How to Improve Your Credit Score in Philadelphia: A Master’s Guide to Financial Restoration

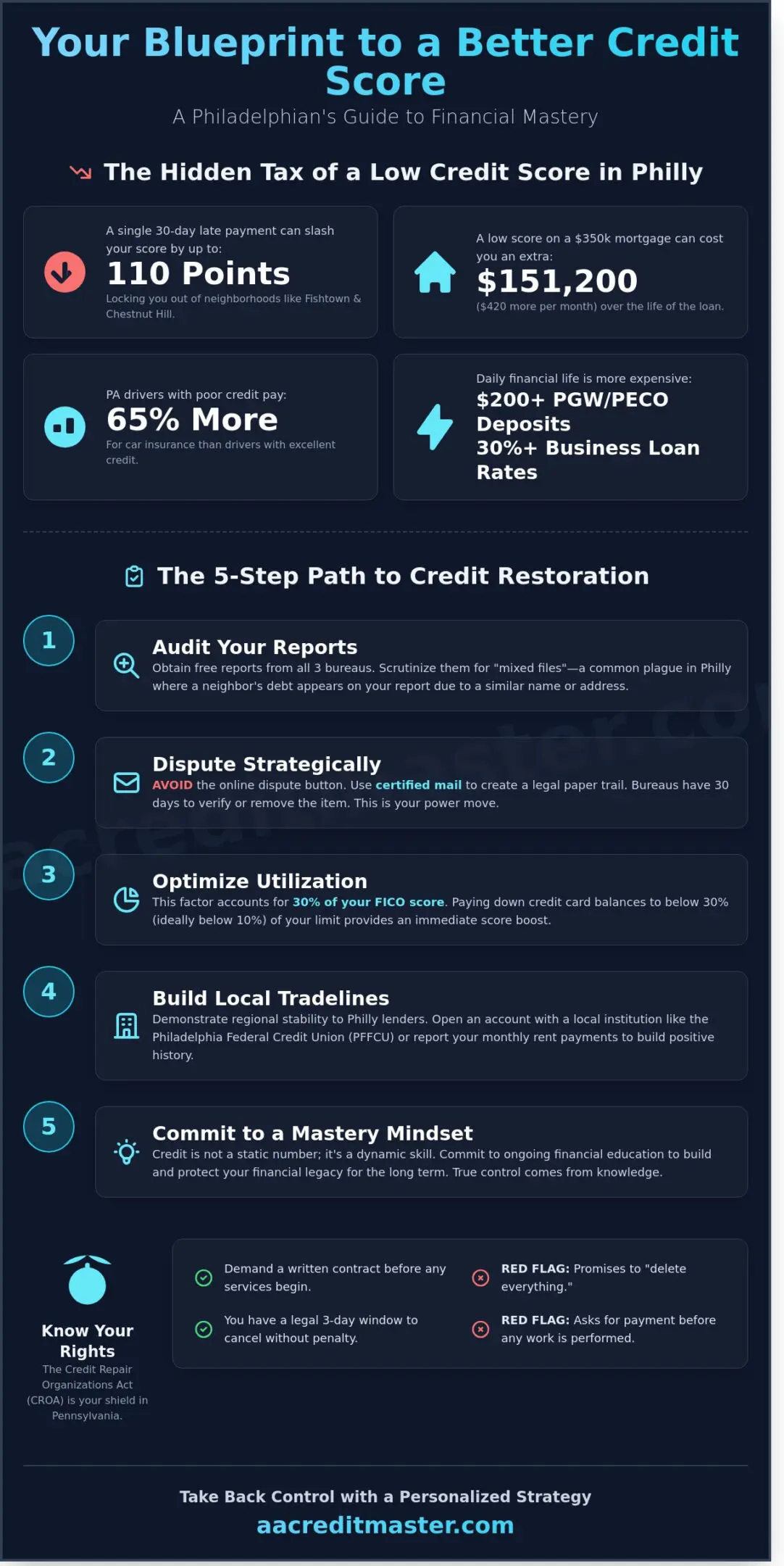

A single 30-day late payment on your report can slash your FICO score by up to 110 points, effectively locking you out of Philadelphia’s most competitive neighborhoods like Fishtown or Chestnut Hill. It’s frustrating to watch your homeownership dreams stall because of a clinical number that feels entirely out of your reach. If you’ve been denied a mortgage or noticed your PA car insurance premiums are $450 higher than they should be, you’ve felt the weight of financial instability. You likely believe that learning how to improve credit score in Philadelphia is a confusing, uphill battle against impersonal institutions.

