The Essential Guide to Reviewing Your Credit Report in Philadelphia (2026)

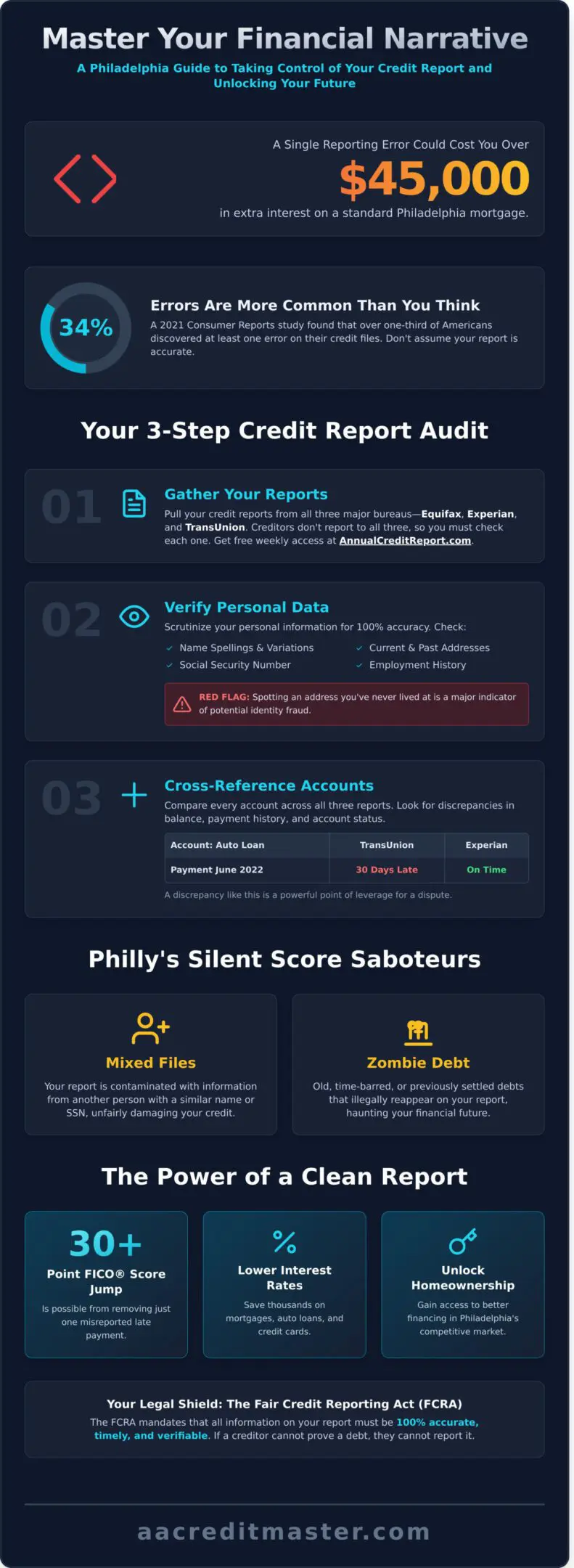

A single reporting error on your credit file can cost you an extra $45,000 in interest over the life of a standard Philadelphia mortgage. You likely feel the weight of past financial mistakes every time you think about your future. It’s exhausting to face conflicting data from the three major bureaus while avoiding the predatory scams that target your anxiety. You aren’t alone in this frustration, and you don’t have to let a static number define your worth.

If you take the time to master your financial narrative, then you can unlock the doors to homeownership and competitive business lines of credit. This guide will show you exactly how to review credit report Philadelphia documents to identify and dispute derogatory items with confidence. We’re going to transform your report into a clean reflection of your true potential. You’ll learn the specific steps to take back control of your data and build a foundation of financial literacy that lasts a lifetime.

Key Takeaways

- Transform your credit report into a strategic asset to overcome the unique financial pressures of Philadelphia’s competitive housing market.

- Follow a methodical checklist to review credit report Philadelphia records and verify your personal data across all three major credit bureaus.

- Guard your reputation against common urban inaccuracies like “Mixed Files” and “Zombie Debt” that can silently sabotage your score.

- Master the proactive dispute process to eliminate derogatory items and restore your path to homeownership and lower interest rates.

