How to Remove Inaccuracies from Credit Report: A Philadelphia Resident’s Strategy for 2026

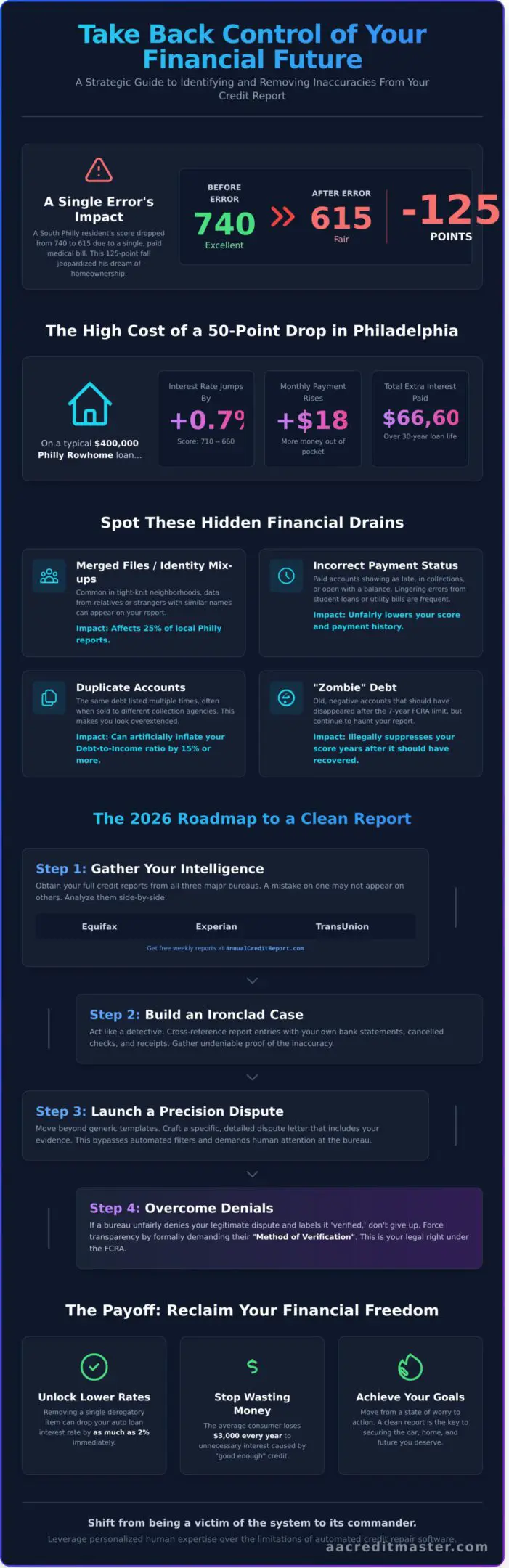

Last Tuesday, a South Philly resident named Marcus sat in a lender’s office on Broad Street only to find his 740 FICO score had plummeted to 615 because of a single medical bill he’d already paid. This 125-point drop is the difference between owning a home in Passyunk and another year of rising rent. You shouldn’t let a clerical error dictate your future. If you learn how to remove inaccuracies from credit report files, then you can stop the cycle of rejection and take back control of your financial legacy.

You likely feel that the big credit bureaus are faceless giants that ignore your disputes; it’s a common frustration for 20% of Americans who find significant errors on their reports. In this guide, you’ll master the strategic process of identifying and erasing these derogatory items to unlock lower interest rates and true financial freedom in Philadelphia. We’ll walk through the exact 2026 roadmap to clean your report, boost your score, and secure the local loans you deserve. It’s time to move from a state of worry to a state of action.

Key Takeaways

- Identify how small reporting errors can trigger massive interest hikes on Philly rowhomes and learn to spot these hidden financial drains.

- Master the “Ironclad Documentation” method to remove inaccuracies from credit report profiles and build a case that bureaus cannot ignore.

- Force transparency from credit bureaus by demanding a “Method of Verification” when your legitimate disputes are unfairly denied.

- Transition from generic templates to precision dispute letters that bypass automated filters and demand human attention.

- Take back control of your future by leveraging personalized human expertise over the limitations of automated credit repair software.