You deserve a clear path to restoration. We’ll provide the exact, step-by-step strategy to dispute derogatory items and rebuild your profile from the ground up. You’ll learn how to qualify for a PHFA mortgage and unlock the city’s most favorable financial opportunities. This breakdown moves you from uncertainty to mastery, providing the exact blueprint needed to take back control of your financial legacy. We’ll explore everything from credit bureau secrets to long-term financial literacy habits.

Key Takeaways

- Secure the best mortgage rates for Philadelphia rowhomes and premium Center City rentals by mastering the local credit landscape.

- Follow a professional five-step roadmap on how to improve credit score in Philadelphia by identifying and disputing inaccurate derogatory items.

- Evaluate the critical differences between city-funded counseling and professional restoration to choose the most effective path for your financial recovery.

- Boost your rating quickly by leveraging local institutions like the Philadelphia Federal Credit Union and reporting your monthly rent payments.

- Take back control with a personalized strategy from our Market Street experts, moving beyond generic software to achieve true financial mastery.

Understanding the Philadelphia Credit Landscape in 2026

Living in the City of Brotherly Love requires more than just grit; it requires a FICO score that opens doors. In 2026, your credit profile acts as your financial resume. If your score sits below 620, you face immediate barriers to the Philadelphia rowhome market. Lenders like PFFCU or local community banks often look for more than just a number. They analyze your history for stability. Learning how to improve credit score in Philadelphia means understanding that national banks use rigid algorithms, while local Pennsylvania lenders might offer flexibility if your report is clean of derogatory items.

You must distinguish between credit restoration and credit counseling. Credit restoration is the process of challenging the accuracy of items on your credit report to ensure the bureaus follow the law. It is about mastery over your data. Credit counseling focuses on budgeting and debt management. If you want to secure a Center City rental or a competitive mortgage, you need the aggressive, tactical approach of restoration to remove the roadblocks holding you back.

The Cost of Low Credit in Philly

A 100 point gap in your score costs you money every single day. On a $350,000 mortgage for a Manayunk rowhome, a score under 660 can increase your monthly payment by $420 compared to a 760 score. That is a $151,200 loss over a 30 year term. In Philadelphia, auto insurance premiums for drivers with poor credit are 65% higher than those with excellent credit according to 2025 insurance commission data. Even PGW and PECO may demand deposits exceeding $200 if your credit history shows recent late payments. For local small business owners in neighborhoods like Fishtown, low credit acts as a hidden tax, forcing them into high interest merchant cash advances with rates exceeding 30%.

Your Rights Under the CROA in Pennsylvania

The Credit Repair Organizations Act (CROA) is your shield against predatory “cowboys” who make impossible promises. Pennsylvania residents have the right to a written contract before any services begin. You have a legal three day window to cancel any agreement without penalty. If a local firm promises to “delete everything” or asks for payment before they perform any work, they are violating federal law. Authentic credit restoration is about legal precision and strategy. Take back control by demanding transparency and a personalized plan. You deserve a partner who views credit as a life skill to be conquered, not just a static number on a screen.

5 Steps to Improve Your Credit Score in Philadelphia

Take back control of your financial destiny by following a proven blueprint for restoration. You can’t fix what you haven’t measured; therefore, your journey begins with a deep dive into the data. Understanding how to improve credit score in Philadelphia requires more than just paying bills on time. It demands a strategic overhaul of your entire financial profile. If you follow these five steps, you’ll transform from a passive observer into a master of your own creditworthiness.

- Audit your reports from all three bureaus for local reporting errors.

- Strategically dispute inaccurate derogatory items using professional methods.