- Leverage a performance-based partnership where you pay for results, ensuring your financial restoration is guided by local Market Street experts.

Why a Professional Credit Report Review in Philadelphia is Your First Step to Financial Mastery

Your credit report is your financial autobiography. In a city as competitive as Philadelphia, this document determines where you live and exactly how much you pay to exist. A professional review credit report Philadelphia session is not a casual glance at your history. It is a strategic audit of your entire financial reputation. We act as your Financial Guardian. We stand directly between you and the massive, impersonal institutions that decide your worth based on a three-digit number. This process is about moving from a state of worry to a state of absolute authority.

Philadelphia residents face high-stakes pressure that varies by ZIP code. In Rittenhouse Square, where median home values reached $615,000 in early 2024, a small dip in your score can disqualify you from the best neighborhoods. Even in emerging areas like Brewerytown or Fishtown, rental applications are scrutinized more heavily than they were just 24 months ago. Before you can improve your standing, you must understand the fundamentals of What is a credit score? and how the three major bureaus calculate your risk. This foundational knowledge is your first weapon in the fight for financial restoration.

We use a strict “If-Then” logic to guide our strategy. If you master the details of your report today, then you unlock the door to a 3.5% lower interest rate on an auto loan tomorrow. If you identify a single misreported late payment from 2022, then you could see an immediate 30-point jump in your FICO score. Mastery is not a gift; it is a skill you develop to take back control of your legacy.

The High Cost of Credit Inaccuracies in Pennsylvania

A single inaccuracy on a Pennsylvania mortgage application is more than a nuisance; it is a financial catastrophe. Data shows that a 50-point discrepancy caused by a reporting error can lead to $48,000 in additional interest payments over the life of a 30-year fixed loan. Derogatory items carry a heavy psychological weight that can paralyze your decision-making. You don’t have to carry that burden alone. The Fair Credit Reporting Act (FCRA) serves as your legal shield. It mandates that every piece of data reported about you must be 100% accurate, timely, and verifiable. If an institution cannot prove a debt, they cannot report it. We ensure they follow the law to the letter.

Mastery vs. Quick Fixes: Why Education Matters

Generic software “fixes” are temporary band-aids that often fail when you need them most. We prioritize personalized credit consulting because your financial journey is unique. True mastery comes from financial literacy, which acts as a permanent solution rather than a fleeting adjustment. You don’t just want a higher number; you want the knowledge to maintain it for life. This education ensures you never find yourself at the mercy of a lender’s algorithm again. When you understand the mechanics of credit utilization and account age, you transform from a passive consumer into a savvy market participant. This is how you build a lasting legacy for your family in Philadelphia.

How to Review Your Credit Report: A Step-by-Step Philadelphia Guide

Securing your financial future starts with a clear view of your current standing. You can’t fix what you haven’t measured; therefore, your first move is to pull your files from Equifax, Experian, and TransUnion. Since 2023, the three major bureaus have made weekly reports permanently free through AnnualCreditReport.com. A 2021 study by Consumer Reports found that 34% of Americans discovered at least one error on their credit files. If you want to review credit report Philadelphia data effectively, you must look at all three bureaus because creditors don’t always report to every agency.

Begin your audit by scrutinizing your personal identification section. Verify that your name is spelled correctly and that your current Philadelphia address is accurate. Check your employment history for outdated or incorrect employers. These details seem minor, but identity thieves often use slight variations of your information to open fraudulent accounts. If you spot a street address you’ve never lived at, it’s a red flag for potential fraud. You should also ensure that your Social Security number and date of birth are perfectly aligned across all three documents.

Cross-referencing account details is where most Philly residents find the leverage they need for restoration. Compare the balance, payment history, and account status for your mortgage or car loan across the different reports. If TransUnion shows a 30-day late payment from June 2022 but Experian shows that same month as “on time,” you have a discrepancy that requires action. Disputing errors on your credit report is your legal right under the Fair Credit Reporting Act. This federal law requires bureaus to investigate and remove any “unverifiable information” within 30 days of your notification.

Look specifically for accounts that aren’t yours or entries that should have aged off. Most negative items must be removed after 7 years; however, Chapter 7 bankruptcies can stay for 10 years. If you find a collection account from 2015 still lingering on your file in 2024, it is dragging down your score unnecessarily. You can master your financial narrative by identifying these ghosts of the past and demanding their removal. Taking this proactive step puts the power back in your hands.

