higher. Your dream home isn’t a matter of luck; it’s a matter of strategy. We provide the roadmap to help you get approved for a mortgage Philadelphia families can build their futures on. Stop feeling overwhelmed by debt and start feeling empowered by your progress.

- Expert Guidance: Stop guessing which bills to pay and start following a proven plan.

- Strategic Advantage: Leverage our deep understanding of FICO scoring models to maximize your points.

- Local Presence: Work with a team that understands the specific demands of the Philly housing market.

The path to your front door starts with a single decision. Don’t let a fixable credit score stand in the way of your family’s stability. Schedule your Philadelphia credit consultation today and take the first step toward mastering your financial future.

Secure Your Philadelphia Homeownership Future Today

The 2026 housing market in Philadelphia requires more than just a down payment; it demands a credit profile that commands respect from lenders. You’ve learned how to leverage local grants like the Philly First Home program and why addressing derogatory items is the first step toward a lower interest rate. If your FICO score isn’t where it needs to be, you don’t have to face the credit bureaus alone. To get approved for a mortgage Philadelphia lenders will actually fund, you need a strategy built on 100% CROA compliance and post-performance fees.

Since our founding, AA Credit Master has served as a financial guardian for local families. We provide a tailored strategy specifically designed for the unique requirements of Philly mortgage applicants. Our team ensures every dispute and rebuilding step aligns with the 2026 lending standards. Stop letting past financial stress dictate your legacy. Take back control of your financial story and turn that “denied” letter into a set of house keys. Your new home is within reach.

Master your credit and get approved; Start your Philly home journey here

Frequently Asked Questions

What is the minimum credit score for a mortgage in Philadelphia in 2026?

You need a minimum FICO score of 580 for an FHA loan or 620 for a conventional mortgage in Philadelphia as of 2026. While some lenders accept lower scores, hitting the 740 threshold unlocks the most competitive interest rates. If your score sits below 580, you must focus on removing derogatory items to get approved for a mortgage Philadelphia lenders will fund. Take back control by monitoring your reports from all three bureaus monthly.

Can I get approved for a mortgage with a recent collection on my Philly record?

You can secure a mortgage with a recent collection, but lenders often require these accounts to be paid or settled at least 12 months prior to application. A collection added within the last 90 days can drop your score by 50 to 100 points instantly. Our strategy involves disputing inaccurate data to clear your path. If you resolve these liabilities early, you demonstrate the financial maturity required for a 30 year commitment.

How long does the credit restoration process take before I can apply for a loan?

Most clients see significant score improvements within 90 to 180 days of starting the restoration process. The Fair Credit Reporting Act gives bureaus 30 days to investigate disputes, meaning each round of corrections takes roughly one month. We prioritize a personalized strategy over generic software to accelerate this timeline. Your journey to homeownership moves faster when you replace errors with a legacy of positive payment history and master your financial profile.

Are there special mortgage programs for first-time buyers in Philadelphia?

Philadelphia offers robust support through the PHFA Keystone Home Loan and the Philly First Home grant which provides up to $10,000 in assistance. These programs specifically help residents who haven’t owned a home in the last 3 years. You must complete a city-certified housing counseling course to qualify for these funds. Using these tools reduces your out of pocket costs and makes the dream of a stable home a tangible reality for your family.

What is the difference between mortgage pre-qualification and pre-approval?

A pre-qualification is a basic estimate based on unverified data, while a pre-approval is a formal commitment after a lender reviews your tax returns and pay stubs. In the competitive 2026 Philly market, sellers won’t consider offers without a verified pre-approval letter. This document proves you have the financial power to close the deal. It turns you from a browser into a serious contender for your future home and provides immediate confidence.

How much do I need for a down payment in the Philadelphia market?

You should prepare for a 3.5% down payment for FHA loans or 3% for specific conventional programs in the Philadelphia area. For a median-priced home of $250,000, this equates to roughly $7,500 to $8,750 in cash upfront. Don’t forget to budget an additional 3% for closing costs like title insurance and transfer taxes. Beyond these initial costs, it’s wise to also budget for future maintenance. As part of your research, you can explore Sidewalk and Driveway Leveling to understand the types of upkeep new homeowners often face. Mastering your savings plan now ensures you aren’t caught off guard at the closing table when you finalize your purchase.

Does AA Credit Master guarantee mortgage approval?

No company can legally guarantee a mortgage approval because only the lender makes the final funding decision. We focus on the mastery of your credit profile to ensure you meet or exceed every underwriting requirement. By removing inaccurate derogatory items, we position you as the ideal candidate for a loan. Our role is to act as your financial guardian throughout the restoration process, standing between you and impersonal credit institutions to ensure fairness.

How does my debt-to-income ratio affect my Philly home search?

Lenders generally require a debt-to-income (DTI) ratio below 43% to get approved for a mortgage Philadelphia institutions offer. If your monthly debts exceed 50% of your gross income, you’ll likely face a denial or high interest rates. Lowering this number gives you more purchasing power in neighborhoods like Fishtown or South Philly. When you balance your income against your liabilities, you gain the freedom to choose the home you truly want.