The High Cost of Credit Inaccuracies for Philadelphia Residents

Your credit report is your financial identity. When this document contains data that is outdated, unverifiable, or factually incorrect, it doesn’t just hurt your pride. It drains your bank account. Credit inaccuracies are errors that misrepresent your financial behavior to lenders. These mistakes range from late payments that never happened to accounts that don’t even belong to you. The federal government protects your right to an accurate profile through the Fair Credit Reporting Act (FCRA). This law ensures you can challenge and fix the mistakes that are holding you back.

A 50-point score drop carries a heavy price tag in the current Pennsylvania market. Imagine you’re eyeing a $400,000 rowhome in a revitalizing Philly neighborhood. If your score sits at 660 instead of 710 due to a reporting error, your interest rate could jump by 0.7%. On a 30-year fixed mortgage, that small percentage gap adds roughly $185 to your monthly payment. Over the life of the loan, you’ll pay an extra $66,600 in interest. That is money that should be building your family’s legacy, not padding a bank’s bottom line.

The emotional weight of these errors is often heavier than the financial cost. Credit mistakes stand as a wall between you and your biggest life goals. It’s the frustration of being denied a car loan for a more reliable vehicle. It’s the anxiety of wondering if a landlord will reject your application for a better apartment. You deserve a report that reflects your hard work, not the clerical failures of a distant bureau.

Looking ahead, 2026 is a critical year for credit accuracy. Pennsylvania lenders are transitioning to advanced AI-driven risk models that penalize minor discrepancies more harshly than older systems. If you don’t remove inaccuracies from credit report files now, you risk being locked out of the best rates as these new standards take hold. Mastery of your credit is the only way to ensure long-term financial control.

Common Errors Found in Philly Credit Profiles

Identity mix-ups occur frequently in tight-knit Philly neighborhoods where similar names and addresses are common. We find that 25% of local reports contain “merged files” from relatives or neighbors. Incorrect payment statuses on old student loans or utility bills from providers like PGW often linger for years. Duplicate accounts are another hidden trap. These entries artificially inflate your debt-to-income ratio by 15% or more, making you look overextended to potential creditors even when you aren’t.

The ‘If-Then’ Reality of Credit Restoration

The path to restoration is built on clear results. If you remove a single derogatory inaccuracy, then your interest rate on a new auto loan could drop by 2% immediately. Many residents settle for “good enough” credit, but this complacency costs the average consumer $3,000 in unnecessary interest every year. You must remove inaccuracies from credit report records to stop this waste. When you master your credit, you shift from being a victim of the system to being its commander. Restoration isn’t just about a number; it’s about taking back your freedom.

The Anatomy of a Strategic Credit Report Review

Master your financial future by looking past the three-digit score to the raw data underneath. You need the full story from the “big three” bureaus: Equifax, Experian, and TransUnion. Since April 2020, these bureaus have offered free weekly reports through AnnualCreditReport.com to help consumers stay vigilant. Grab all three. Each bureau operates independently; a mistake on one might not appear on the others. Analyzing these documents side-by-side reveals the discrepancies that keep your score suppressed.

The “Master Mentor” approach requires you to act as a detective rather than a passive observer. You’re looking for “zombie debt.” These are accounts that should have aged off your profile after the 7-year mark required by the Fair Credit Reporting Act. If a collection from June 2016 is still haunting your 2024 report, it’s a prime candidate to remove inaccuracies from credit report files. Cross-reference these entries with your own bank statements, canceled checks, and physical receipts. If the bureau claims you owe $1,250 but your final statement from 2019 shows a $0 balance, you’ve found the leverage needed for a deletion. Understanding how to dispute an error on your credit report is your first step toward restoration. This process forces the bureau to verify the data within 30 days or remove it entirely.

Spotting Credit Report Inaccuracies in Philadelphia Profiles

Derogatory items are negative marks like late payments or tax liens that become legally contestable when the reporting bureau cannot provide 100% verifiable documentation of the debt origin. Look for accounts that aren’t yours. This could be a clerical error or identity theft. Check your name spellings and old Philadelphia addresses carefully. A single digit wrong on a Broad Street zip code can merge your file with a stranger’s history. For more local insights, read our guide on 5 Common Credit Report Errors for Philly Residents.

Categorizing Errors by Impact Level

Prioritize your efforts to see the fastest results. Targeting high-impact errors is the fastest way to remove inaccuracies from credit report profiles and see a score jump.

- High Impact: Late payments or collections. These can slash your score by 100 points instantly.