Decoding Technical Jargon: From FICO to Derogatory Items

Technical terms shouldn’t stand between you and a 700+ score. A “charge-off” means a creditor has written your debt off as a loss after 180 days of non-payment, but you still legally owe the money. “Utilization ratios” represent how much of your available credit you’re using; keep this under 30% to avoid a score drop. “Derogatory items” are simply negative marks like tax liens or judgments that signal risk to lenders. Understanding these labels helps you see exactly how a Philly lender views your application.

Personal vs. Business Credit Reports: What You Need to Know

Local entrepreneurs must understand that personal and business credit are two distinct engines. While your personal score uses your Social Security number, business credit relies on an EIN and reports to agencies like Dun & Bradstreet (D&B) or Experian Business. Keeping these worlds separate protects your personal assets from business liabilities. Building a strong business profile allows you to secure 5-figure or 6-figure credit lines without risking your family’s home. You’ll create a lasting legacy by optimizing both profiles simultaneously. This dual-track strategy is essential when you review credit report Philadelphia requirements for commercial loans.

Common Credit Report Inaccuracies Facing Philadelphia Residents

Errors on your credit report aren’t just minor typos. They are financial roadblocks that prevent you from securing the 3.5% interest rate you deserve on a new home or a low-interest auto loan. When you sit down to review credit report Philadelphia data, you must look beyond the surface. In a city of 1.5 million people, the credit bureaus often struggle with data integrity. Mistakes happen frequently. You need to act as your own Financial Guardian to ensure your history remains untarnished by administrative negligence or predatory collection tactics.

One primary threat is “Zombie Debt.” These are old, unverified debts that have surpassed the seven-year legal reporting limit. Debt buyers often purchase these expired accounts for pennies on the dollar and attempt to “re-age” the debt to make it appear recent. If a debt from 2015 suddenly reappears with a 2024 or 2025 date, it is a violation of the Fair Credit Reporting Act. You must identify these illegal resurrections immediately. Taking back control of your financial legacy starts with scrubbing these derogatory items from your record.

The “Mixed File” Phenomenon in Dense Urban Areas

Philadelphia’s density creates a unique problem called a mixed file. This occurs when a credit bureau merges your financial history with someone else who has a similar name or Social Security number. If you are one of the thousands of Philadelphians named “John Smith” or “Maria Rodriguez,” your report might include a neighbor’s $15,000 credit card default. You should verify every address listed in your history. If you see an apartment in South Philly where you never lived, it is a red flag. Identifying these subtle overlaps is the first step toward restoration. You can learn how to get your free annual credit reports to begin this audit today. Spotting a stranger’s late payment now saves you months of stress later.

Public Records and Local Philadelphia Liens

Local municipal disputes often bleed into your credit health. Philadelphia residents frequently face inaccuracies regarding Philadelphia Gas Works (PGW) bills or outdated property tax liens. Even if you satisfied a city lien in 2023, the record might still appear as “unpaid” in 2026. Under current 2026 reporting standards, public records must meet strict identity matching criteria to remain on your report. If a lien lacks your full name, address, and Social Security number, it is often disputable. Many Philadelphia-specific municipal filings fail these rigorous standards. If you find an outdated court record, you must demand a deletion to protect your FICO score.

Identity theft is another reality of urban life. Digital environments in cities like Philly see a 15% higher rate of unauthorized account openings compared to rural areas. Check your “inquiries” section for banks you don’t recognize. If an unknown lender ran your credit for a store card in King of Prussia while you were at home in Fishtown, you are likely a victim of fraud. When you review credit report Philadelphia documents, look for these specific red flags. Mastering your credit profile requires a proactive stance against these common urban errors. You have the power to rebuild your score and achieve the financial freedom you’ve worked for.

Taking Back Control: Disputing Errors and Rebuilding Your Score

You gain financial freedom when you eliminate the errors holding you back. A 2021 study by Consumer Reports found that 34% of Americans discovered at least one mistake on their credit files. These aren’t just minor typos; they are roadblocks to your mortgage or a lower interest rate. When you review credit report Philadelphia data with a professional, you uncover the specific inaccuracies that automated software often misses. You need a proactive strategy to identify, document, and challenge these derogatory items with surgical precision.