- Optimize your credit utilization ratio for an immediate score boost.

- Build a local tradeline portfolio to demonstrate regional stability.

- Commit to a Mastery Mindset with ongoing financial education.

Auditing Your Philadelphia Credit Report

You are entitled to free weekly credit reports from Equifax, Experian, and TransUnion through annualcreditreport.com. In a densely populated city like Philly, “mixed files” are a frequent plague. You might find a neighbor’s 2021 utility collection from a North Philly rowhome appearing on your report simply because you share a common last name. A derogatory item is a negative record, such as a late payment or a tax lien, that slashes your score and warns lenders you’re a high-risk borrower. Identifying these local errors is the fastest way to see an upward shift in your numbers.

The Power of Strategic Disputes

Clicking a “dispute” button on a credit monitoring app is a trap. These automated systems often force you to waive your rights to a full investigation under the Fair Credit Reporting Act. To see real results, you must use certified mail with a return receipt requested. This creates a legal paper trail that the bureaus cannot ignore. When you provide detailed documentation, such as a 2022 lease agreement or a cleared check, the bureau has 30 days to verify the debt or remove it. Tracking your progress through physical mail ensures you remain the authority in the conversation. If you need a partner to handle this heavy lifting, you can explore a personalized restoration strategy that puts the pressure on the creditors instead of you.

Beyond disputes, focus on your credit utilization ratio, which accounts for 30% of your FICO score. If you reduce your balances to below 10% of your total limits, you’ll likely see a significant point increase within 45 days. Combine this with a local tradeline portfolio. Opening a secured card or a credit-builder loan through a local institution like the Philadelphia Federal Credit Union shows lenders you’re rooted in the community. Mastery isn’t about a quick fix; it’s about building a legacy of financial literacy that keeps your score high for decades. If you treat your credit like a skill to be mastered, you’ll never have to worry about a rejection letter again.

Philly Credit Repair vs. Free Counseling: Which Path is Right?

Deciding how to improve credit score in Philadelphia often starts with a choice between public resources and private restoration. You must weigh the value of your time against the complexity of your financial report. If you have a single late payment from 2023, a DIY approach might suffice. If you’re facing a wall of derogatory items while trying to secure a mortgage, you need a more aggressive ally.

The Limitations of Free City Programs

The City of Philadelphia provides Financial Empowerment Centers through phila.gov that offer vital support for basic budgeting. These programs are excellent for learning the fundamentals of debt management. However, they operate on thin margins and high volume. You will often face a 30 to 45 day waiting list just for an initial intake session. These counselors focus on education, not the surgical removal of reporting errors. They provide a map; they don’t drive the car for you. If your goal is a rapid score increase to catch a 6.5% interest rate before it climbs, the slow pace of a non-profit “Credit Academy” may cost you more in lost opportunities than you save in fees.

The Benefits of a Credit Score Specialist

A professional specialist acts as your Financial Guardian. We don’t rely on generic software that sends “one-size-fits-all” dispute letters. We analyze the clinical reality of your FICO data to find specific violations of the Fair Credit Reporting Act. This personalized strategy is essential for high-stakes goals like home ownership. If you can move your score from a 620 to a 720, the ROI is massive. On a $285,000 home in a neighborhood like Mount Airy, a 1% difference in your mortgage rate saves you roughly $200 per month. That equals $72,000 over a 30 year term. Professional restoration offers several distinct advantages:

- Direct Advocacy: We stand between you and impersonal credit bureaus to demand accuracy.

- Aligned Interests: Post-performance fee structures mean we only succeed when your score improves.

- Speed to Result: Expert consulting can often achieve in 90 days what takes DIYers 18 months to navigate.

- Strategic Mastery: We teach you how to maintain your score so you never have to pay for repair again.

Take back control of your financial legacy. If you hire a master mentor, then you gain a powerful ally who knows exactly where the pitfalls lie. We help you master how to improve credit score in Philadelphia by treating your credit as a life skill to be conquered, not just a number on a screen.