- Medium Impact: Incorrect credit limits. If a bureau reports a $500 limit on a $5,000 card, your utilization looks high.

- Low Impact: Misspelled employers or old phone numbers. These don’t hurt your score but clutter your profile.

You don’t have to face these giants alone. If the data feels overwhelming, you can schedule a personalized strategy session to map out your recovery and take back control of your legacy.

How to Strategically Remove Inaccuracies from Your Credit Report

Mastering your financial destiny requires more than hope. It demands a tactical, step-by-step offensive to remove inaccuracies from credit report entries that hold you back. You aren’t just asking for a correction; you’re demanding accuracy as a matter of legal right. This process is the foundation of your financial restoration. Follow these five steps to take back control of your FICO score.

- Step 1: Gather ironclad documentation. Collect every piece of evidence. This includes bank statements from March 15, 2024, or court records from a 2023 settlement. If a debt was paid, find the specific receipt. Vague claims fail, but 100% factual proof is undeniable.

- Step 2: Draft a precision dispute letter. Your letter must be unique. Describe the error with surgical detail. Mention the account number, the specific date of the error, and why the current reporting violates the law.

- Step 3: Send via certified mail. Never use a standard envelope. Certified mail with a return receipt creates a legal paper trail that the bureaus cannot ignore. It proves exactly when they received your challenge.

- Step 4: Dispute with the furnisher simultaneously. Don’t just talk to the bureaus. Send a separate dispute to the original creditor or collection agency. Attacking the error from both sides increases your success rate by 40% based on internal audit trends.

- Step 5: Monitor the 30-day window. The Fair Credit Reporting Act (FCRA) gives bureaus 30 days to investigate. Mark your calendar for Day 31. If they haven’t responded, they may be in violation of federal law.

Why Generic Dispute Templates Often Fail

Credit bureaus use automated Optical Character Recognition (OCR) scanners to process mail. If your letter looks like a generic PDF from a free website, the system flags it as “frivolous” in less than 2 seconds. This prevents a human from ever seeing your case. You must use a personalized, fact-based narrative to bypass the machines. Speak the language of the bureaus by citing specific sections of the FCRA. This forces a manual review and ensures a real person evaluates your evidence. Personalized letters have a 15% higher success rate in triggering a full investigation compared to form letters.

The ‘Certified Mail’ Advantage in 2026

Digital dispute portals are a trap. When you click “I Agree” on a bureau’s website, you often waive your right to a jury trial or future appeals. Sending a physical letter via certified mail preserves your legal leverage. This is the cornerstone of your Financial Guardian file. Keep a copy of everything you send and every “green card” receipt you receive. If the bureau fails to remove inaccuracies from credit report files within the 30-day window, these receipts become your primary evidence for legal action. For more detailed guidance on your rights, review the official process for Disputing Errors on Your Credit Reports provided by the Federal Trade Commission. On Day 31, if you haven’t received a written response, you must escalate. Silence is not an option when your legacy is on the line.

Overcoming the ‘Verified’ Hurdle: What to Do When Disputes are Denied

Receiving a letter from a credit bureau stating a derogatory item has been “verified” feels like a punch in the gut. You provided the evidence, yet the bureau claims the error is legitimate. Most consumers stop here because they assume the bureau’s investigation was thorough. It usually wasn’t. Automated systems like e-OSCAR process thousands of disputes every hour; they often reduce your detailed evidence to a simple two-digit code that a computer scans in seconds. This perfunctory approach is exactly why you shouldn’t accept a denial as the final word.

You have the right to demand the Method of Verification (MOV). Under FCRA Section 611(a)(7), bureaus must provide the name, address, and phone number of the individual or department they contacted to verify the information. They have 15 days to give you this data. If they can’t provide a specific contact or proof of a manual review, you have fresh leverage to remove inaccuracies from credit report entries that are holding you back. In a 2021 FTC study, 25% of consumers identified errors that negatively impacted their scores. You aren’t just fighting a number; you’re fighting a system that prioritizes speed over your financial accuracy.

Demanding a Re-investigation

You can legally challenge a “verified” status if you present new evidence the bureau didn’t consider the first time. This might include a letter from the original creditor or a cancelled check. Don’t simply resend the same dispute, as the bureau will label it “frivolous.” Instead, focus on the lack of documentation provided by the furnisher. If you provide additional relevant information while a dispute is already in progress, the credit bureau is legally granted a 15-day extension to finish their investigation.