Our Master Mentor approach transforms you from a passive observer into an active participant in your restoration. We don’t just “fix” your credit; we coach you through the nuances of the Fair Credit Reporting Act (FCRA). If you understand the law, then you hold the power over the bureaus. This process requires patience. You should expect a 30 to 45-day window for bureaus to respond to initial challenges. A full restoration typically spans 4 to 6 months, depending on the complexity of your history. We set realistic expectations because genuine mastery takes time, not magic.

True progress happens when you transition from defensive disputing to offensive building. Removing a collection account is only half the battle. You must also diversify your credit mix and establish positive tradelines. If you maintain a utilization rate below 10%, then your score will reflect your discipline. We guide you in selecting the right tools to prove your reliability to future lenders.

The Dispute Process: More Than Just a Letter

Generic dispute templates often fail because credit bureaus use automated scanning systems to flag and dismiss repetitive language. Successful disputes rely on the “If-Then” logic of the law. If a creditor cannot provide original documentation for a 2020 late payment within the legal timeframe, then that item must be deleted. We focus on “unverifiable” and “outdated” challenges that force creditors to prove their claims. This strategic pressure ensures your report reflects the truth, not just a debt collector’s record.

Building Business Credit in Philadelphia

Philly startups can achieve legacy and control by separating personal and business liabilities. You can establish your first tradelines by opening Net-30 accounts with vendors like Uline, Grainger, or Quill. These companies report your payment history to business bureaus even if your company is less than 12 months old. Once you have 3 to 5 reporting vendors, your business gains its own identity. This allows you to secure funding without risking your family’s personal assets. It is the fastest way to build a foundation for long-term growth in the city.

Stop letting errors dictate your life and start your journey toward financial mastery. Take back control of your future by choosing to review credit report Philadelphia documentation with a Master Mentor today.

Master Your Future with AA Credit Master: The Philadelphia Advantage

Success begins at 1515 Market Street. AA Credit Master, operating as Allen & Allen, Inc., stands as the definitive authority for residents ready to transform their financial standing. We don’t just look at numbers; we see the person behind the file. When you review credit report Philadelphia documentation with our team, you gain access to over 26 years of regional expertise. Since 1998, we’ve focused on one goal: providing a clear path to financial freedom for the Philly underdog.

Our “Post-Performance” fee structure sets us apart from the competition. Most agencies demand massive upfront retainers before they’ve sent a single dispute letter. We flipped that broken model. You pay for results, not promises. We work first. You see the deletions and corrections. Then, and only then, do you pay. This ensures our goals align perfectly with yours. If we don’t deliver a better report, you don’t pay the performance fee. It’s the ultimate form of expert reassurance in a market filled with empty talk.

Why a Local Philadelphia Consultant Beats National Chains

National chains treat you like a ticket number in a massive database. They rely on generic software that misses the nuances of the Pennsylvania financial landscape. At our Market Street office, the human element is our greatest strength. We understand the specific lending habits of local institutions like PNC or Philadelphia Federal Credit Union. Our team acts as a powerful ally, standing between you and the three major credit bureaus. We know the laws that protect Pennsylvanians, and we use them to your advantage.

Customized Solutions for Individuals and Businesses

No two financial histories are identical. A strategy that works for a first-time homebuyer in Fishtown won’t work for a small business owner in Center City. When you review credit report Philadelphia data with us, we provide tailored resources to rebuild personal scores and establish robust business credit profiles. Our clients often see an average score increase of 45 points within the first 90 days. Whether you need to remove a 2021 medical debt or secure a $25,000 line of credit for your startup, we create the blueprint. This personalized strategy beats automated software every time.

Mastering your credit is a life skill, not a one-time fix. If you improve your score by just 30 points, you could save $150 every month on an average car loan. Those savings belong in your pocket, not the bank’s vault. We provide the financial literacy you need to ensure your score stays high long after our work is done. You don’t have to face the bureaus alone. Our seasoned professionals have navigated these pitfalls over 4,500 times. We know the shortcuts and the traps.

Stop letting a three-digit number dictate your quality of life. You have the power to change your trajectory. Take back control of your financial destiny today. Visit us on Market Street or call to schedule your consultation. Your legacy starts with a single, decisive action. Master your credit. Master your life.