Leveraging Local Philadelphia Financial Habits and Tradelines

True financial restoration isn’t just about deleting old mistakes; it’s about building a solid foundation using the resources in your own neighborhood. Learning how to improve credit score in Philadelphia requires a hyper-local approach to credit building. National banks often treat you like a anonymous data point, but local institutions like the Philadelphia Federal Credit Union (PFCU) offer credit builder loans specifically designed for our community. These loans hold your funds in a secured account while reporting monthly on-time payments to all three bureaus. This process often results in a 40 to 60 point increase within twelve months for those with thin credit files.

Philly tenants have a unique advantage that many overlook. With roughly 47% of the city’s population renting their homes according to 2023 Census data, rent reporting is a powerful, untapped tradeline. By using services that report your monthly payments at the Navy Yard or in Fishtown, you turn your largest monthly expense into a credit-building asset. You don’t have to sacrifice your lifestyle to see results. Mastery involves keeping your credit utilization below 30% while still enjoying the city. If you have a total credit limit of $2,000, keep your reported balance under $600. This simple ratio accounts for 30% of your FICO score and is the fastest way to signal reliability to lenders.

Building Credit with Local Lenders

Credit unions in the Delaware Valley offer secured cards that consistently outperform big-box bank options. These cards require a small deposit, usually between $200 and $500, but they act as a vital training ground for financial discipline. Establishing this local banking relationship now is a strategic move. When you apply for a mortgage in the next 24 months, having a documented history with a local lender can be the deciding factor for your approval. Take back control of your future by starting these relationships today.

Advanced Mastery: Business Credit for Philly Entrepreneurs

Center City startups often struggle because owners lean too heavily on personal FICO scores for business expenses. You must separate your personal and business credit to protect your family’s financial legacy. Start by registering your business in Pennsylvania and obtaining an EIN. Opening a business tradeline with a local supplier allows you to buy materials without affecting your personal utilization. This separation is the hallmark of financial mastery and ensures your personal score remains high even as your business grows.

Take Back Control with AA Credit Master’s Philadelphia Team

Secure your financial legacy from our professional hub at 1515 Market Street. While automated bots offer generic fixes that often fail, our team provides a personalized strategy designed specifically for the local market. You deserve a partner who understands that a FICO score represents your ability to provide for your family and build a future in this city. We prioritize education because restoration without literacy is only a temporary patch. Mastery means you gain the skills to remain financially healthy for life. If you learn the mechanics of your score now, then you protect your wealth forever.

Our Philadelphia office stands as a beacon of professionalism in the heart of the city. We don’t rely on software to do a human’s job. Instead, we offer expert reassurance through every step of the process. We’ve seen how a low score creates a ceiling on your potential. We’re here to break that ceiling. Understanding how to improve credit score in Philadelphia starts with recognizing that your situation is unique. We treat it with the individual attention it requires.

The AA Credit Master Restoration Process

We perform a forensic audit of your credit history to pinpoint every disputable inaccuracy. A landmark study found that 25% of consumer credit reports contain errors serious enough to result in a denied application. Our Financial Guardian approach means we fight these errors on your behalf. We strictly adhere to the Credit Repair Organizations Act (CROA). This federal law protects you by ensuring we only collect fees after we perform the contracted work. Our process is transparent and methodical:

- Comprehensive Audit: We identify duplicate accounts, incorrect balances, and outdated derogatory items.

- Strategic Disputes: We draft custom challenges based on the Fair Credit Reporting Act (FCRA).

- Continuous Monitoring: We track every change to ensure the bureaus comply with federal mandates.

Start Your Journey to Mastery Today

Your first consultation focuses on clarity and objective setting. Whether you want to qualify for a 3.5% down payment FHA loan or secure a $50,000 business line of credit, we build the roadmap to get you there. We’ll show you exactly how to improve credit score in Philadelphia by leveraging local insights and federal law. You’ll leave our 1515 Market Street office with a clear understanding of your current standing and a timeline for your restoration. Take the first step toward your new financial life and schedule your consultation at our Philadelphia office. Replace your anxiety with an actionable plan and join the thousands of Philadelphians who’ve reclaimed their financial freedom.