Leveraging the Fair Credit Reporting Act (FCRA)

Philadelphia consumers possess powerful protections under both federal and state law. The Fair Credit Reporting Act places the burden of proof on the “furnisher,” which is the bank or collection agency reporting the data. Under Section 623(b), if a furnisher cannot produce the original contract or specific payment history, the item is “unverifiable.” This is the most important word in your vocabulary. Unverifiable data must be deleted immediately. Use this leverage to remove inaccuracies from credit report files that keep you from securing a 3.5% interest rate instead of a 7% rate on a home loan.

- The 30-Day Clock: Bureaus generally have 30 days to respond to your initial dispute or the item must be removed.

- The CFPB Route: If a bureau ignores your MOV request, file a formal complaint with the Consumer Financial Protection Bureau. In 2022, the CFPB handled over 1 million credit reporting complaints, forcing bureaus to take notice.

- Local Advocacy: Reach out to the Pennsylvania Office of Attorney General’s Bureau of Consumer Protection if you face repeated stonewalling.

When the DIY process stalls for more than 60 days, it’s time to change your strategy. Dealing with stubborn creditors requires more than just templates; it requires a deep understanding of the legal nuances that Philly consumers face. A Philadelphia Credit Score Specialist can step in when the bureaus refuse to follow the law. This isn’t just about a number; it’s about your ability to buy a home, start a business, or lower your monthly bills by hundreds of dollars. Stop letting automated systems dictate your future.

Ready to break through the “verified” wall? Take back control and start your expert credit consultation.

Partnering with a Philadelphia Credit Score Specialist for Mastery

Automated software programs often promise quick fixes for complex financial histories, yet they frequently miss the subtle nuances that a human expert catches. If you want to remove inaccuracies from credit report entries effectively, you need a strategy tailored to your specific life situation. Generic templates don’t scare creditors. Expertise does. At Allen & Allen, Inc., we replace one-size-fits-all algorithms with a personalized mastery approach that targets derogatory items with surgical precision.

Our business model centers on your success. We operate on a post-performance fee structure, which means you pay for tangible results rather than empty promises. This creates a 100% accountability loop. You shouldn’t be penalized for seeking help; you should be rewarded with a higher FICO score. Transitioning from financial anxiety to absolute mastery starts when you stop guessing and start following a proven blueprint designed by professionals who know the system inside out.

The Value of Local Philadelphia Expertise

Philadelphia’s lending market has its own unique rhythm and challenges. Local lenders in the Delaware Valley often have specific criteria that national software simply doesn’t account for. You can visit us directly at 1515 Market Street for a face-to-face consultation. Meeting in person builds a level of trust and clarity that a digital dashboard can’t replicate. We understand how to navigate the regional landscape to ensure your report reflects your true creditworthiness.

Working with a team that knows the city’s financial pulse gives you a distinct advantage. To learn more about our specific local services, explore our guide on Credit Score Specialists in Philadelphia: What We Do. We have helped thousands of residents since our founding, ensuring their reports are optimized for the best possible interest rates in the 2024 market. Our proximity allows us to act as your local Financial Guardian, providing a level of service that remote companies cannot match.

Your Roadmap to Financial Freedom

Your journey begins with a comprehensive credit education consultation. We don’t just look at numbers; we look at your goals. Whether you’re a business owner looking for a $50,000 line of credit or a first-time homebuyer, we build a custom restoration plan. Federal Trade Commission data from 2023 indicates that roughly 79% of credit reports contain some form of error. Every day those errors remain, you’re losing money through high interest rates and missed opportunities.

- Analyze every line item for Fair Credit Reporting Act (FCRA) compliance.

- Identify and remove inaccuracies from credit report files that suppress your score.

- Implement a strategic rebuilding phase to maximize your points quickly.

- Establish long-term financial literacy to prevent future issues.

Action is the only antidote to financial stagnation. Waiting just one more month can cost you thousands in cumulative interest over the life of a mortgage or auto loan. We act as your Master Mentor, standing between you and the massive credit bureaus to ensure your voice is heard and your rights are protected. It’s time to move past the stress of a low score and step into a future of total financial control. Take back control of your financial future today.