Master Your Financial Future Starting Today

You’ve learned that a single error can cost you thousands in higher interest rates. Since the Federal Trade Commission reports that 20% of consumers have significant mistakes on their files, you can’t afford to wait. You’ve seen how to identify inaccuracies and the steps required to dispute them effectively. It’s time to review credit report Philadelphia data with a professional eye to ensure your next home loan or vehicle purchase doesn’t hit a wall.

At AA Credit Master, we stand as your financial guardian. We’re an A+ Rated and Accredited Business located at 1515 Market Street in the heart of Philadelphia. You won’t pay for our results until they’re delivered because we operate on a strict post-performance fee structure. We prioritize your legacy over generic software. If you fix your score now, then you’ll unlock the lower rates you deserve. You’ve got the tools; now you just need the right ally to help you use them.

Your journey toward financial mastery begins with a single, confident step forward. We’re ready to help you reach the finish line.

Frequently Asked Questions

Is it legal to hire a credit repair service in Philadelphia?

Yes, hiring a credit repair service is 100% legal in Philadelphia under the Pennsylvania Credit Services Act of 1976. This state law works alongside federal regulations to ensure companies provide transparent services and honest results. When you partner with a professional consultant, you gain a powerful ally who understands how to navigate these statutes to remove derogatory items. We help you take back control of your financial legacy by holding creditors accountable to these specific legal standards.

How long does it take to see results after a credit report review?

You can expect to see initial results within 30 to 45 days after you review credit report Philadelphia data and submit your first round of disputes. Federal law requires credit bureaus to investigate and respond to your claims within a 30-day window. If they can’t verify an item within this timeframe, they must delete it from your record. Quick action leads to faster score improvements and better interest rates on your next Philadelphia home loan.

What is the Credit Repair Organizations Act (CROA) and how does it protect me?

The Credit Repair Organizations Act is a federal law passed in 1996 that prevents credit firms from making false claims or charging you before they’ve performed services. It mandates a written contract and gives you a 3-day right to cancel any agreement without penalty. This protection ensures you remain the master of your financial journey. We follow every CROA guideline to provide the expert reassurance and high-level service you deserve while rebuilding your future.

Can I review my credit report for free in Pennsylvania?

Yes, every Pennsylvania resident can access their credit reports for free through AnnualCreditReport.com once every 7 days. While federal law originally guaranteed one free report every 12 months, the three major bureaus extended weekly access indefinitely in 2023. Taking advantage of this weekly access is the first step to master your finances. If you find errors during your check, you can start the restoration process immediately to protect your score.

How does business credit differ from personal credit for Philly entrepreneurs?

Business credit is linked to your Employer Identification Number (EIN) rather than your Social Security Number. While personal FICO scores range from 300 to 850, business scores like the Dun & Bradstreet PAYDEX range from 0 to 100. Establishing a strong business profile protects your personal assets from company liabilities. If you build a PAYDEX score of 80 or higher, you’ll secure much better terms for your Philadelphia-based startup or expansion project.

What should I do if a credit bureau refuses to remove an error?

You should file a formal complaint with the Consumer Financial Protection Bureau (CFPB) if a bureau ignores your valid dispute. In 2022, the CFPB handled over 500,000 credit reporting complaints to hold these massive institutions accountable to everyday consumers. Don’t let a stubborn bureau block your path to financial freedom. We act as your financial guardian to escalate these disputes and demand the total accuracy the law requires for your report.

Will reviewing my own credit report lower my score?

Checking your own credit report is considered a soft inquiry and it won’t lower your score by even a single point. Hard inquiries from lenders can drop your score by 5 to 10 points, but personal reviews are 100% safe. You should review credit report Philadelphia documents at least once a month to catch identity theft or reporting errors early. Staying informed gives you the confidence to manage your financial health without any fear of penalties.

How much does professional credit consulting cost in Philadelphia?

Professional credit consulting in Philadelphia typically ranges from $99 to $199 for an initial audit followed by monthly fees between $89 and $149. Some firms offer flat-rate restoration packages starting at $500 for specific goals like mortgage readiness. Investing in an expert mentor saves you thousands in high interest charges over the life of a loan. You’ll gain a personalized strategy that generic software simply can’t provide for your unique situation.