Master Your Financial Future in the City of Brotherly Love

You now possess the roadmap to navigate the 2026 credit landscape with confidence. By prioritizing strategic tradelines and understanding the difference between generic counseling and targeted repair, you’re already ahead of 70% of local consumers. Whether you’re one of the many Philadelphia homebuyers looking to secure a 3.5% down payment or a local entrepreneur seeking business capital, your FICO score is the key that unlocks those doors. Mastering how to improve credit score in Philadelphia is a life skill that pays dividends for decades.

Stop letting past mistakes dictate your future. At AA Credit Master, located at 1515 Market Street, Suite 1200, we specialize in helping Philly residents reclaim their purchasing power. Our post-performance service fees ensure you’re never paying for effort; you only pay for the tangible restoration of your credit health. It’s time to move from worry to action. Take back control of your financial future and consult with a Philly expert today. You’ve worked hard for your dreams; now it’s time to make sure your credit score works just as hard for you.

Frequently Asked Questions

Is credit repair legal in Philadelphia?

Yes, credit repair is 100% legal in Philadelphia under the federal Credit Repair Organizations Act of 1996. This law protects your right to challenge any item on your credit report that is inaccurate, unfair, or unverifiable. We operate under the strict guidelines of the Pennsylvania Credit Services Act. You have the legal power to demand a fair report, and we act as your expert guide to navigate these complex regulations.

How long does it take to see results with a credit score specialist?

You will typically see initial results within 30 to 45 days of starting your first dispute round. The Fair Credit Reporting Act requires bureaus to investigate and respond to disputes within a 30-day window. If you follow a personalized strategy, a full restoration often takes between 3 and 6 months. This methodical approach ensures we address every error to help you master your financial future and achieve your goals.

Can I improve my credit score for free using phila.gov resources?

Yes, you can access free financial counseling through the Philadelphia Financial Empowerment Centers (FEC) at locations like the United Way or Clarifi. These city-backed programs provide one-on-one coaching to help you understand how to improve credit score in Philadelphia without a fee. While these services offer excellent foundational guidance, they often lack the aggressive, customized dispute tactics required for complex cases involving multiple legal challenges against major credit bureaus.

What is a ‘good’ credit score for buying a home in Philadelphia?

You generally need a minimum FICO score of 580 for an FHA loan with 3.5% down, though a score of 620 is the standard benchmark for most Philadelphia lenders. If your score reaches 740 or higher, you’ll unlock the most competitive interest rates available. Securing a lower rate on a $250,000 mortgage in neighborhoods like Fishtown can save you over $40,000 in interest payments over the life of a 30-year loan.

Will checking my own credit report hurt my score?

Checking your own credit report is a soft inquiry and it will never lower your score. You can monitor your progress daily through tools like IdentityIQ or AnnualCreditReport.com without any penalty. If you want to take back control of your financial legacy, you must review your reports frequently. This proactive habit allows you to spot identity theft or reporting errors before they derail your next big purchase or mortgage application.

How much does professional credit repair cost in Philadelphia?

Professional credit repair services in Philadelphia typically range from $99 to $199 for an initial audit and setup fee. Monthly service fees usually fall between $89 and $149 depending on the level of intervention required. Investing in your credit health is a strategic move; raising your score by 50 points can decrease your auto loan interest by 5%. This simple shift saves you thousands of dollars in total financing costs.

Can AA Credit Master remove legitimate late payments?

We cannot legally remove accurate, verified late payments, but we ensure that every single detail of that reporting is 100% compliant with the law. If a creditor fails to provide documented proof of the late payment or reports the data inconsistently, the item must be deleted from your record. We focus on how to improve credit score in Philadelphia by identifying these technical inaccuracies that often hide within legitimate accounts.

What happens if a dispute is denied by the credit bureaus?

If a bureau denies a dispute, we pivot to a more aggressive strategy by providing new evidence or challenging the verification process itself. We don’t accept a “verified” response as the final word. Instead, we demand the specific method of verification used by the bureau. If they cannot produce the required documentation within the 30-day legal limit, we push for the immediate removal of the derogatory item.