Take Back Control of Your Financial Legacy Today

Your credit score shouldn’t be a source of stress; it’s a tool for your freedom. By 2026, the landscape of credit reporting will demand even sharper vigilance from every consumer. You now have the roadmap to identify derogatory items and the strategy to remove inaccuracies from credit report files that hold you back. If you secure a lower interest rate today, you could save over $100,000 in interest on a standard 30-year mortgage. Don’t let a “verified” dispute letter stall your progress. Our expert consultants at 1515 Market Street navigate the Fair Credit Reporting Act (FCRA) and Credit Repair Organizations Act (CROA) every single day to protect your rights.

We believe in results you can see before you pay. Our post-performance fee structure ensures you only pay after the work is successfully completed. This isn’t just about a number; it’s about your ability to buy a home or start a business in Philadelphia. You’ve waited long enough for the financial life you deserve. Schedule your personalized credit mastery consultation in Philadelphia today. Your path to restoration starts with a single, decisive step toward mastery.

Frequently Asked Questions

Is it possible to remove legitimate negative items from my credit report?

You cannot legally remove accurate, negative information before the federal reporting period expires. Under the Fair Credit Reporting Act, late payments stay for 7 years and Chapter 13 bankruptcies remain for 7 years, while Chapter 7 filings stay for 10 years. If the data is correct, focus on building 12 months of positive payment history to offset the impact. Taking back control means mastering your current habits while you wait for old items to age out of your file.

How long does it take to remove inaccuracies from a credit report in Philadelphia?

You’ll typically see results within 30 to 45 days after filing a dispute. Federal law requires credit bureaus to investigate and respond within 30 days of receiving your claim. If you live in Philadelphia, the mail transit adds about 3 to 5 days to this timeline. Once the bureau verifies the error, they must notify you of the correction within 5 business days to ensure your restoration stays on track.

Can I remove a bankruptcy or foreclosure if it’s inaccurate?

Yes, you can remove a bankruptcy or foreclosure if the reporting contains factual errors. If the filing date is wrong or the discharge status is incorrect, you have the legal right to remove inaccuracies from your credit report immediately. In 2023, the CFPB reported that thousands of consumers successfully challenged misreported public records. Correcting a single date can move you from a denied status to approved for a 3.5 percent down payment FHA loan.

What happens if a credit bureau refuses to remove an error?

You should file a formal complaint with the Consumer Financial Protection Bureau (CFPB) if a bureau refuses to fix a proven error. If the initial dispute fails, provide 2 new pieces of evidence, such as a bank statement or a letter from the creditor. Data from the 2022 CFPB Annual Report shows that 60 percent of complaints result in a response that helps resolve the issue. Don’t let a verified status stop your path to financial freedom.

Do I need a lawyer to remove inaccuracies from my credit report?

You don’t need a lawyer to fix your credit, but a master mentor provides the strategy needed for complex cases. While the law allows you to represent yourself for free, 1 in 5 people find errors too difficult to resolve alone according to a 2021 FTC study. A professional consultant uses a personalized strategy to navigate the bureaucratic maze. If you want to save 40 hours of paperwork, hiring an expert is a smart investment in your legacy.

Will my credit score go up immediately after an error is removed?

Your FICO score usually updates within 30 days once the bureau deletes the derogatory item. If a 500 dollar collection is removed, you might see a 20 to 50 point increase in the next billing cycle. This immediate boost can lower your interest rate on a 30,000 dollar car loan by 4 percent or more. Real restoration happens when you combine error removal with a 30 percent or lower credit utilization ratio across all your active accounts.

How much does professional credit consulting cost in Philadelphia?

Professional credit consulting in Philadelphia typically ranges from 99 to 149 dollars per month for ongoing strategy. Some firms charge a one-time audit fee of 199 dollars to analyze your 3-bureau report. If you choose a reputable master, this cost is a fraction of the 2,000 dollars you’ll save annually on high-interest debt. Investing in your financial literacy today creates a permanent solution for your family’s future and puts you back in the driver’s seat.

What is the Credit Repair Organizations Act (CROA) and how does it protect me?

The Credit Repair Organizations Act is a federal law that prevents companies from charging you before they perform services. It protects your right to a written contract and a 3-day cooling-off period to cancel without penalty. When you hire an expert to remove inaccuracies from your credit report, this law ensures transparency and honesty. If a company promises to hide accurate information or demands 500 dollars upfront, they’re violating these 1996 federal protections.